Matthias,

Thank you very much for your comments. I am trying to sort this out and you have some great ideas.

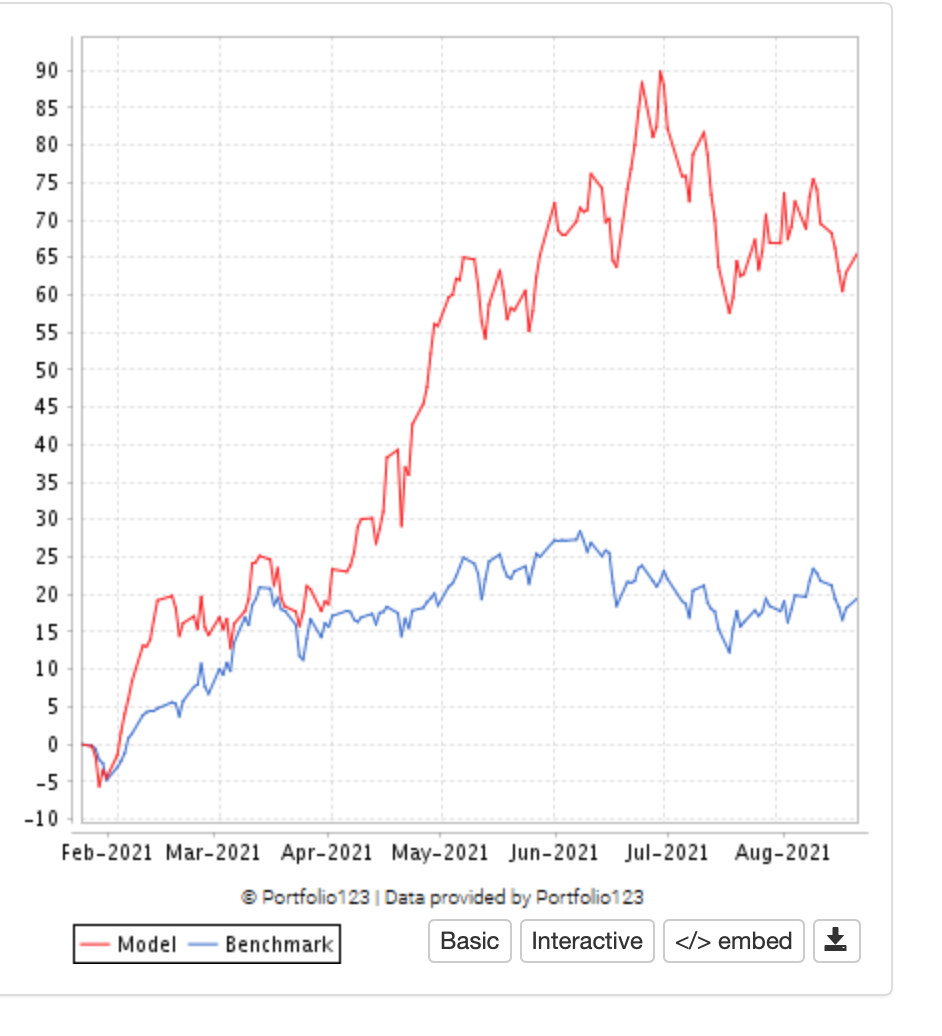

Slippage is not the answer, however. My slippage is not NEARLY as high as the variable slippage used in the sim here.

In addition, the sim and port usually buy the same ticker (but not always). The port has the slippage that I actually get when I trade (always edited to the real price I get with my broker). So the port includes my slippage. In those instances where the sim buys the same ticker it adds ADDITIONAL, UNREALISTIC slippage to the sim. This should put the sim at a disadvantage yet the sim is doing better. It must be something else.

With realistic slippage in the sim the difference gets ridiculous and I have no choice but to step back and take a look at this: to get a reality check from out-of-sample data.

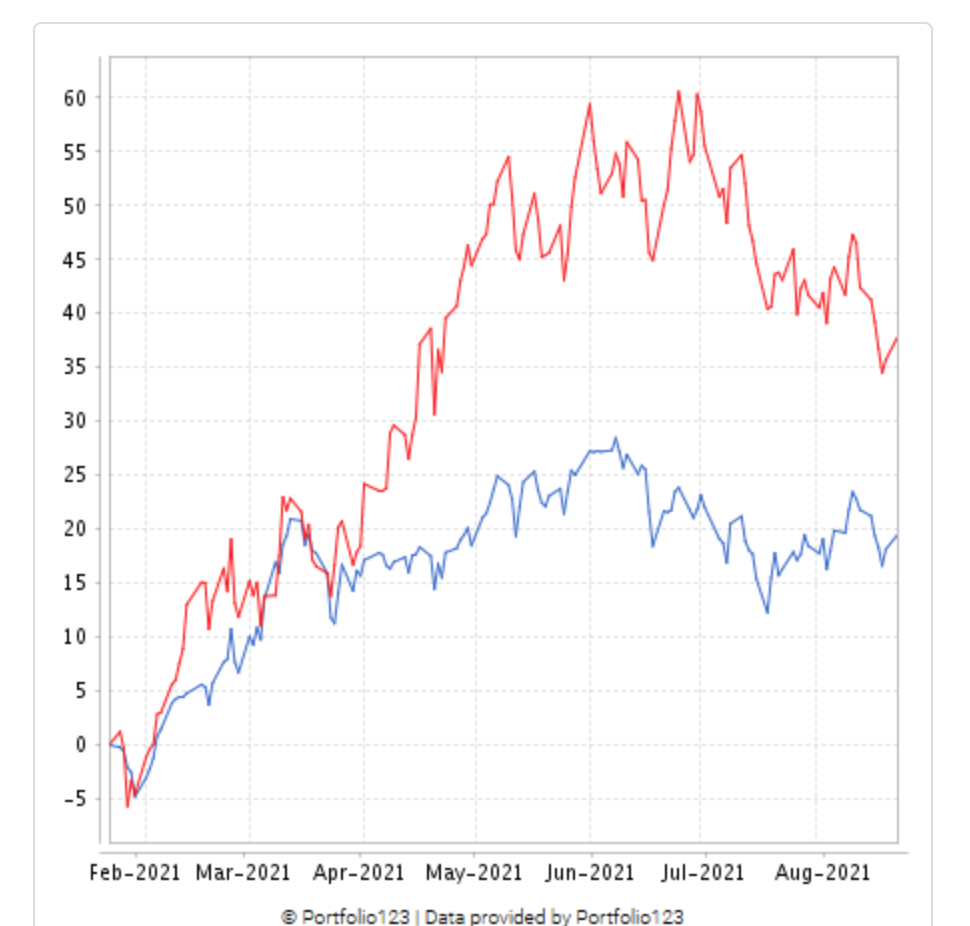

My sim does not reset the weights. It sells based on RankPos or a few sell rules. The stock is purchased, the entire position is held and then the entire position is sold.

Yes!!!

So I am using the screener (with no buy rules) to sort this out. I have not been doing this for long, however (exactly 2 weeks now). The “Force Positions into Universe” in the sim and port cause too much chaos (literally) and confusion.

Some differences occur in the screener the next day. BUT, a this point (2 weeks of data) it is arguable how much effect this has.

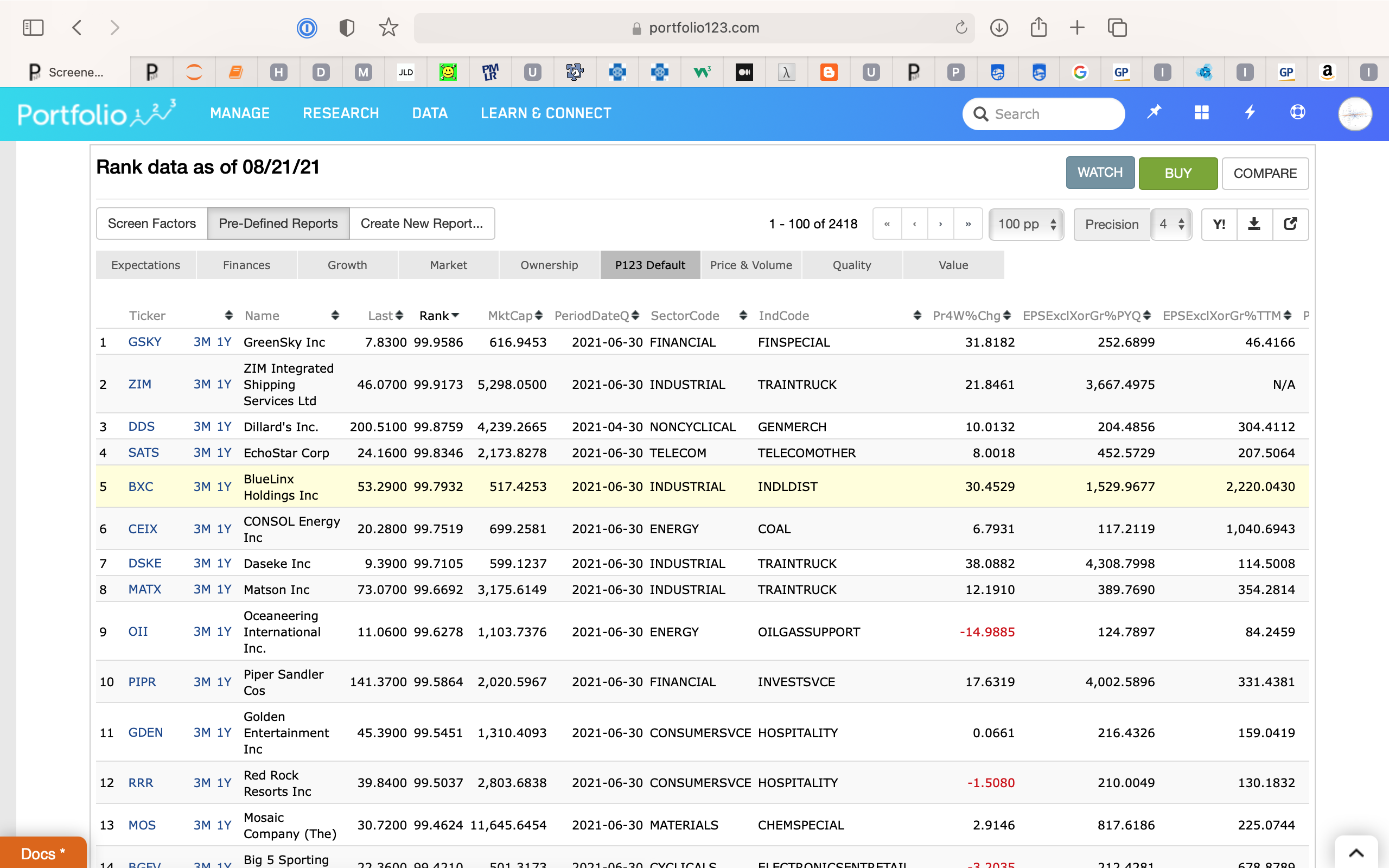

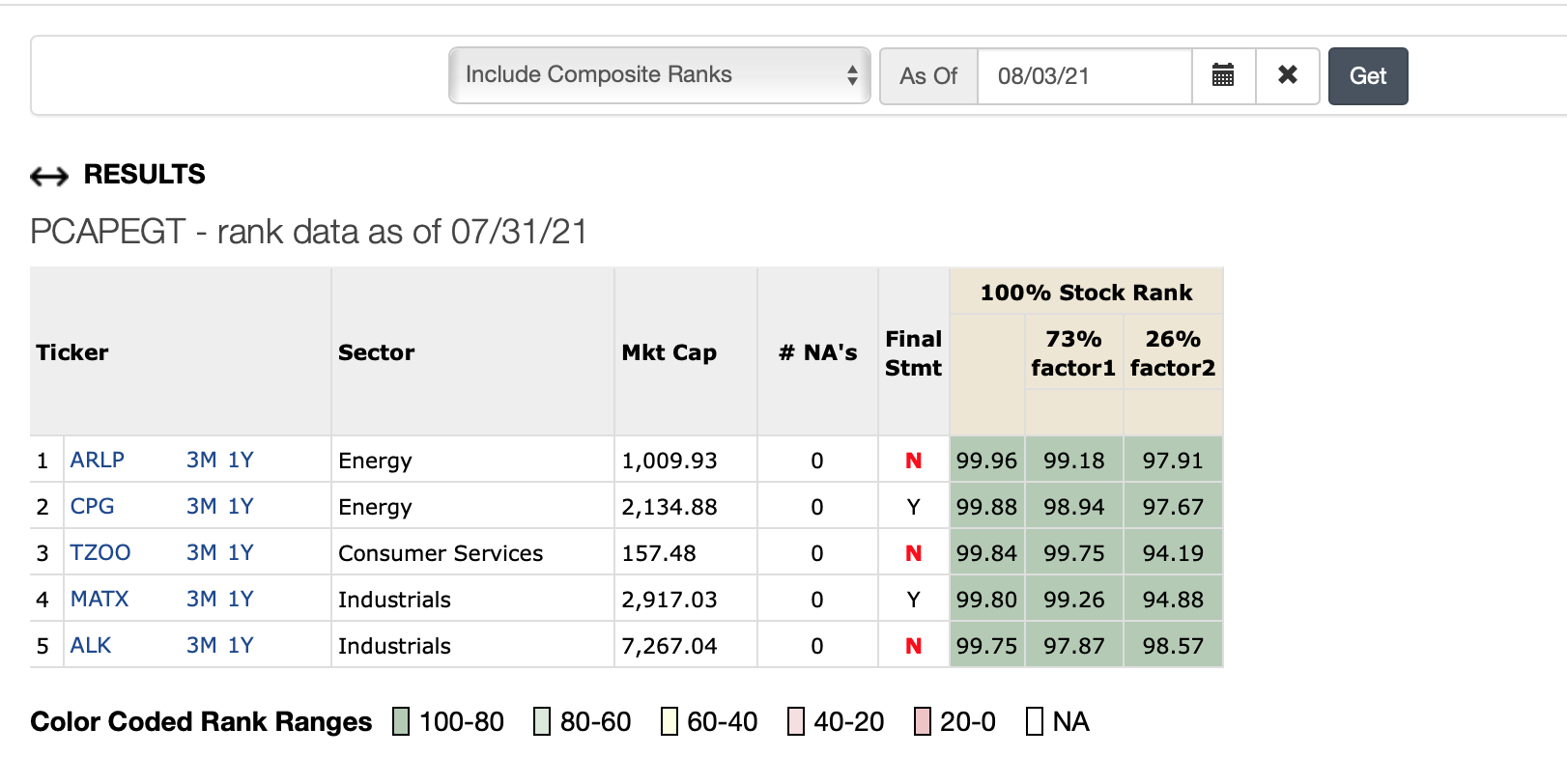

First image, screenshot of the screen Monday morning which gave rank data as of 8/21/21 (I always check that the data is fully updated). This uses exclude preliminary data which I think will end up being important.

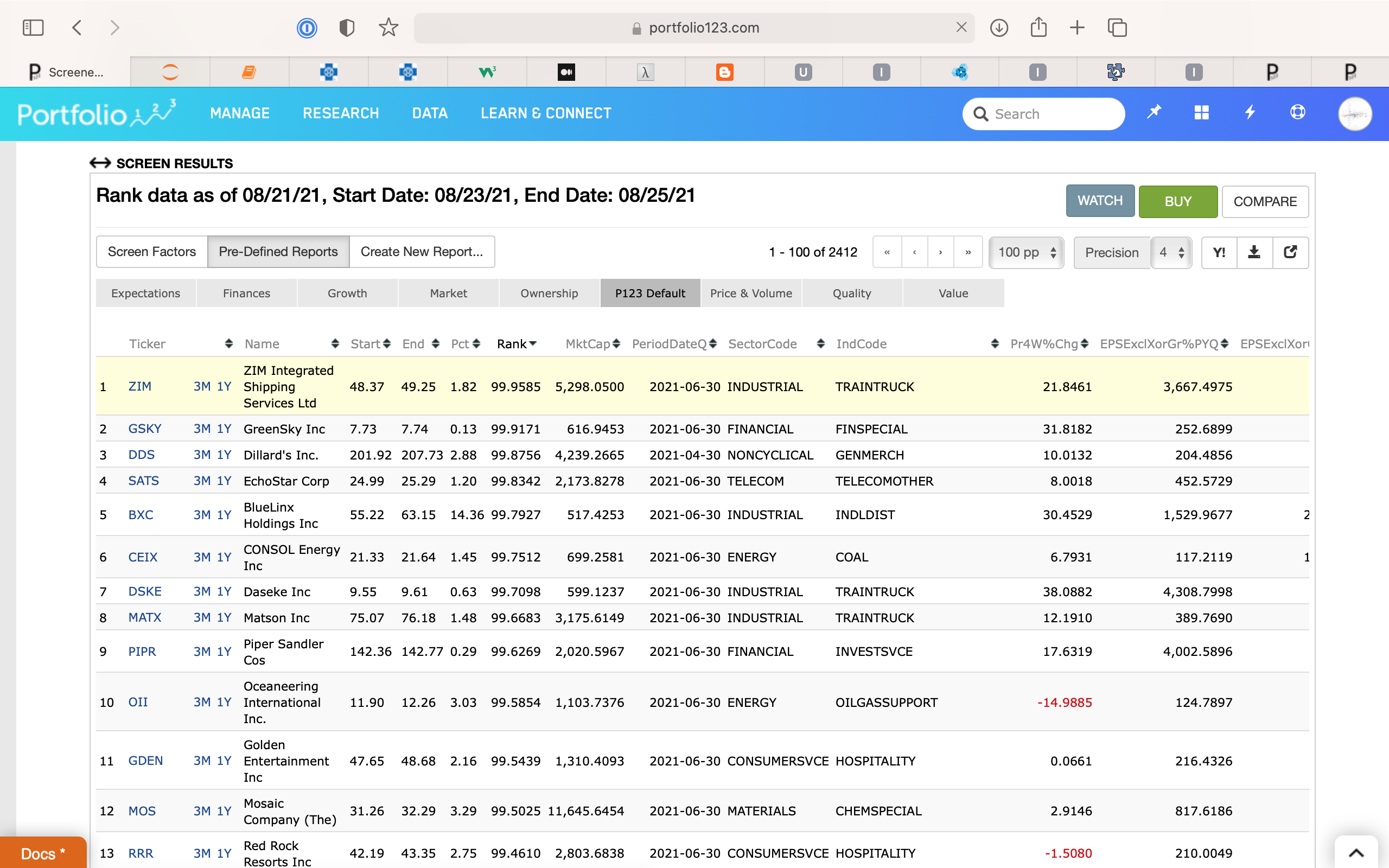

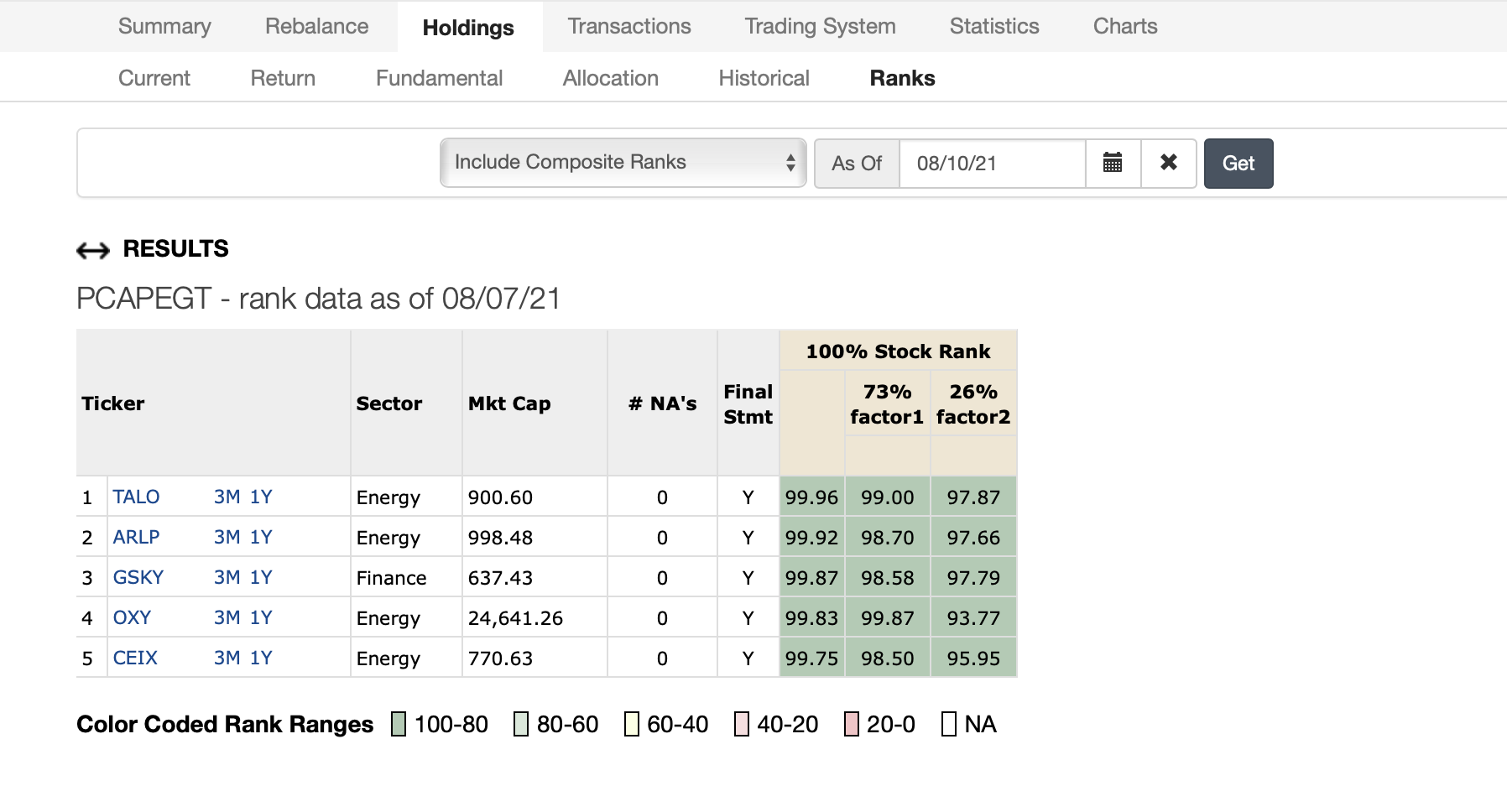

Second image, this morning looking back to 8/21/21.

This argues either way (with this limited data). There is a difference but does it really matter that GSKY and ZIM are switched? You can find some additional differences further-down in the ranks. You can use it to argue either way at this point, I think, and I will leave it at that for now.

Also, will there be more changes when I check this again in the future?

Matthias. Extremely well reasoned!!! I very much appreciate your help with this!!!

I am open to all ideas at this point including: no worries, I should put all my money into this port, there will be a little volatility but I will have my own personal Learjet in no time at all. But I think I will step back for a moment before committing to that. Get a little more data first.

So, just to be clear on what you are saying: It is possible that the port is getting more up-to-date data that–so far at least–is harming my port relative to the sim. Did I understand what you are saying correctly?

I think I might not understand why P123 would want it that way and would ask P123 to explain why they do it this way. And consider changing this if it is true (and possible to change).

Best,

Jim