I have some doubts about the theory or the idea behind the Rebalance Frequency.

I have a simulation that works well in a large period of time, monthly rebalance, but the simulation results improve by few points if I change the rebalance to weekly.

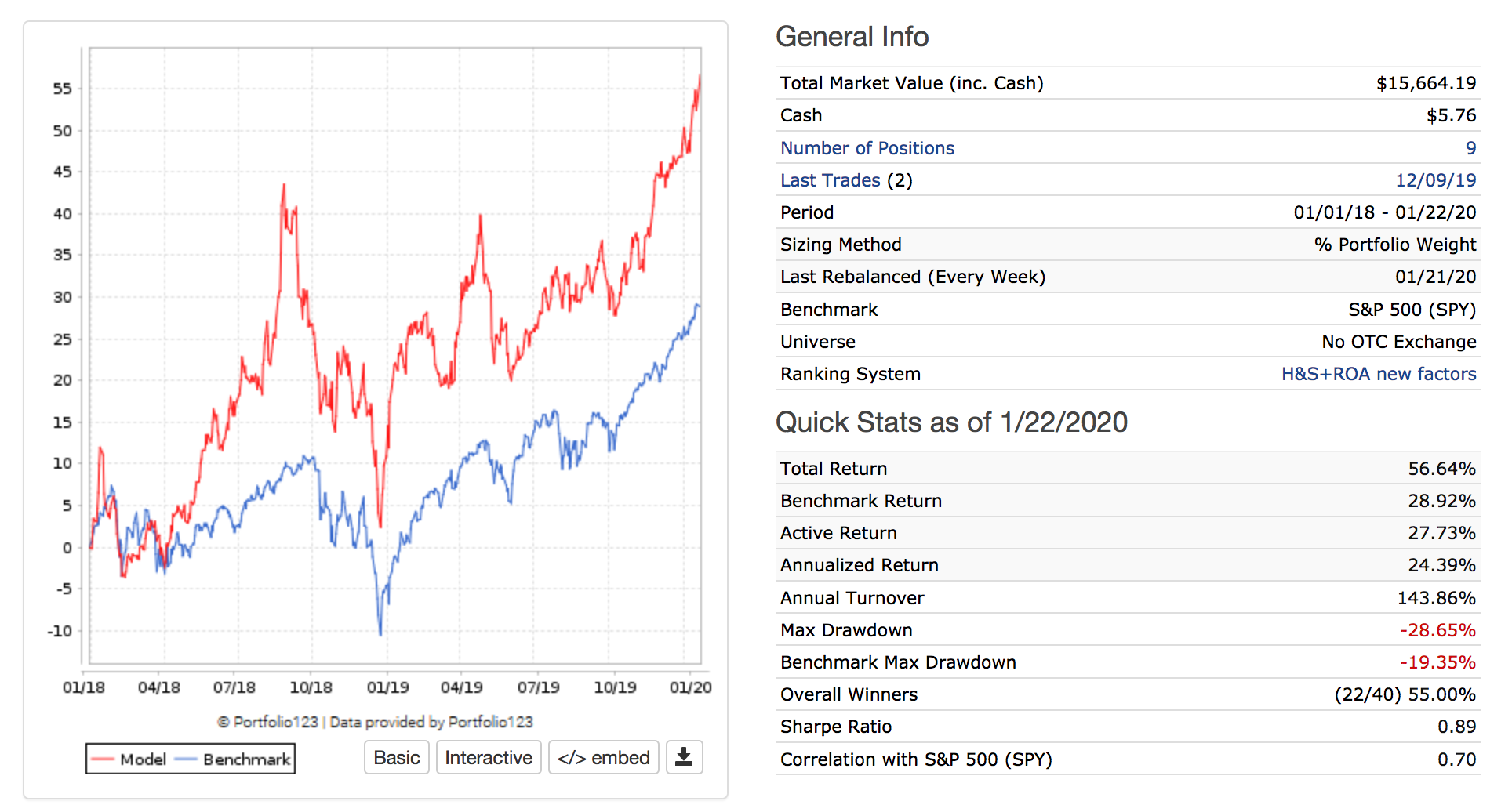

Let’s say it’s a 10 years period, the Annualized return in the sim is 25% in monthly rebalance, and if I change the rebalance to weekly, the simulation gets an Annualized return of 28%.

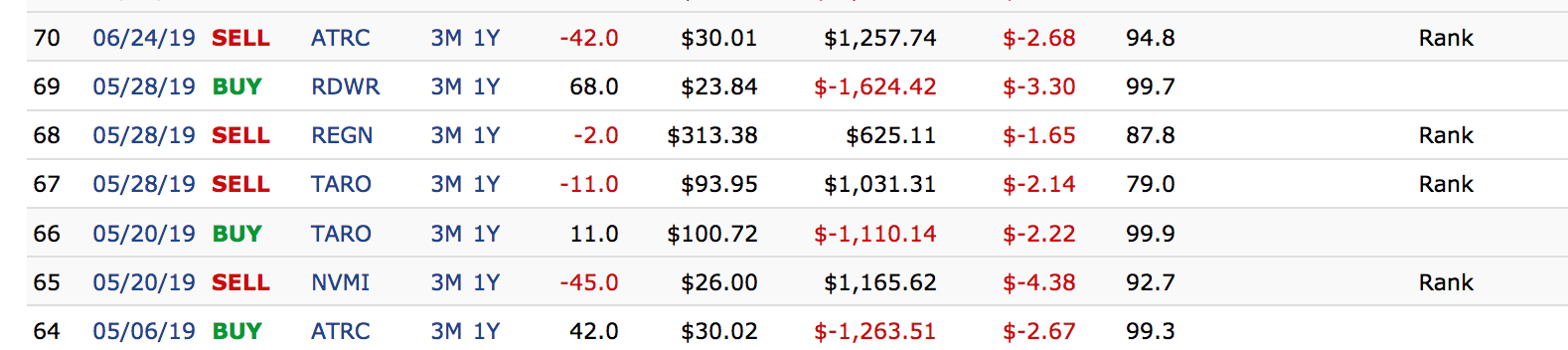

Then I look at the Transactions history, and I can see the simulation trade the same companies, maybe a 10% of the portfolio, selling and buying, this companies almost in each rebalance.

And that is clearly a nonsense to me. Selling a company that I just bought two rebalances ago, and now selling it again… ?!? I don’t get the point…

I have to add that my simulation only have fundamental rules, there are no technical rules.

The thing is:

Should I have to keep the best rebalance period in the simulation, despite the high turnover rate, or keep what my common sense says and stay with a monthly rebalance?

Would be great to ear your thoughts and experience on that subject.

My small-cap model actually works better for higher frequency trading (more frequent rebalancing) - weekly is the best, 1 year is the worst.

And I guess this is better than the opposite situation.

So I would be cautious about your model.

Jaume,

You should test your model using the “Formula Weight” rebalance module. Then you could reconstitute weekly and rebalance every 4 weeks, for example.

Let me hazard a guess. If you’re using a fundamentals-based model and your slippage costs are low, you’re likely using quite a few value-based factors. When a stock’s price goes up (relative to other stocks), it will rank lower; when it goes down, it will rank higher. You are thus buying and selling the same stock but making money on each trade because of the price fluctuations. Buying low and selling high is the best thing you can do as an investor. I’ve seen this happen a lot in my own portfolios. And it works pretty well for me.

If, on the other hand, your slippage costs are high, this could backfire.

There are common-sense ways to reduce turnover without changing the rebalancing period. If you’re using a simulation, use “and NoDays > XX” in your sell rules, and lower the sell rank rule. If you’re using a screen, play with the “Rank Tolerance” setting.

There’s another thing to consider too. Even if you are mostly trading back and forth the same positions, there will be some positions you trade in or out that stay for a much longer time or that you maybe never acquire back. The longer you hold onto a position that no longer satisfies your criteria is going to on average put a drag on your returns and prevent you from owning a better position that should have a better fundamentally justified return.

I think this type of swapping back should be expected and tolerated to some degree with algorithmic trading. It’s just the nature of the beast and what inevitably needs to happen to assure you are holding the best positions based on numerical ranking and screen factors. This type of behavior is going to be more pronounced with momentum, value, sentiment factors as these things are always fluctuating for stocks relative to each other causing noise in a sense.

Have you tried playing around with NoDays in your sell rule and the rank or rankpos at which you sell? That’s the best way to find out if reducing turnover will improve or worsen your results.

But here, I do not understand the use of the rule “Nodays”. Actually, my complain or concern, is for excessive turnover with the same companies. If I add this factor, just I get more turnover, since I force the positions to sell after x number of days.