I have a 15 stock portfolio, and I want the 5 top RankPos stocks be at least three times as big as the 5 stocks with lowest RankPos in the portfolio.

How can I achieve this with dynamic weight?

I have a 15 stock portfolio, and I want the 5 top RankPos stocks be at least three times as big as the 5 stocks with lowest RankPos in the portfolio.

How can I achieve this with dynamic weight?

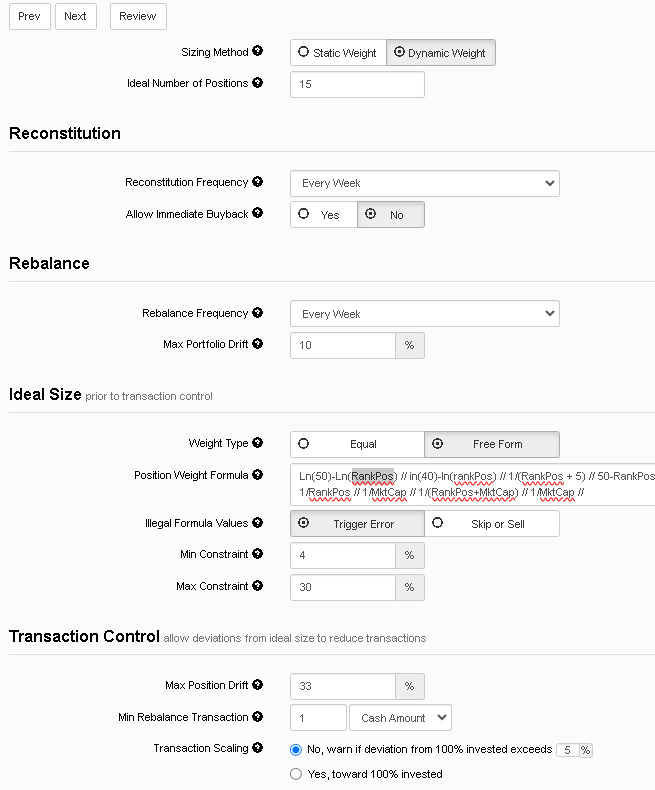

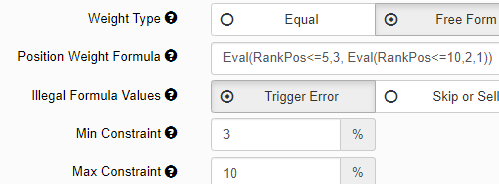

You can use nested Eval() statements to define the weights like this if you want the top 5 to be 3x the bottom 5. If the strategy holds 15 stocks, the top 5 get a 10% weight and the bottom 5 get a 3.3% weight.

Eval(RankPos<=5,3, Eval(RankPos<=10,2,1))

This might interest you too. Position Weight Formula: 100-Rank

It gives them weights ranging from 10% to 3.3% if you you the same min=3% and max=10% settings.

Is it possible to combine this solution - to Yuval: How to dynamically weight new positions without rebalance - #3 by primus

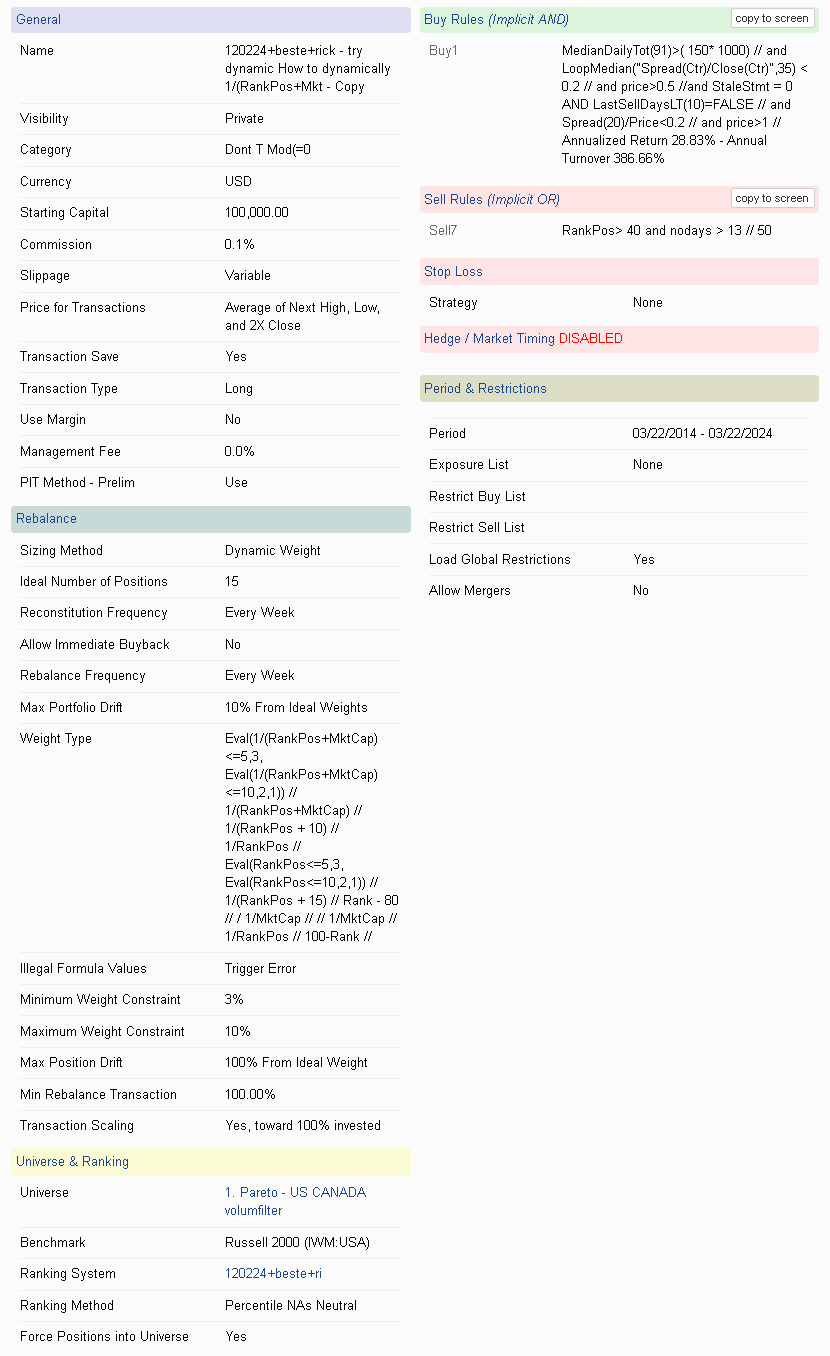

With this: Eval(RankPos<=5,3, Eval(RankPos<=10,2,1)), but where the Eval(RankPos<=5,3, Eval(RankPos<=10,2,1)) has something like this: Eval(1/(RankPos+MktCap) <=5,3, Eval(1/(RankPos+MktCap) <=10,2,1))

You could combine this with the settings mentioned in that other thread. I cant answer if that combination will produce results you like. You should experiment with the various settings available for Dynamic Weight and check the transaction history on the transactions page of the sim to see if it is behaving the way you intend. Also be sure to look at the Charts tab in the sim because some of these settings can cause the % Cash Invested to go way over 100%.

OK, thank you!!

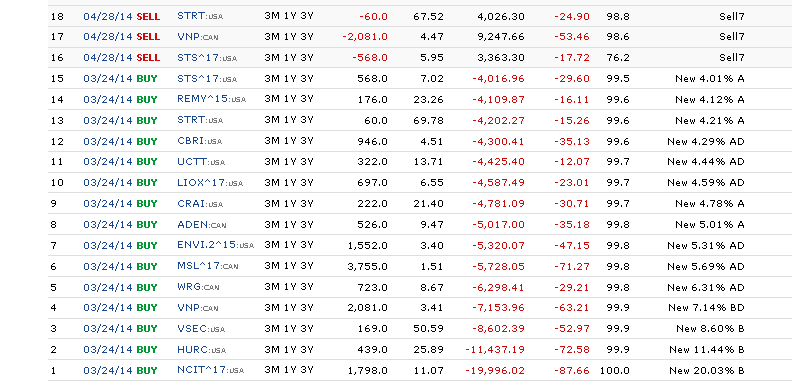

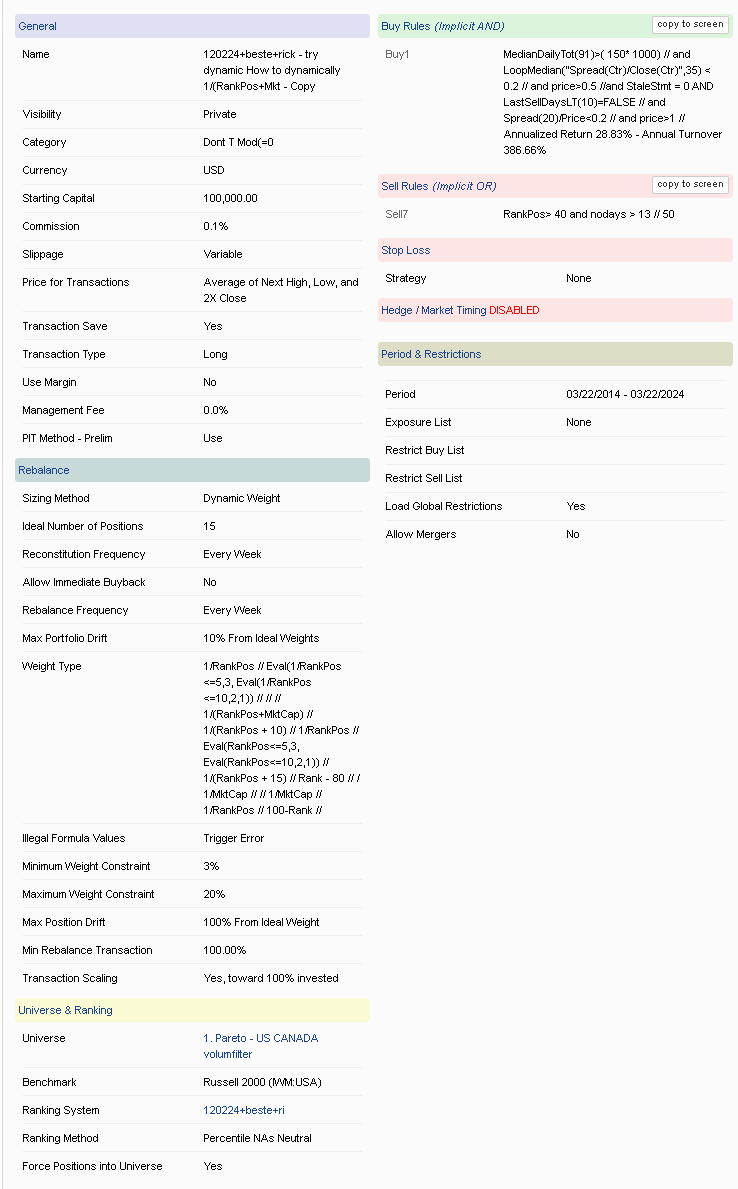

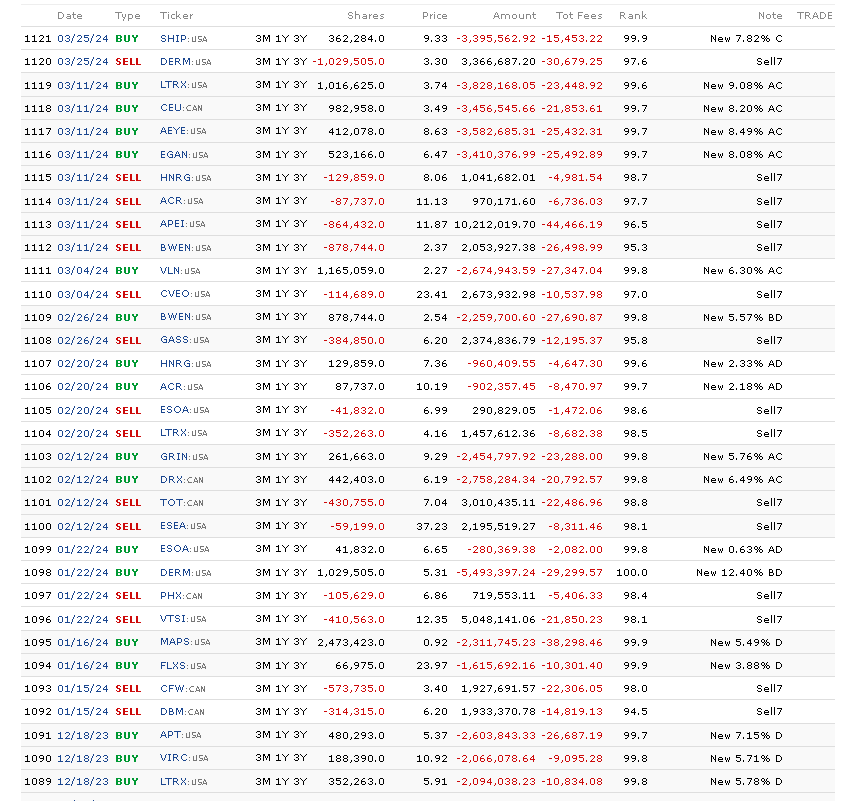

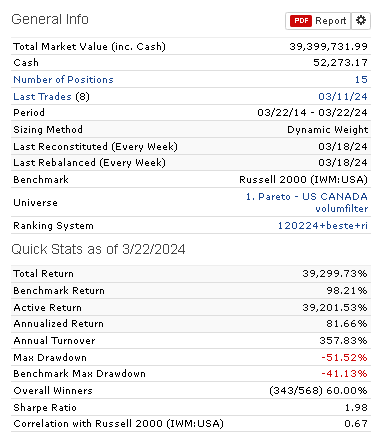

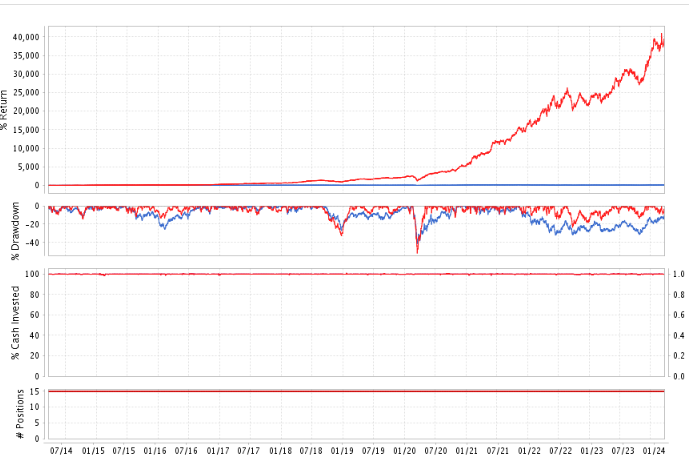

I have tried different solutions here, and just to make sure that the results here aren't to good to be true.

This strategy is "to be reconstitute without rebalancing" each week like described here: How to dynamically weight new positions without rebalance

And each week it reconstitute, but only with a maximum position weight on 20% and a minimum weight of 3%

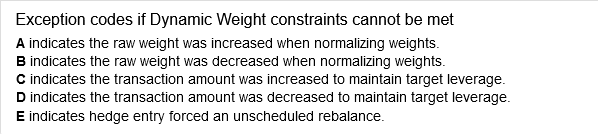

Sorry, Yes thank you, I saw this at the end of transaction overview