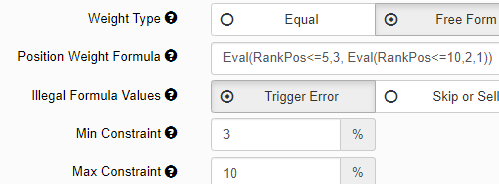

You can use nested Eval() statements to define the weights like this if you want the top 5 to be 3x the bottom 5. If the strategy holds 15 stocks, the top 5 get a 10% weight and the bottom 5 get a 3.3% weight.

Eval(RankPos<=5,3, Eval(RankPos<=10,2,1))

This might interest you too. Position Weight Formula: 100-Rank

It gives them weights ranging from 10% to 3.3% if you you the same min=3% and max=10% settings.