All,

Riccardo is reportedly adding some options for using a correlation matrix and ETFs. As I understand it, he has a finance degree but does not choose to participate in any discussions about diversification in this forum.

I definitely understand that. Likewise, Hem has not chosen to post recently. Marc is gone. We are told there is an AI expert somewhere at P123. No word about his interest in this topic.

The important questions on this topic are quite simple. It is finding the best answer for any single member at P123 that is hard. I do not mean to imply that the answers are easy (just the questions). This has all been trivialized at P123.[color=firebrick] The P123 forum is at best a competition as to who has the biggest…uh, returns. Won by the person who can find the best cherry-picked, overfitted or anecdotal example. Nothing more can be expected of P123 at this time with regard to mainstream considerations in finance.[/color]

I still think 2 question matter: 1) Is it possible to get increased returns with decreased volatility by using mean-variance optimization (perhaps with some leverage)?

I seem to recall there may have been a Nobel Prize for some ideas on this. And there are some newer ideas.

Question 2) that may not apply to everyone: If you are at or near retirement are you willing to give up some return (if necessary) in order ensue that you will not run out of money with a large drawdown and be able to continue to withdraw a minimum amount to live on each year until you die. Thinking you may not be in love with the idea of generating new income mowing lawns when you are 85 years old if there is an unexpectantly large drawdown.

[color=firebrick]The Kelly Criterion addresses a third (separate) question if one decides to use at lot of leverage: How much leverage is safe and will give you the highest returns?[/color] Again, I do not think these questions are particularly difficult to understand nor do I think they are unimportant for everyone at P123.

There is an article by Pimco (referenced) and post that attempts to put some of this together into one theory: A Bond Fund’s View on Risk. Some have said this is too complex for P123 members. If what Yuval says is true in this regard, maybe Riccardo will help at some point.

Maybe we can hope for something from Riccardo on this in a bit. In the meantime we have Portfolio Visualizer, other sites and Python libraries to help with these questions.

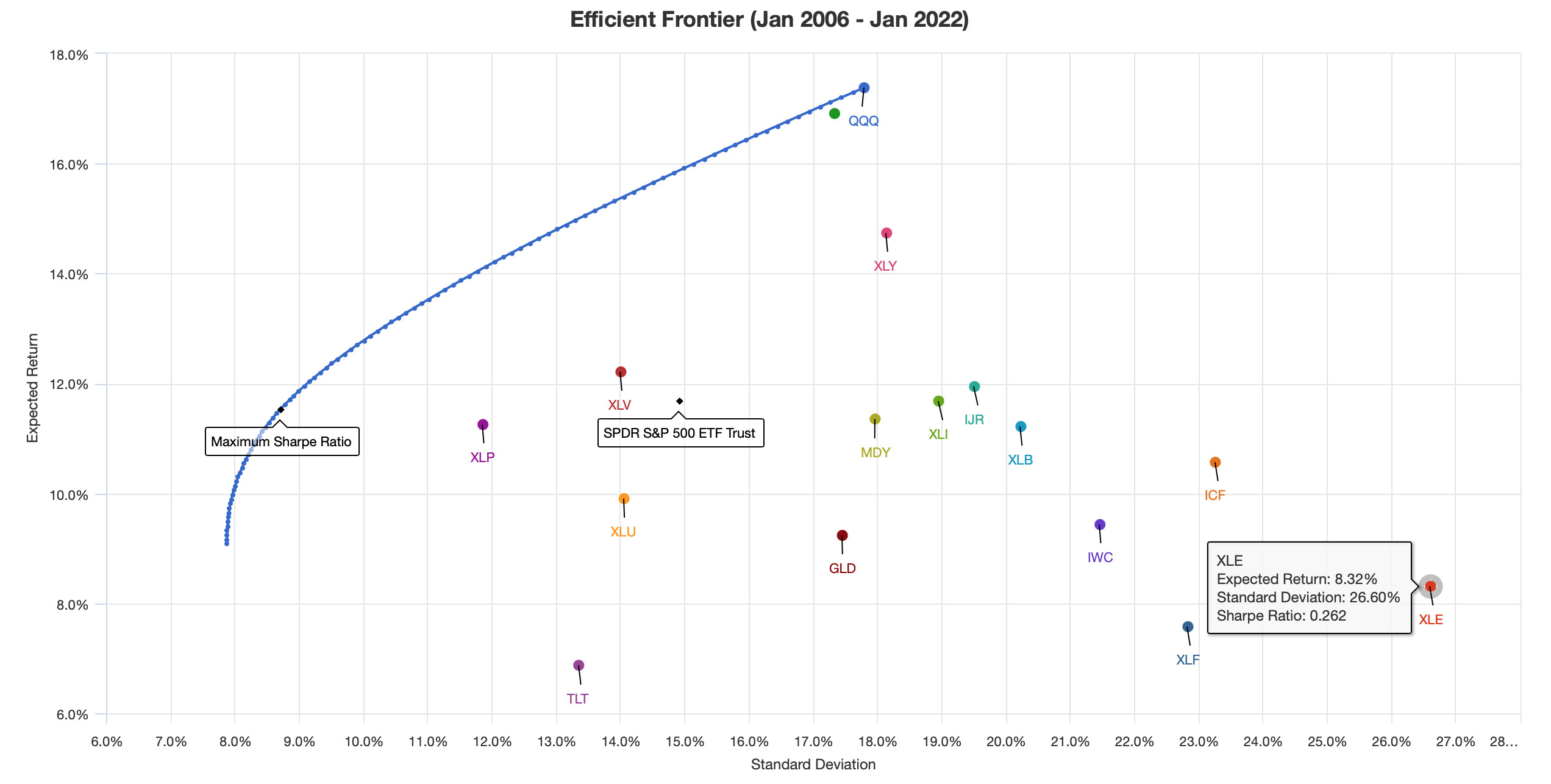

Here is something like the assets one would find in the security-market-line as a start. But this is not really a topic for discussion at P123.

More realistically, maybe we will get an overfitted backtest from one of the members (or staff) that will be represented as the final word on this (no Nobel Prize or even a finance degree required): I leave the floor to whomever wishes to think an overfitted in-sample backtest is the final word on this. Riccardo and Hem are welcome to reply also but I think I would die holding my breath waiting–in which case this would all be academic anyway. And BTW, I am not looking to mow lawns when I am 85 years old either. But that could just be me.

If you are an [color=firebrick]“optimistic”[/color] investment advisor no need to worry about any of this of course.

Best,

Jim