It was a long time ago, and not on p123, but do recall testing days of the month using a technical trading software (Amibroker) testing the premise that automated 401k contributions based on pay periods in middle and end of month might have influence on overall market prices. I recall periods of the month were stronger roughly consistent with the hypothesis - and do think it carried over into the beginning of the next month. Don’t know if I ever traded it or what a real explanation might be or if just a fluke. fwiw, I’ve always found going in and out of positions quickly never suited my personality, and there’s always the problem of idle cash that the activity generates that has to always be redeployed in another idea vs. slippage/trading costs.

Again, haven’t tested it with p123, so don’t know the degree that such effect, if still present, would disparately effect sell price action for sells vs. the buy price action of the new positions if using for rebalance date. I haven’t tested if those time periods are better to sell into or buy into. I’m just thinking out loud here, and I can’t recall if there is an effect on trading volume, but if liquidity is better on some predictable days than other, it could help reduce spreads/slippage and that could be beneficial. Psychologically it may be easier to sell during mostly stronger times of the month even if both what you’re selling and what you’re buying both go up. (Or if you’re like me it might just cause stocks I’m trying to buy to run away from me. )

I have several simulations which show the highest return when trades are specified to occur only on the first trading day of the first week of a month, or on the first trading day of the fourth week of a month.

Trading set to occur on the first trading day of the second week of a month, or on the first trading day of the third week of a month produces significantly lower returns.

I have never figured the reason for this, but the effect of EOM anomaly could explain this.

If you you are using a trend-following strategy, trading just after the 1st could be the earliest opportunity to pick up on a new trend. If there is truly a turn-of-the month effect that bounce at the beginning of month could be the first clear signal of a trend. The first clear signal of a shift in sentiment.

I would be interesting to look at strategies based on fundamentals, earnings revisions or analysts recommendation and compare those to strategies that use momentum or relative-strength.

What got me thinking about this is that I rebalanced a strategy (based on relative-strength) October 1st. After reading this thread I kind of wished it were easier to rebalance it at the end of the month. But then I remembered I had looked at that to some extent (as you have).

Georg, like you I have looked at rebalancing this relative-strength strategy at different times and the first of the month was best for this strategy also.

Perhaps the trend often starts at the first of the month for reasons often mentioned–like money from pension funds, people rebalancing on the first etc. But also, a port based purely on fundamentals (no momentum) could possibly do better at the end of the month if it is based on data that masses will be noticing soon when making their investment decisions at the turn-of-the-month.

I have only tested this with a single relative-strength strategy that did best at the first of the month on backtesting. Also Georg presents some interesting data that may or may not use momentum, relative-strength or moving average cross-overs (Georg can comment if he wishes). Other than these examples and the literature on the turn-of-the-month effect I am speculating. So just a hypothesis.

The EOM phenomenon has been around for as long as I can remember, but it is the last week of the month, not the first week if memory serves me correctly. Part of the explanation may be mutual fund window dressing but that would likely be at the end of the quarter. Geov - if you are interested you might check to see if the phenomenon is more pronounced at the end of the quarter as opposed to end of each month. I’m curious anyways!

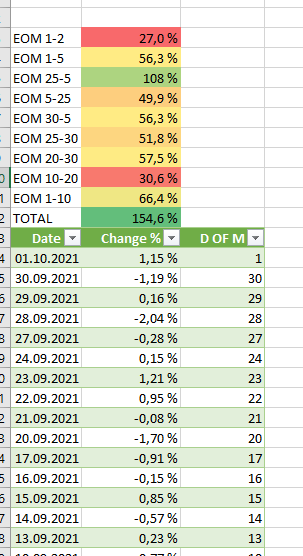

I also conducted additional tests to determine the strength of this effect. For the period 2006-2020, the S&P 500 was used. It is based on daily price.

According to the numbers below, it appears that the major indices begin their rising trend a few days before the end of the month.

Since I do not have access to the simulator, I have not yet tested the effect on a strategy.

I tried putting the strategy on the “daily” screen and applying the filter “MonthDay> 28 OR MonthDay 3,” but I got such a bizarre result that I’m not sure the rules function well enough to force a rebalancing at the proper time when employing rebalancing.