Using the P123 Piotroski system and adding liquidity criteria and EPSCurrYr timing gives me a long holding period (about 200 days if I remember correctly), avg return/trade over 30%. Increasing the turnover does not seem to help performance.

The ETF ranking systems seem different but it may be due to my lack of experience in thinking this way.

I am going to try the forder approach you suggest as soon as I have a little more time. Thanks.

It seems like the sell rules (with the exception of trailing stops) are only evaluated at the rebalance. In that case, I need to incorporate something like what Denny demonstrated.

I’m starting to look into ETF ranking systems to use in my Fidelity 401k. They have a number of ETFs that trade commission free which is of use for low capital or higher frequency systems, though trading restrictions are 30-day minimum for the free ETFs.

Is anyone willing to restart this discussion or share a starting point for an ETF ranking that would work well under these constraints? Thanks!

Caley, some momentum factors actually do better with four week rebalance rather than weekly. Thirty days is close enough to four weeks to make it work.

I don’t have a ranking system but I do have some suggestions on designing an ETF book which did not exist a couple years ago.

Diversify with stocks, bonds, gold, ( I don’t like resources)

Diversify with many designers including yourself.

Use different market timings and Hedging

Here is a book that would cost less than $100 and by playing with the Assets and Hedging you can get the drawdown lower than 8% with a return of 20%. This might not suit your needs for free trading but it would come close since it is low turnover.

Is there a way to see what portfolio are responsible for what % of the total book return? And I supposed there’s no way to see the underlying systems of 2 of the 3 since they are R2G models.

In the book click statistics and then click Risk to see the individual results. You can also create your own book and just add the smart alpha models individually. This will give you much more detail and history.

There is no way to see smart alpha models but both of them have about 2 years of OS. One is all bonds and the other acts like a Hedge using stocks. Not much OS so it makes me nervous. Not to mention all the bad press about Bond ETF as the next bubble but there is not much choice.

• When markets are good there is 33% bonds and 67% stocks (More if you use leverage)

• When markets are bad and all portfolios are bullish there is a minimum of 33% bonds, 33% Short Stocks and 33% cash.

The timing is not right all the time so it will be interesting to see what the future results are. I expect it to beat the market by a few points over the next ten years and to suffer some heavy drawdowns during the next bear market.

The concept is when times are good add more stocks and during bears short and go to cash at the same time always be diversified.

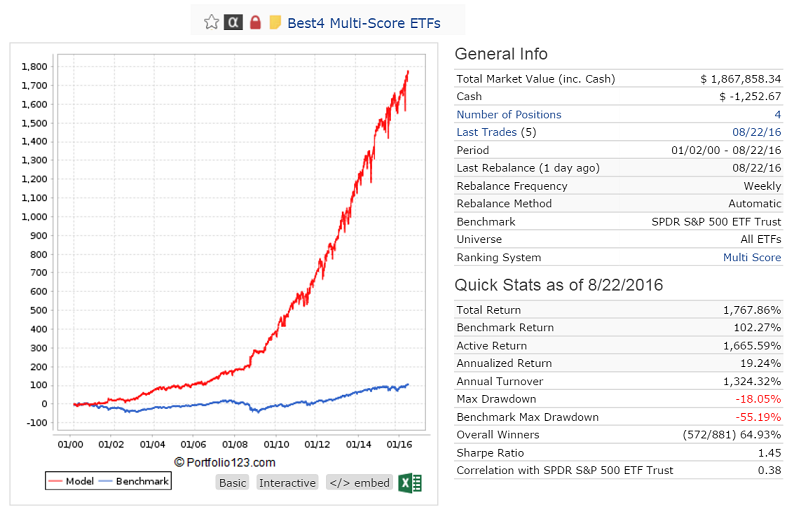

No, not the Best2 MC-Score System. Return is a bit too low for SA. You can easily recreate this model from the information given. I have a SA in incubation. Best4 Multi-Score ETFs. https://www.portfolio123.com/app/r2g/summary?id=1438590

Turnover is a bit high.

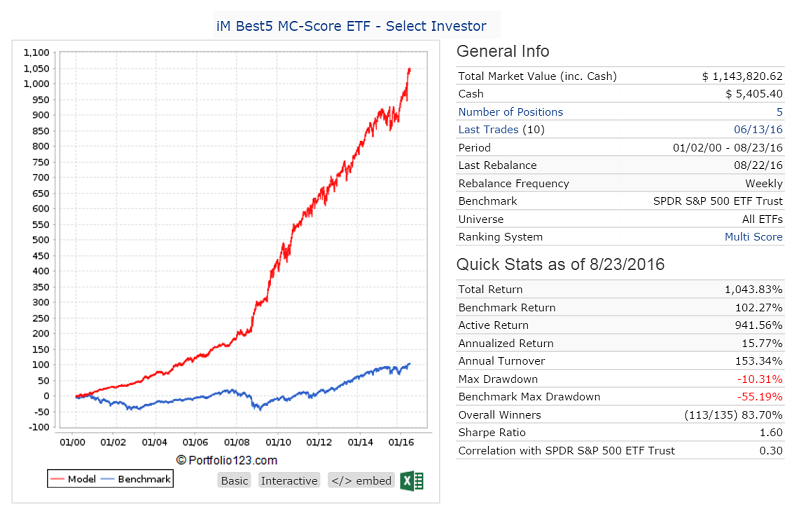

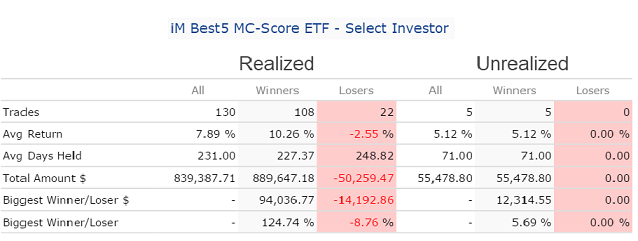

It is easy to bring turnover under control. Further down is the iM Best5 MC-Score ETF - Select Investor. Holds 5 ETFs, has an avg. turnover of 150% and still provides a decent return. Only 135 trades in 16.5 years, CAGR= 15.8% with a max D/D of -10% and a win rate of 84%. You can’t do much better than this.

You mention it’s easy to create but I’m not as quick as you. Would you mind sharing the general process I don’t need the detailed calculations. I presume you need to use the EVAL function and nest multiple conditions to create a buy signal at the same time use a counter or just have the evals pick the ETF’s based on thresholds. I have not seen anyone post this publicly so you could be the first.

This method works well in a screen, but in a simulation one gets thousands of Buy/Sell Difference trades. One has to rebalance weekly to pick up the signal when the MCS changes, but when there is no MCS change the model always sells and re-buys weekly the same ETFs causing these annoying small Buy/Sell Difference trades to be generated. Because there are so many of them one cannot possibly trade them all, but they have a significant impact on overall performance of the model. However, I have figured out a formula to prevent the majority of these trades to be eliminated, but it only works for the MCS models.