Hello fellow traders,

I'm currently exploring strategies for protecting my crypto portfolio against market downturns using options and am keen to delve into the nuances of selecting the most effective options for this purpose.

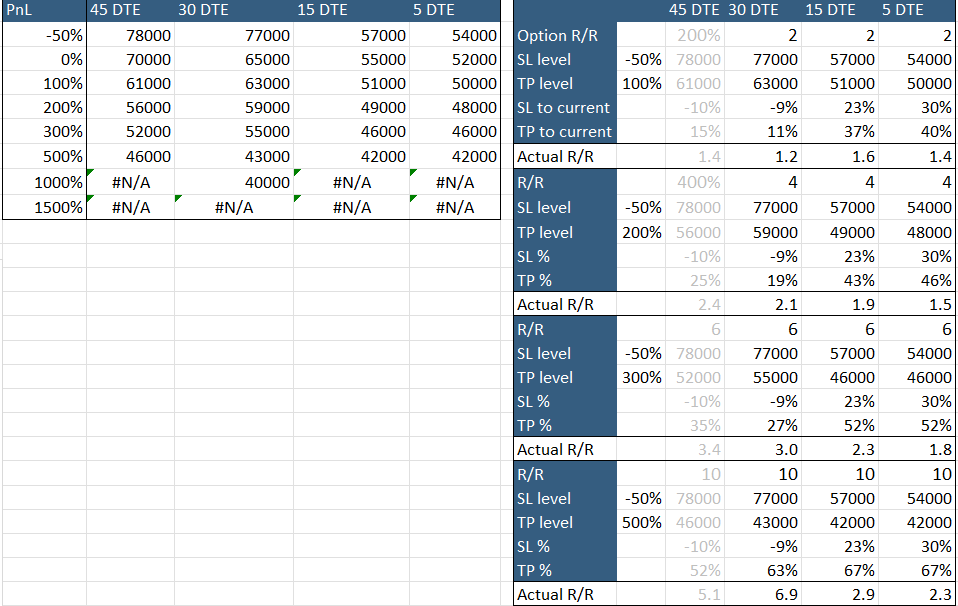

Context: My primary focus has been on buying put options based on their estimate worth (using B&S w/ different DTE and IV multiples).

I thought about a thought process with options to get a potential R/R (like we do with Spot/Futures trading.

Example:

-

Option R/R: 2 (-50% downside w/ 100% upside)

Then I looked levels for an option (at set DTE & IV) to reach that goal (minimum) -

Actual R/R (inspired by trading futures/spot experience): dividing these levels as they were SL/TP to current price

-

Validity of Approach: Does the emphasis on lower actual R/R ratios as a measure of attractiveness hold water? Are there scenarios where this metric might be misleading?

-

Additional Considerations: Beyond the actual R/R ratio, what other factors does options traders prioritize when selecting options for the purpose of hedging against downturns in the market? I'm particularly interested in how experienced traders balance cost, hedge effectiveness, expiration dates, and market volatility in their decision-making process.

-

Strategic Insights: could you share insights or examples where certain strategies or option characteristics outperformed others? How do you integrate these into your overall risk management framework?

Your insights and experiences would be incredibly valuable for refining my approach to using options for crypto/equity portfolio protection.

Thank you in advance for sharing your thoughts and strategies.