Any insights as to how much longer this factor inversion in small and microcap will last. One of my main KPIs is looking at my strategy vs the R2K, and this is YTD period is one of the worst I’ve seen.

I built something for this.

If you are ok with it, provide the ranking system or factors you want to analyze and I can spit out an historical analysis, which should help frame things for you.

I started working on trying to understand and predict them. I have a decent hypothesis for generic stuff. I have another post providing some of the output.

In some ways I think participants’ simplistic heuristics are working against them. For some, a low p/e means its a value/undervalued stock and a high one an overvalued stock which is a view detached from reality. It is usually the same people that say and wonder why value is underperforming? that wonder why expensive heavily shorted stocks do well? Here is a hypothesis: if that thinking continues high pe should outperform and low pe should underperform very regularly.

Added to that, why would expensive stocks not get more so if the participants chase after them? Many mechanically so like ETFs which dictate things more by sheer size of flows even if one assumes hedge funds are 3x levered. Not to mention, now ETFs are also levered too and looking to make 5x available.

In financial markets, the participants are part of the phenomenon being studied by the participants themselves leading to seemingly paradoxical yet explainable stock market behavior.

I don’t really wax poetic about this stuff. People think they can get rich quick and piling into stuff like garbage Quantum Stocks. It happens from time to time. It will look just as stupid as when people piled into garbage stocks in 2021 in hindsight. As a quant modeler what are you going to do? I’ll never build, much less stick with, a model that puts me into Peloton in 2021 (or Rigetti in 2025).

The good news is the inversions seems confined to the US markets. It’s been a great year if you’ve been diversified internationally in traditional quant factors. My US models have had their worst year against their benchmarks in simulation or out of sample, but I’m very happy with total ytd performance as a whole thanks to large outperformance in Europe and Canada using largely the same factors

3 Likes

Definitely a lot of that going on- and on margin

1 Like

You're right.

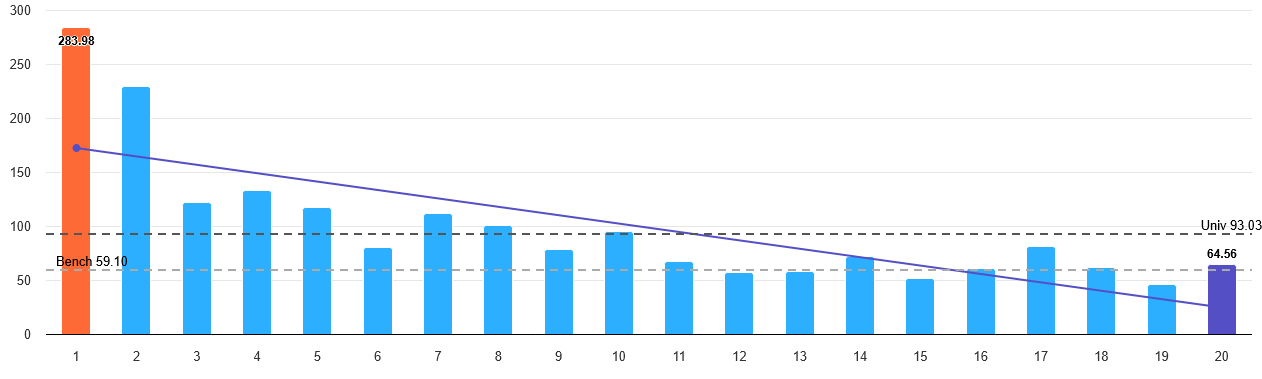

Russell 2000 universe, evaluative ranking system that I created in 2023 (so all out of sample), last six months, rebalancing every 4 weeks (all returns are annualized):

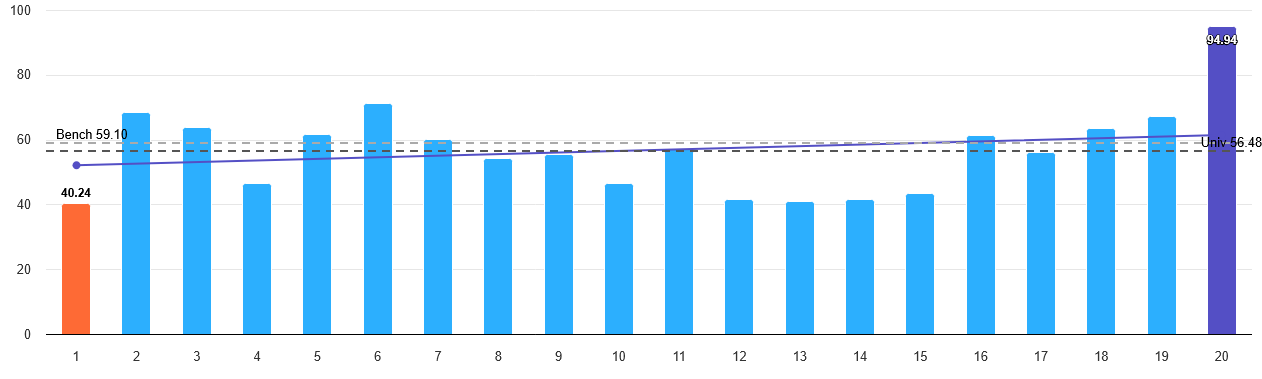

I created a similar universe for non-US stocks: exclude the top 1000 Canadian and European stocks by market cap, include the next 2000. Same test:

7 Likes

Is it connected to the crypto “sh**coin” gambling phenomenon? People claim to be using up to 50x leverage.

1 Like

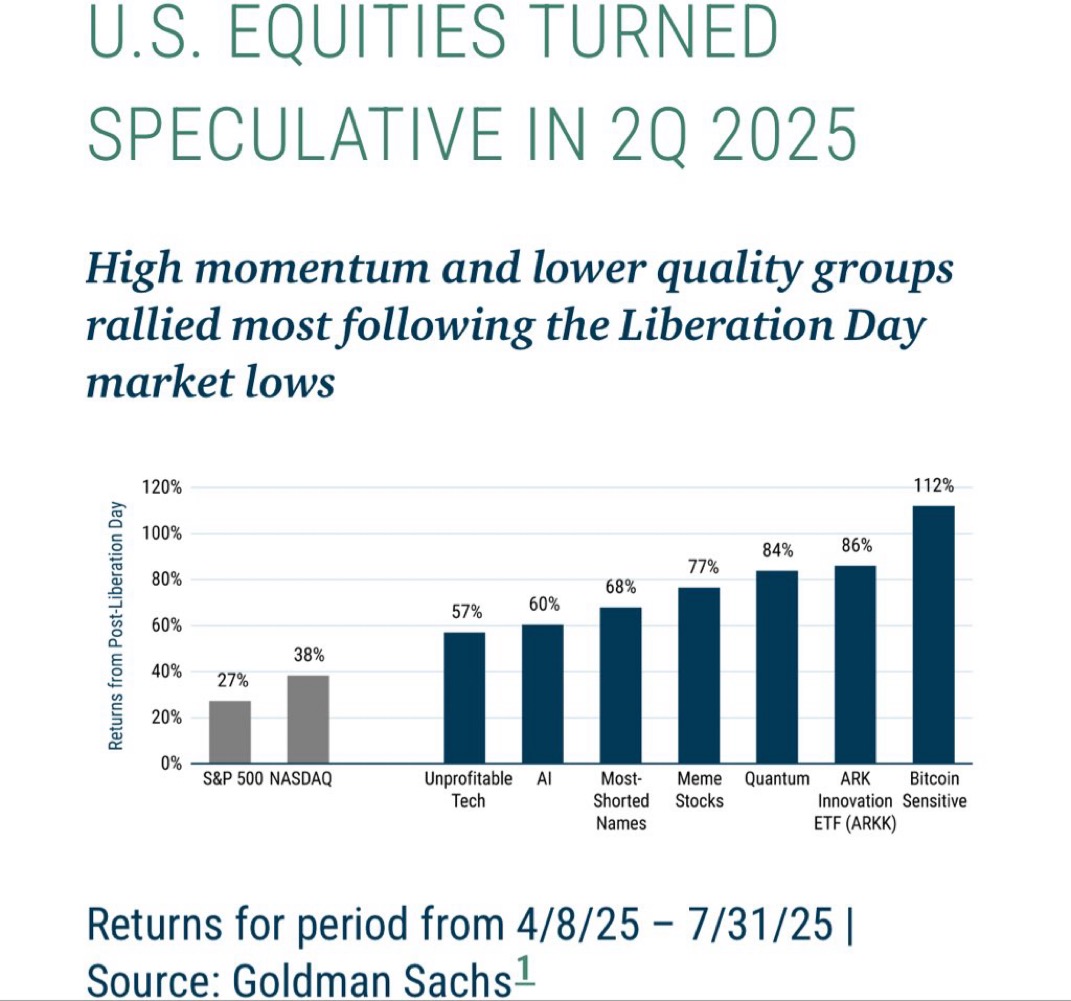

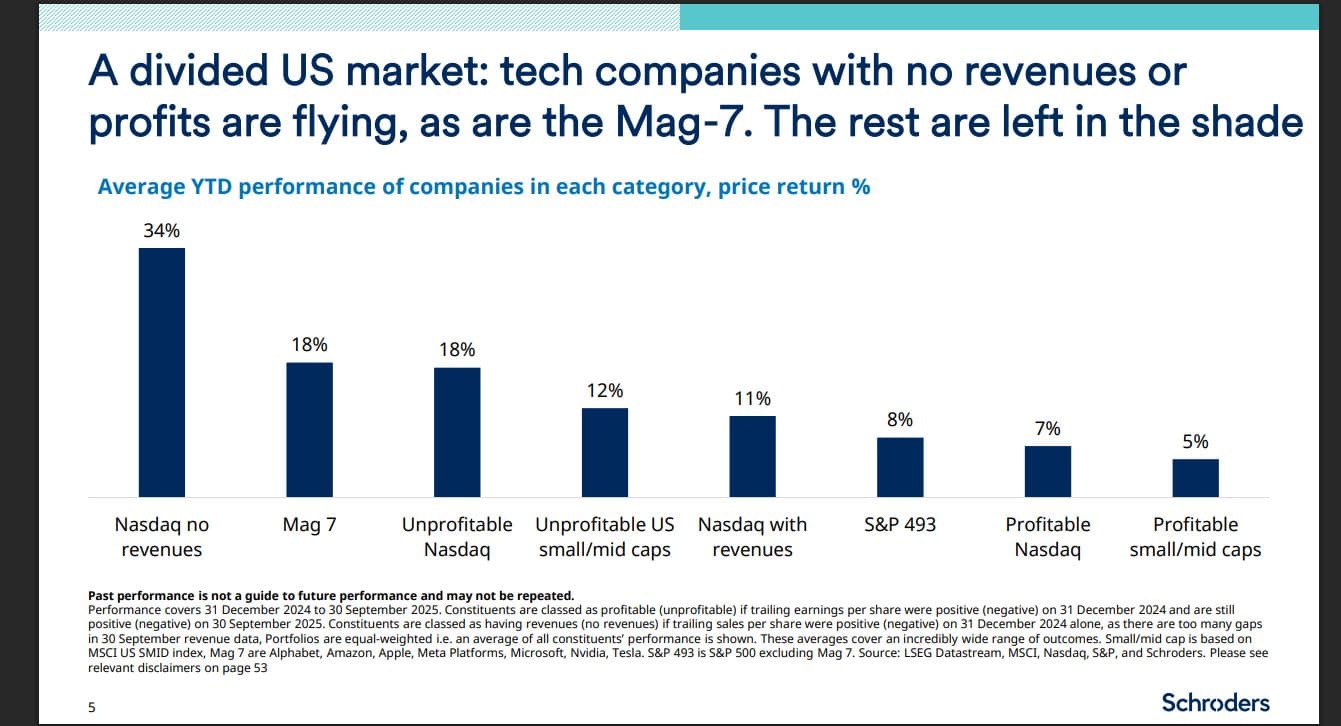

I think it’s downstream of AI Mania that is particular in US markets right now. People are piling into any unprofitable junk they can find as long as they can loosely attach an AI story to it. On the other end, any generic non-AI story company is hated/ignored. They’re still expected maintain/expand margins by The Street, often despite rising input costs from tariffs, otherwise they’re ‘falling behind to AI’. (too bad FactSet doesn’t go back to the mid-late 90s so we could draw data driven parallels).

Meanwhile, the mania hasn’t seem to hit Europe, and Canadian stock market has had huge tailwinds with the gold melt up.

1 Like

AI, Quantum, Unprofitable tech, futuristic tech, gold, crypto (rip smaller crypto) etc. basically stocks or assets where there is a lot of uncertainty, low visibility, and high potential even if low probability. They have no fundamental predictable cashflow grounding like say a bond has. The less fundamental grounding you have, the more room for bias to take over and be self reinforcing.

Basically, a highly speculative environment

3 Likes

And now they’re not even going to be required to report numbers quarterly.

Matter of time…and mister wipe out will do his job

1 Like

Must be largely driven by the tariffs. U.S. companies that struggled to compete in the market received a boost in the U.S., while “quality” companies that can still compete in the rest of the world are appreciated.

I have some out of the money long term puts on rgti/quantum as a hedge

1 Like

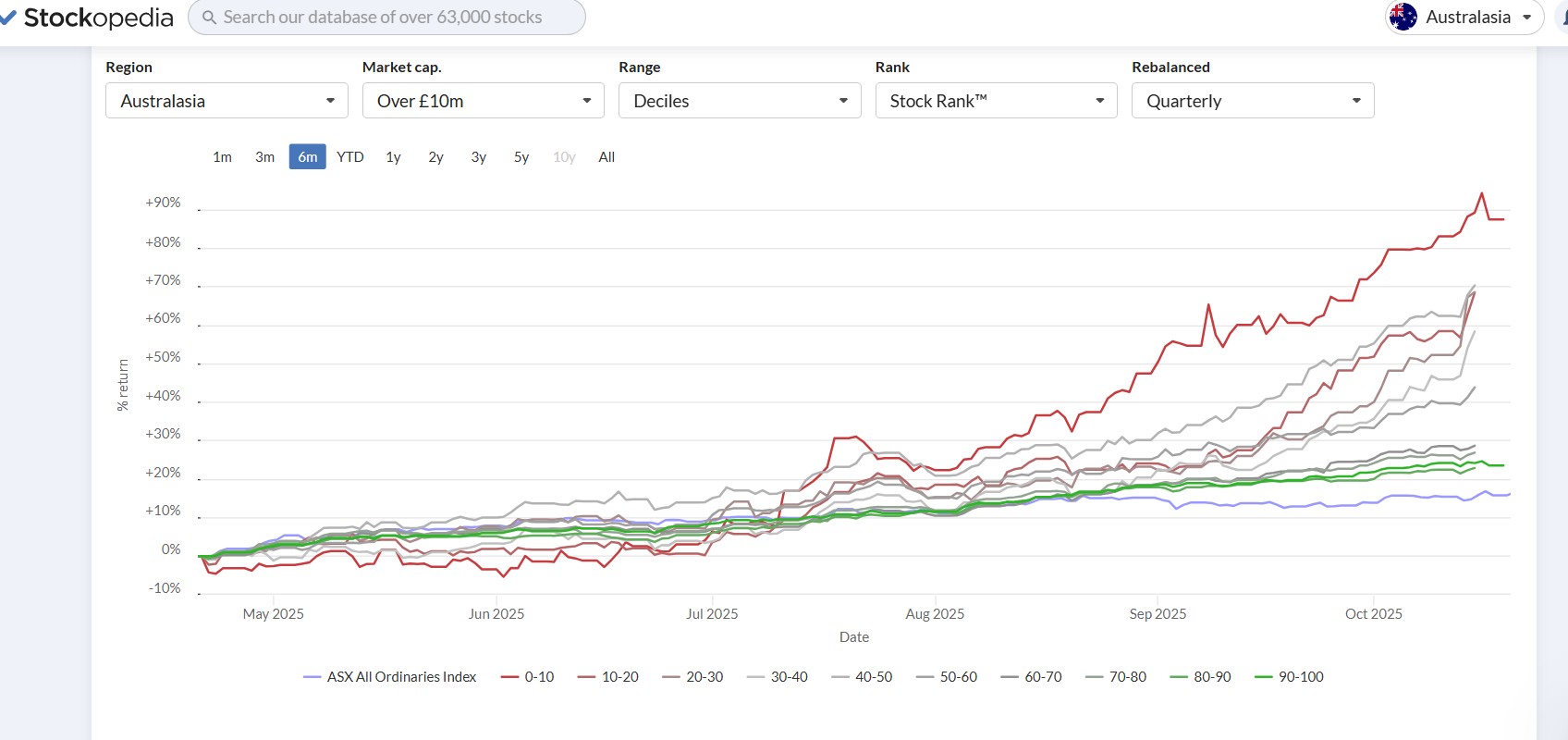

This is Australia/NZ, last 6 months. Stockopedia has a ranking system (value/quality/momentum) which has inverted also.

1 Like

It’s just 2021 all over again. Will be temporary. But this year really shows the benefit of global diversification. Europe/Canada Microcap Multifactor is on fire. US micro is doing okay but lags hard this year.

1 Like

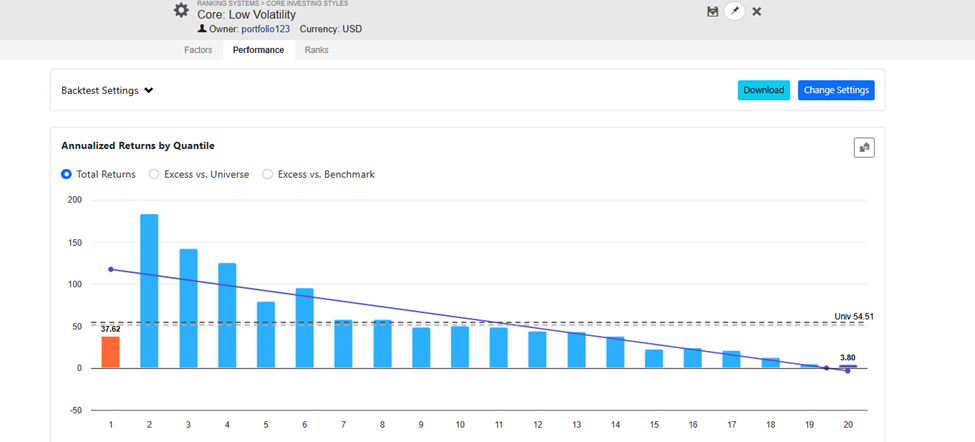

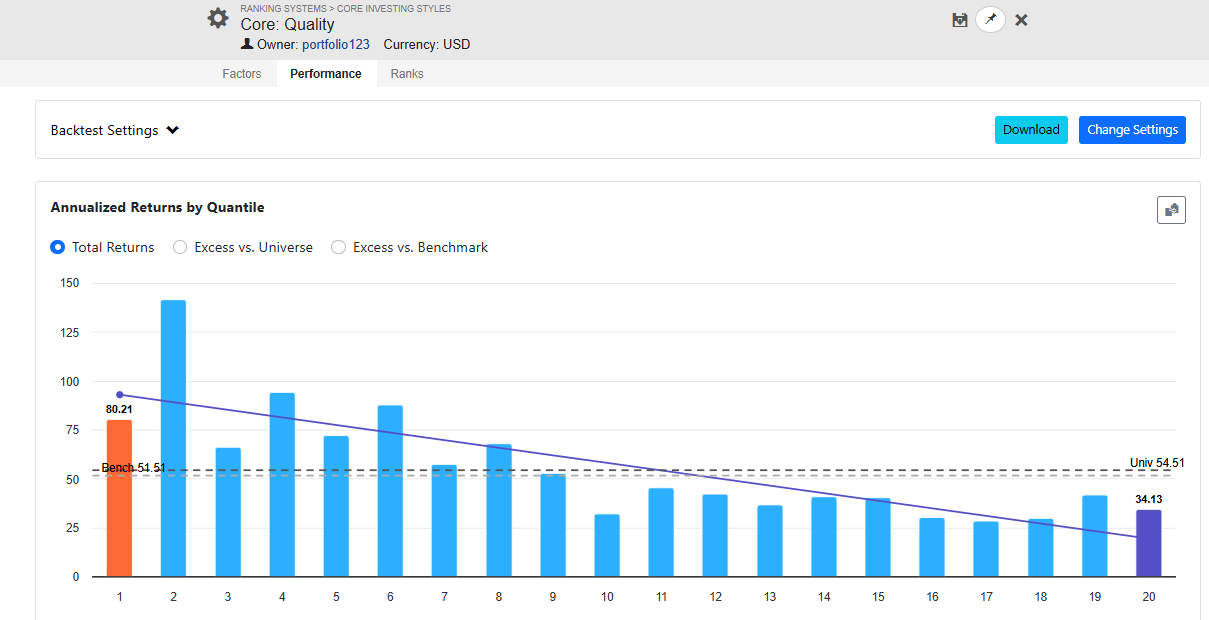

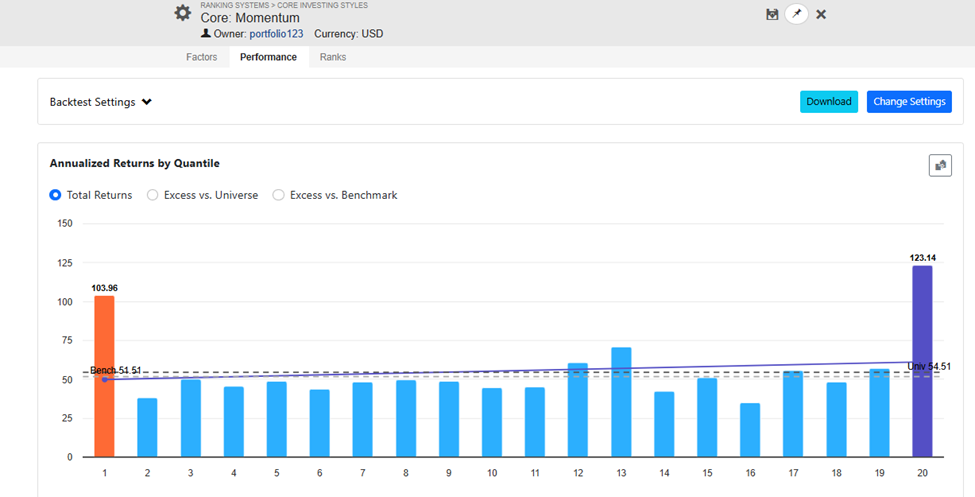

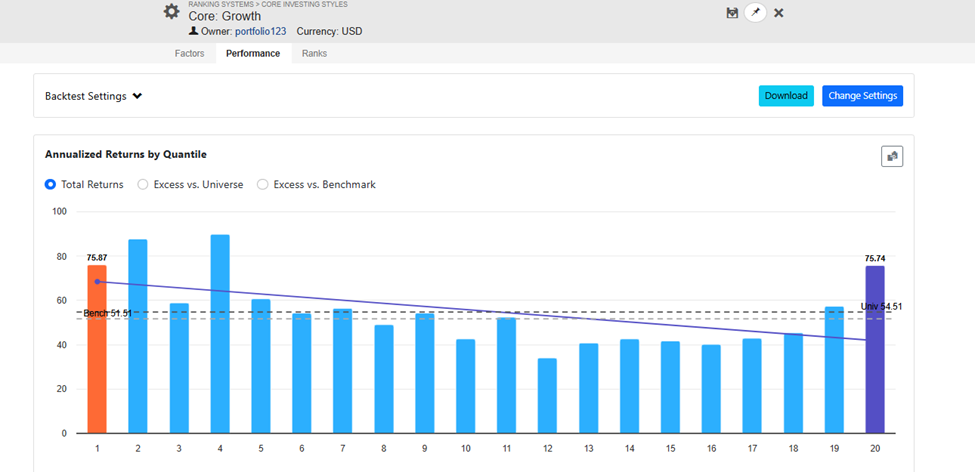

Interesting to see what core styles have worked the last 6 months (~post Liberation Day rebound) against Easy to Trade US universe.

Brutal for low vol.

bad for quality and value.

Great for the highest momentum bucket.

J shape for growth.

which brings up the enternal question of factor timing. How confident would you be piling into high momentum/high vol trend currently without a reversion in the near term?