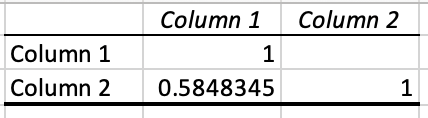

Just for fun I took the rank of 100 (sorted) stocks for a P123 ranking system with about 30 features on 1/7/23 and the ranks of the same (sorted) stocks (with the same ranking system) on 9/9/23.

The 100 stocks were randomly picked by their P123 stock ID (starting with the lowest ID number).

Then in an Excel Spreadsheet I found the Pearson correlation of the 2 ranking systems:

Conclusion: The author's findings about autocorrelation of factors over an extended time period may apply to P123 ranking systems.

I should have noted their conclusions in their words:

As in Lettau and Pelger,19,20 we argue that focusing more on cross-sectional fit and less on global fit is beneficial to out-of-sample portfolio allocation.

Our second core finding is that accuracies (and profits) are the largest when the predictive models are built on deep samples and when the dependent variable is the long-term future return. Third, we document that important drivers of returns depend on the horizon of the returns.

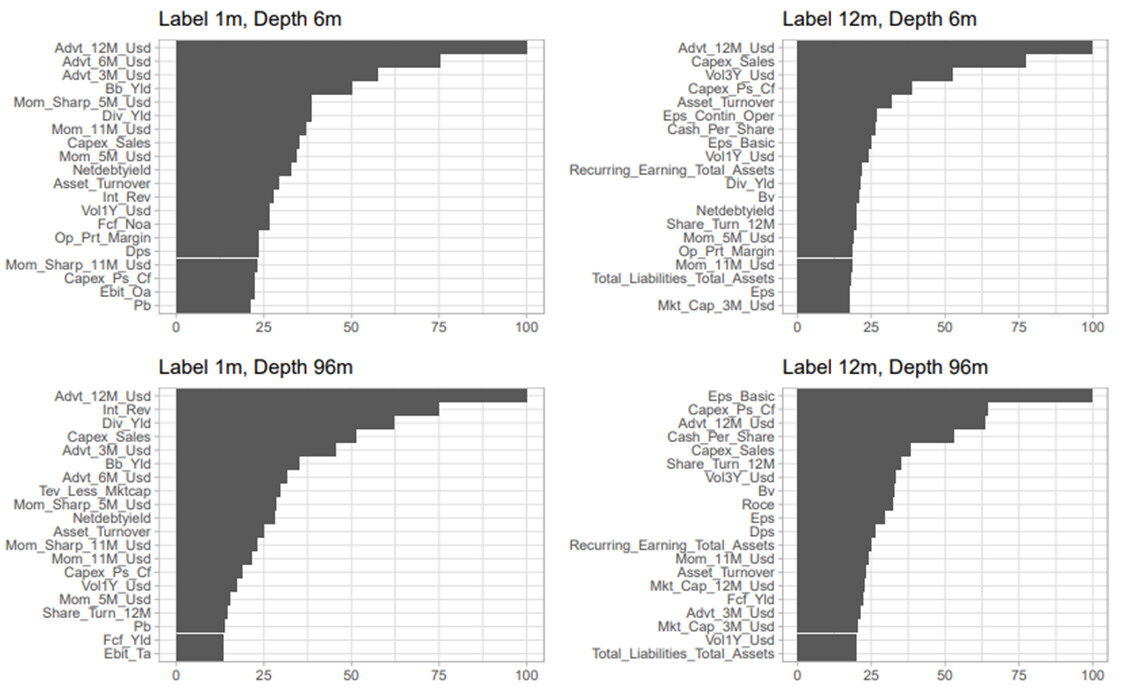

Liquidity and momentum matter in the short term while fundamentals are more prominent for long term returns.

My thoughts: Pick your investments with long term fundamentals, enter and exit on momentum.