Jim, the agreement with Marc is not to show any backtests with market timing. I am not aware that all postings of simulations is prohibited.

That would not make any sense.

As to the 500 stock Port, the question that should be asked is: where does the universe come from?

As I said before there are lots of good tools on P123, and we do not need AI to design good models.

The question was the one Korr123 put forth. Whether some overfitted backtest proves anything.

I agree with Korr123 that the Designer Models are a better indication and that the backtest proves nothing.

Marc has also—correctly in my opinion—made the point that a single overfitted backtest proves nothing.

You now think a backtest—without the AIC that you have recommended in the past—proves much?

Do you not think Designer Models are a better indication?

Whatever your final agreement with Marc, that started with Florian commenting on your over-reliance on backtests. As if they prove anything. I think Florian, Marc, Marco, James and Korr123 all have a point.

Georg, can you share with us again the stats you did on the Designer Models? That is even with survivorship bias isn’t it?

The p-value was something like 10^ -17 wasn’t it? Oh wait. There is that last backtest you showed us. Never mind.

Yeah. Here it is:

Could be just me but it will take more than one backtest to say Korr123 does not have a point. That is a pretty big t-stat you calculated.

The biggest I have ever seen in any serious financial post or publication actually.

Yeah. Korr 123 has a point. The point you so clearly made already.

Aside from my gripe about these forms devolving again, someone stated it well. We will never be able to compete with the likes of he Medallion fund. It won’t happen. Other funds have even tried to replicate their success and failed miserably with much more in financial, human intellect/time, and data wherewithal. If anybody on here has a PHD is mathematics along with several PHDs in mathematics and you have tens of millions of dollars and every data field available then maybe you can compete. Plus most of us can’t access several multiples of leverage. Strategies are not dead on this site. There are out-performers, but we will never be able to compete at the same game Medallion is playing. They make millions of trades a year some held for seconds or minutes at a time. We can still outperform playing a different game in spaces where only retail investors can go.

I will leave it with this. There is value to users revealing back tests. Any common sense person knows that back tests are simply proving grounds for ideas and may, or may not, pan out in real time.

Letting the forum view the back tests, and logic behind them, can spur ideas that may not have been considered. I have commented that there should be a forum open only to subscribers where back tests can be freely revealed so that the trial subscribers don’t get jaded by the fortune telling.

As to your posts Jim, they are rather antagonistic and not very helpful. You seem like a bright guy, so contribute.

Put up some models and lets see what you’ve got. Maybe you can teach us something, but proof is in the Alpha. Not the rhetoric.

Peace. I leave Marc and Marco to make any further comments about backtests.

But I hope people noticed that no one in this thread has asked to have anything turned off as far as features here at P123.

We all know now not to make any feature requests. No one did that either.

If James, Korr123 or I like statistics that should be fine with everyone.

In the last week the only one who has posted any specific statistical methods has Yuval in another thread.

[b]I reserve the right to want to use some of the same methods as Yuval does. Bootstrappping and a method similar to his correlations for example. I call what I do validation. Whatever Yuval calls what he does I generally like it.

FURTHERMORE, I THINK THIS IS A SPECIFIC CAUSE FOR MUCH OF THE SUCCESS OF HIS DESIGNER MODELS.[/b] At least relative to some of my models in this market anyway.

I get that only Yuval is allowed to talk about these ideas. And again no feature requests were made and no one asked to turn off any of the methods you use.

In this thread I defended Korr123 who has posted 9 times in the past. He has met some of the people at the Medallion Fund and I think we could have been more receptive to some of his ideas.

Especially, since I did not hear him wanting to restrict any of your ideas or methods.

Personally, I would like to hear some more from him.

Agreed. Instead of getting all worked up that we’re not doing what RT are doing, I’m thankful for it. Any retail investor or small shop attempting high turnover or high frequency strategy is more likely to be the prey than the predator. I’ve also heard it speculated that RT have locked up exclusive use 100 year leases with their proprietary dataset providers. Trying to play their game is futile at best. If it was all some sort of mathematical or machine learning “special sauce”, someone else would have replicated it by now.

Is everyone sure that D.E. Shaw & Co. is losing money?

On a smaller scale I just helped someone develop a Deep Learning Model for his personal investments. He sells software already for making investments.

The Deep Learning program worked. But ultimately he stuck with what he new: his own program.

The program he sells and the one he decided to use for his personal investments automated something similar what Yuval does with spreadsheets now. This was his own program and I did nothing to help develop this.

He had no complaints about how his program performed and decided to use it himself.

So not as sophisticated as what we are talking about with D.E. Shaw & Co. but someone that contacted me through a mutual friend is doing something a little more advanced than we are.

Personally, I do not think any of this is rare or without success.

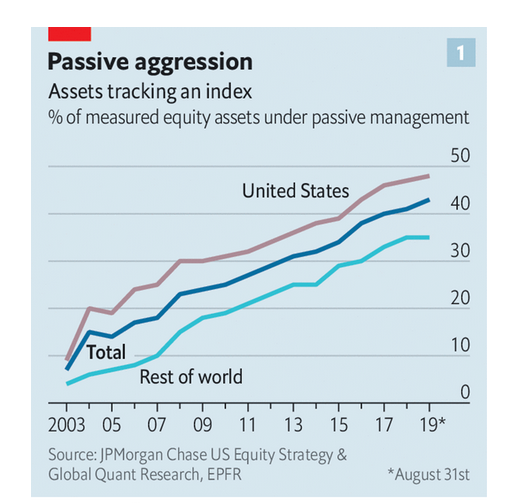

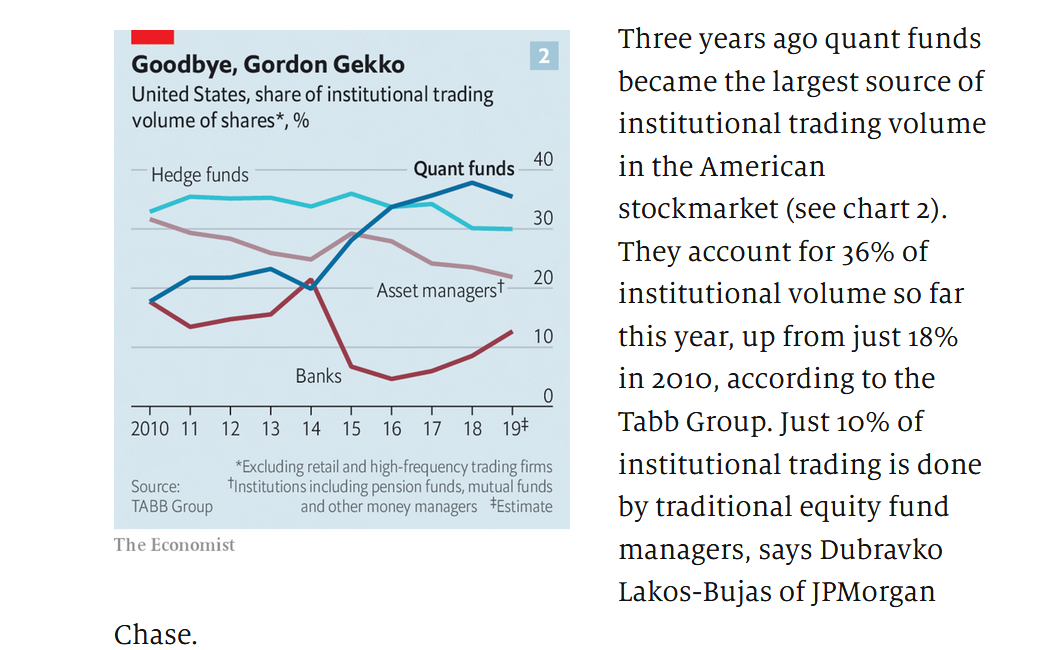

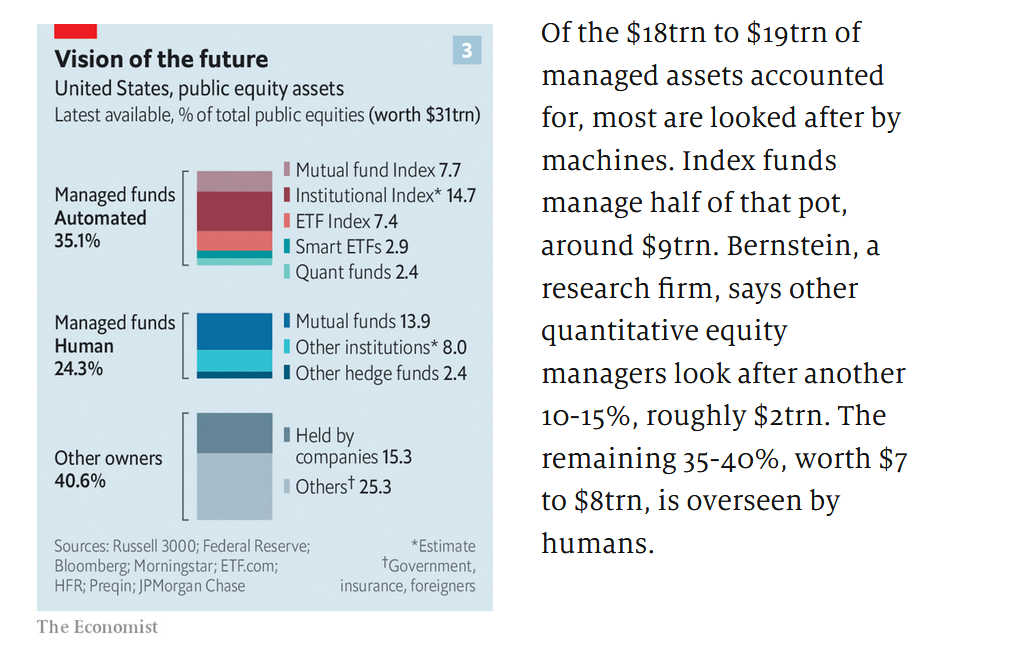

I don’t think there is a choice for retail investors as “The stockmarket is now run by computers, algorithms and passive managers”. Attached are 3 images from this article from the Economist. If you want the full article, here is the link :

Four of the world’s five largest hedge funds —Bridgewater, AQR, Two Sigma and Renaissance—were founded specifically to use quantitative methods. The sole exception, Man Group, a British hedge fund, bought Numeric, a quantitative equity manager in 2014. More than half of Man Group’s assets under management are also now run quantitatively.

To answer Jim’s question, D.E. Shaw’s flagship hedge fund, the Composite Fund made about 11% last year. The returns were driven by gains in both the systematic and discretionary investment strategies. The $14 billion Composite fund, which invests across multiple strategies and closed to new investors (not accepting new money) since mid-2013 gained double-digits in seven of the past eight years. D.E. Shaw’s Orienteer platform did even better last year. The Orienteer platform’s HV variant gained 41.3% while the main Orienteer strategy gained 25.8%.

Everyone does know that the debate over preferences—whatever they may be–isn’t going to change P123’s plans over the short- to medium-term time horizon I hope. At least I do not think so:

I think it’s important to remember that there are many ways to skin a cat. There is no sole superior way to generate alpha. That’s why there have been several different successful investment philosophies throughout time. I love when an article states that “value” investing is dead or that “quantitative” or “machine learning” is the only way to invest because everybody is doing it. That in itself should give you pause. If everybody is doing it that way, then what percentage are actual making alpha? If everybody is trying to expose the same inefficiencies then those inefficiencies are likely to disappear very quickly and simultaneously expose the same players to a high level of risk because they are herding. It doesn’t matter whether it is traditional stock picking, quantitative screening, or machine learning. I do quantitative investing because I feel like it saves me a lot of grunt work. But one could (maybe not as easily) spend the time and comb through the statements and filings of companies by hand and achieve similar results. But that takes a tremendous amount of time and relies on a very level headed disposition on the part of the investor.

So if you were trying to reverse engineer this trade, I guess find an exceptionally crowded short position and get in when the price uptrend ramps up knowing that shorts are always the weakest hand. Pretty common sense stuff, but difficult to time in the real world (which is what RT makes RT, I guess).

Exactly. It is a complex adaptive system. Also, I struggle to see that in the really long term - good old fashioned business analysis - will go out of style. They are not Rentech, but there are a lot of low turnover fundamental shops who beat the S&P. Akre, fundsmith, etc. come to mind.

I think our time is better served on this platform trying to codify their philosophy.

I comment only because Peace may be directed toward me.

I have said before Ray Dalio is one of my heroes and I have at least thought he was largely discretionary. I may be wrong about Ray Dalio but Fundamental Analysis works, IMHO.

Maybe his use of correlations and use of macro information is more complicated, perhaps. He probably employs some quants but I would not put him into the machine learning category anyway.

And if a may, I think the plans for P123 are baked into the cake. I have no reason to sell a particular technique to anyone anymore.