Dear all,

It is not always easier to make money running a long/short book than a long only portfolio.

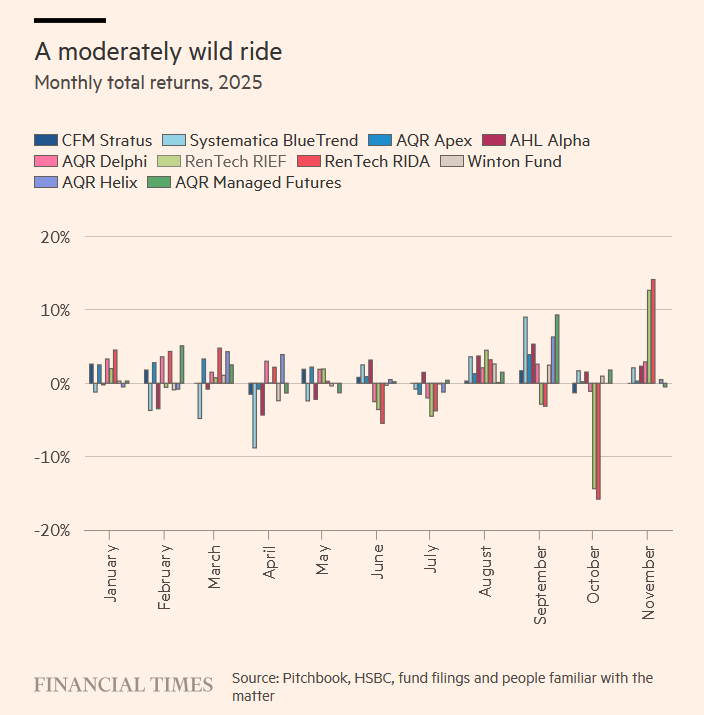

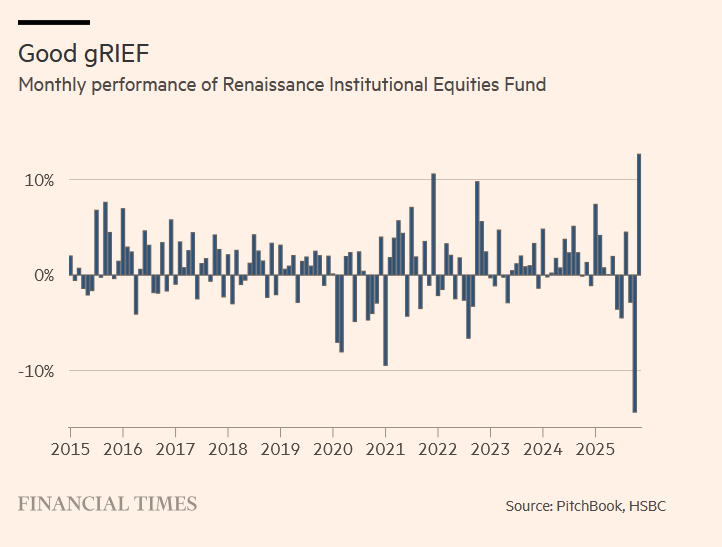

The record losses for quant hedge funds goes to Renaissance Technologies in Oct. With all their AI/ML expertise and factor investing, Renaissance Technologies lost all profits made in the whole year from their Oct losses for both external funds, RIDA and RIEF. They have crawled back some of the losses in Nov with YTD gains about zero.

Pls check out the article below from Bloomberg.

Regards

James

Fast-Money Quants Stumble as Momentum Bust Roils Strategies

By Justina Lee and Denitsa Tsekova

October 25, 2025 at 4:11 AM GMT+8

Takeaways by Bloomberg AIHide

-

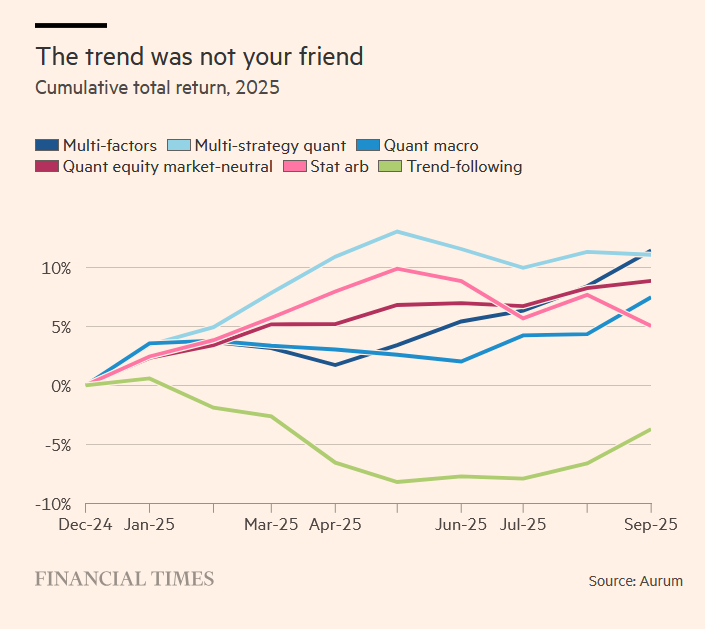

Quantitative funds are suffering this month amid reversals in crowded and previously money-minting positions, with quant long-short funds down 1.7% in October.

-

The momentum unwind has tripped up investors who have been riding on the profitable coattails of steady winners like AI and European banking shares, as well as assets like gold.

-

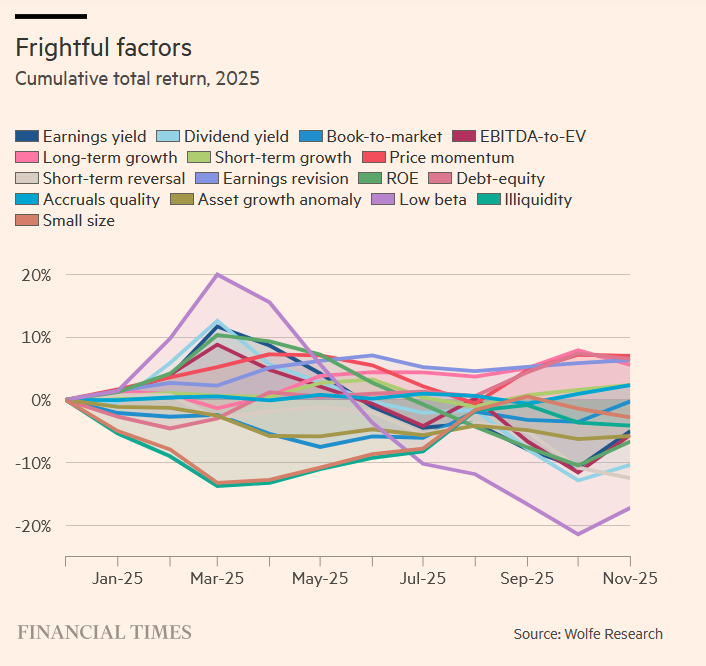

Strategies tuned to the “quality” factor and the “low volatility” factor also lost money as expectations for central-bank easing bolstered risk appetites and lifted firms with flimsier fundamentals.

Behind the scenes of placid Wall Street markets, drama is unfolding for some heavy-hitting professional investors.

Quantitative funds are suffering this month amid reversals in crowded and previously money-minting positions. The risks in stretched momentum trades were laid bare this week in sessions like Wednesday, when high-flying gold, tech shares and crypto were torpedoed all at once.

Quant long-short funds are down 1.7% in October, posting their first losses since another big bout of volatility in July, according to a Thursday report from Goldman Sachs’s prime brokerage. That compares with roughly flat returns for their fundamental peers. The $20 billion Renaissance Institutional Equities Fund lost about 15% through Oct. 10, Hedge Fund Alert reported. A representative of the firm declined to comment.

For now, the pain is confined to institutional investors employing long-short strategies. Broad equity benchmarks ended the week solidly green, with the S&P 500 rising 1.9% and the Nasdaq 100 adding 2.2%. Bitcoin was around $110,000, way below its recent peak, while gold staged a modest bounce after losing more than 5% Tuesday.

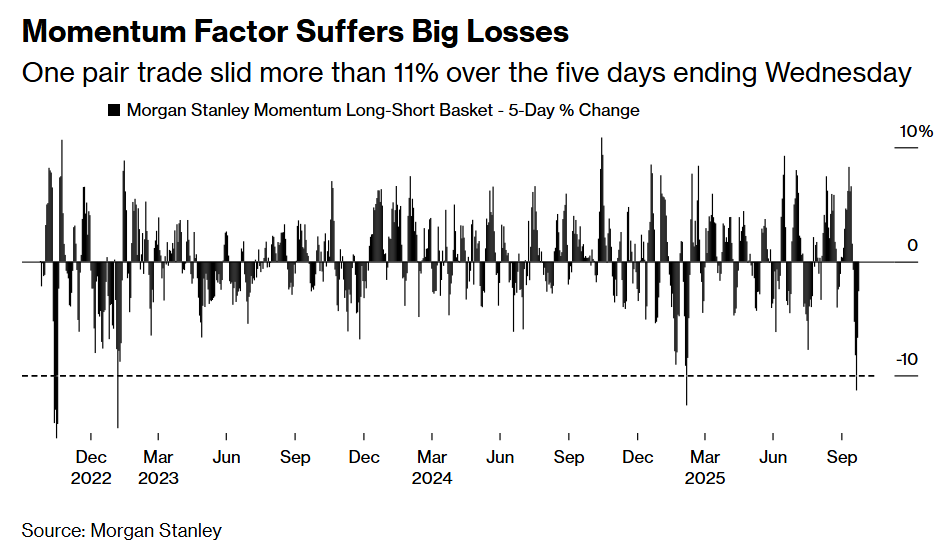

Stripping out the quant-speak, the momentum unwind essentially translates to a stalling out in steady winners like AI and European banking shares, as well as assets like gold, tripping up anyone who has been riding on their profitable coattails. In one brutal example, a long-short Morgan Stanley basket tracking momentum stocks slid 11.3% over the five days ending Wednesday, the sharpest decline since March.

At the same time, strategies tuned to the relatively stodgy “quality” factor — profitable companies with low leverage, mainly — and the “low volatility” factor also lost money as expectations for central-bank easing bolstered risk appetites and lifted firms with flimsier fundamentals.

“‘Junk rallies’ hurt quants because they are often short low-quality stocks and long high-quality stocks,” said Richard Craib, founder of Numerai, a crowdsourced systematic hedge fund that runs about $450 million. “If the damage gets big enough, quant funds start to delever to cover their shorts, making matters worse and leading to a deleveraging cascade.”

Momentum Factor Suffers Big Losses

One pair trade slid more than 11% over the five days ending Wednesday

All told, the declines bear some similarities to the summer, when a junk rally derailed what had been a favorable year for quants. A notably wilder ride for speculative favorites has been a distinguishing feature of the latest drawdown.

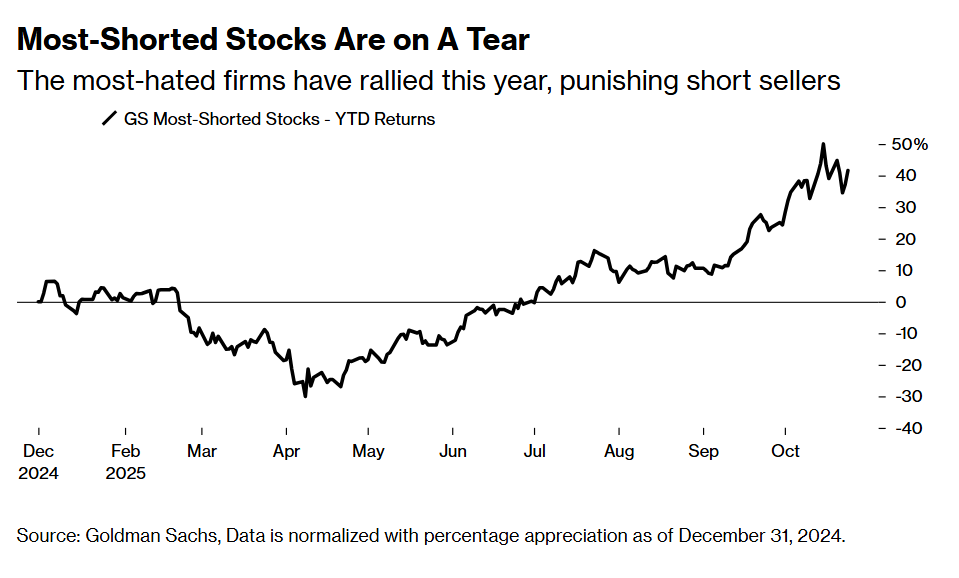

A Goldman basket of the market’s most-shorted stocks saw its October month-to-date gains reach 21% at one point — likely hurting hedge funds — only to nearly halve that by Friday. The highly-shorted Beyond Meat Inc. surged 146% Tuesday on an influx of retail traders before plummeting. Gold posted its worst day since 2020 on profit-taking.

The rollercoaster route that saw some speculative names gaining in early October only to sell off recently has the “makings of another quant quake,” Charlie McElligott, managing director of cross-asset strategy at Nomura, wrote in a note.

“It feels like there is an increased sensitivity of macroeconomic variables and single stocks to reversals at the moment — we saw it with gold and oil,” said Adam Singleton, chief investment officer of external alpha at Man Group. “There’s a little bit of trying to find a narrative around the macro situation right now.”

Most-Shorted Stocks Are on A Tear

The most-hated firms have rallied this year, punishing short sellers

In stocks, the abrupt rotation has been most evident in the momentum strategy, which goes long shares with large recent gains and shorts the opposite. The momentum drawdown may continue as hedge funds continue to trim their historically elevated exposures to the factor, Ioannis Blekos, an equity salesperson at Goldman, noted this week.

Quant hedge funds deploy a wide range of trading signals, many of which can be proprietary. But generally, their October weakness may be explained by big losses in investing styles common to many of them, says Yin Luo, who leads quant coverage at Wolfe Research.

In addition to momentum, value (which favors cheaper shares), quality (profitable and low-leverage ones) and low volatility are all down this month.

These factor declines mean “institutional investors have to rush to cut down risk budgets from time to time — all that timing difference is likely to trigger rounds of further risk-on and risk-off trades,” he wrote in an email. “In short, the self-fulfilling prophecy makes it even worse.”

At Jupiter Asset Management, the $6.3 billion Jupiter Merian Global Equity Absolute Return Fund is down about 1.9% this month, set for its worst period since 2020, trimming its 2025 gain to 8.4%. Its manager, Amadeo Alentorn, attributes the broad quant weakness to a junk rally and short squeeze in the US and momentum declines in Europe.

“It’s not one single kind of driver that’s driving everything in different regions, in different sectors,” he said. “This is why maybe you are seeing quite a bit of dispersion within the managers.”

While many quants rely on idiosyncratic signals that strip out the widely known return drivers, there can still be collateral damage as common factors start selling off, said Singleton at Man. Even then, the declines this month, as in July, are a bit of a mystery.

“It’s starting to get a little bit troubling that managers can have, in some of the more well-publicized cases, quite bad months without there being such an obvious driver of why they’re losing money,” he said.

- — With assistance from Isabelle Lee