Hello everyone,

I took advantage of the trial period to create and optimize a simple strategy that seems to perform quite well so far.

This is my first time investing in this way, so I’d like to avoid beginner mistakes as much as possible.

That’s why I’d really appreciate hearing the opinions of the more experienced members here ![]()

I have €60,000 to invest in a tax-advantaged account (I’m from France).

My plan is to invest €40,000 as soon as possible, then €20,000 in a year, to reduce the risk of investing at a market peak. Given the strong growth in recent years, I’m afraid it might not last forever—but I also don’t want to wait indefinitely before getting started.

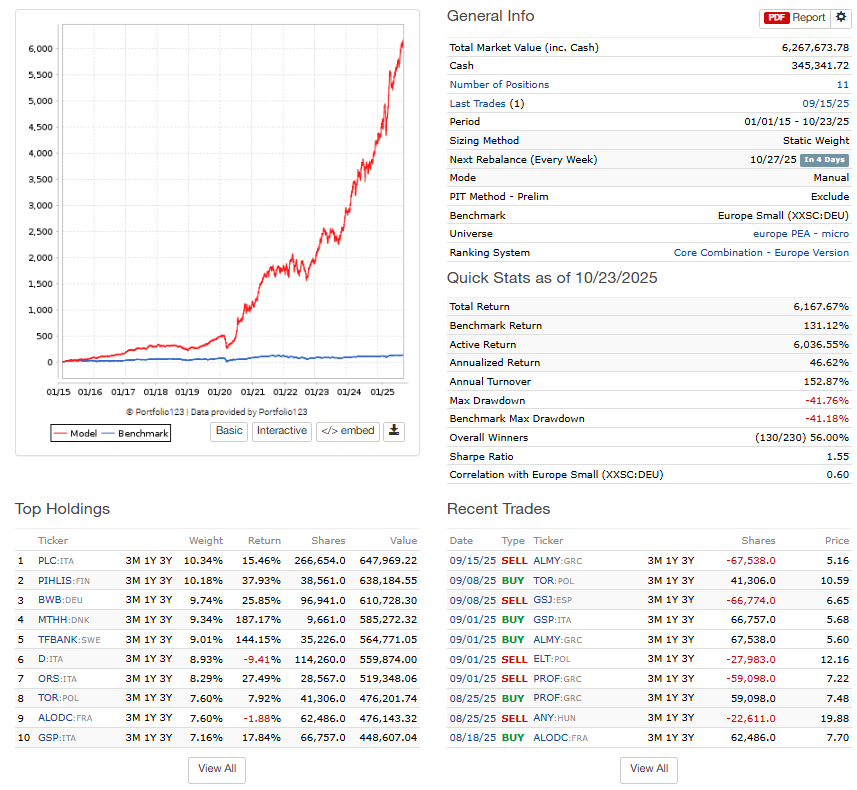

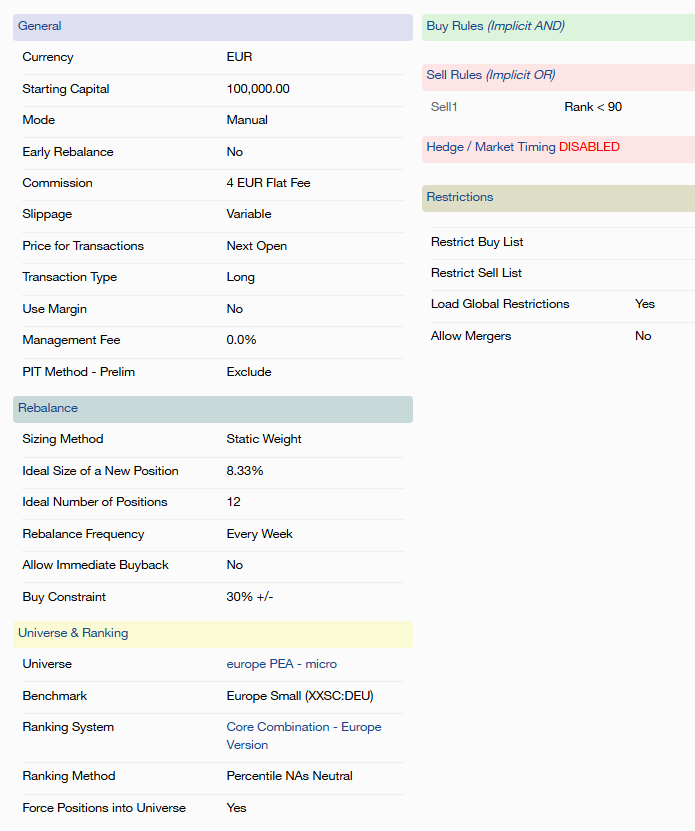

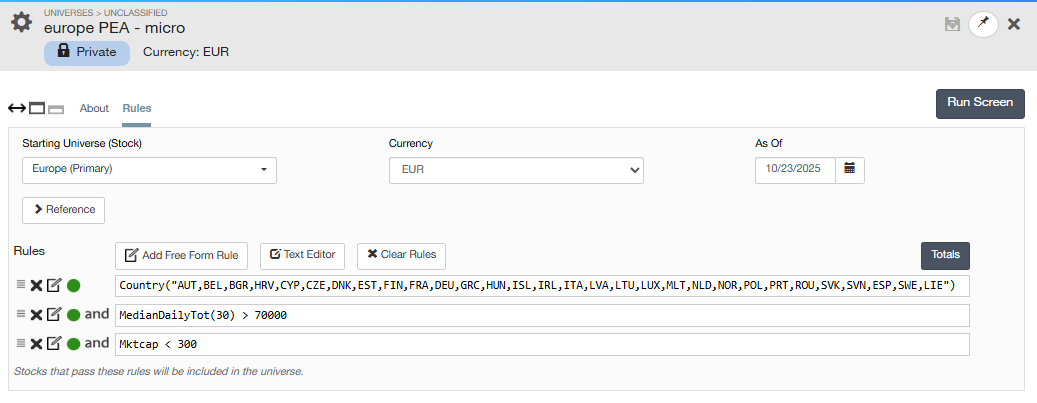

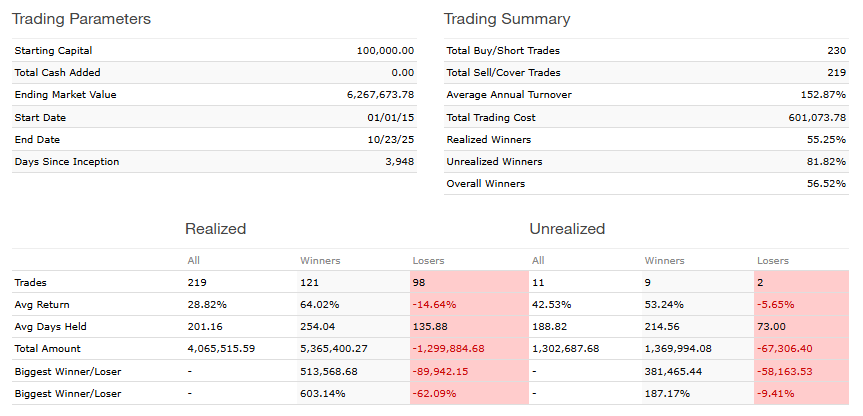

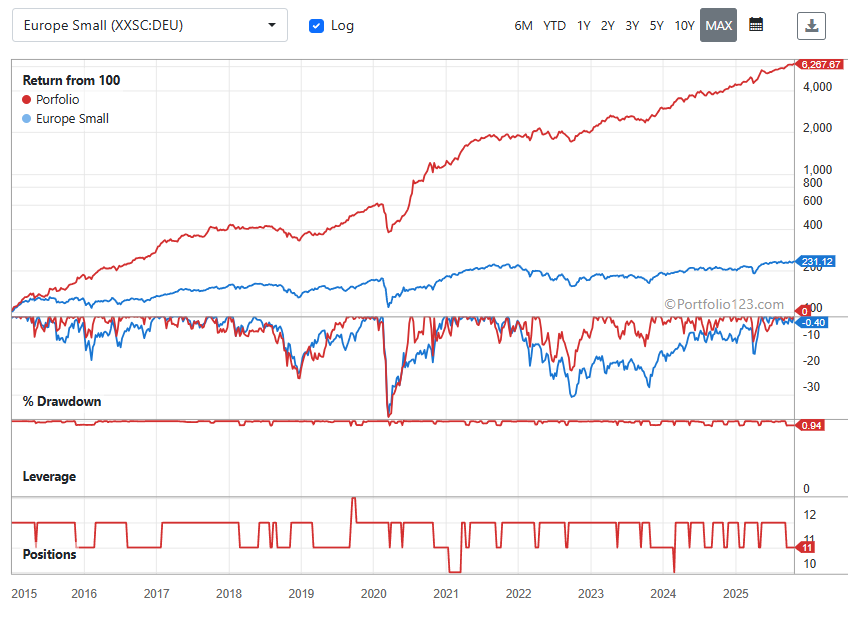

I’ve adjusted the strategy parameters several times to optimize the CAGR (in particular : Ideal Number of Positions, Rebalance Frequency, my single Sell Rule, and the Universe Rules), and I’m wondering if I might have over-optimized the strategy to the point where it’s now unrealistic.

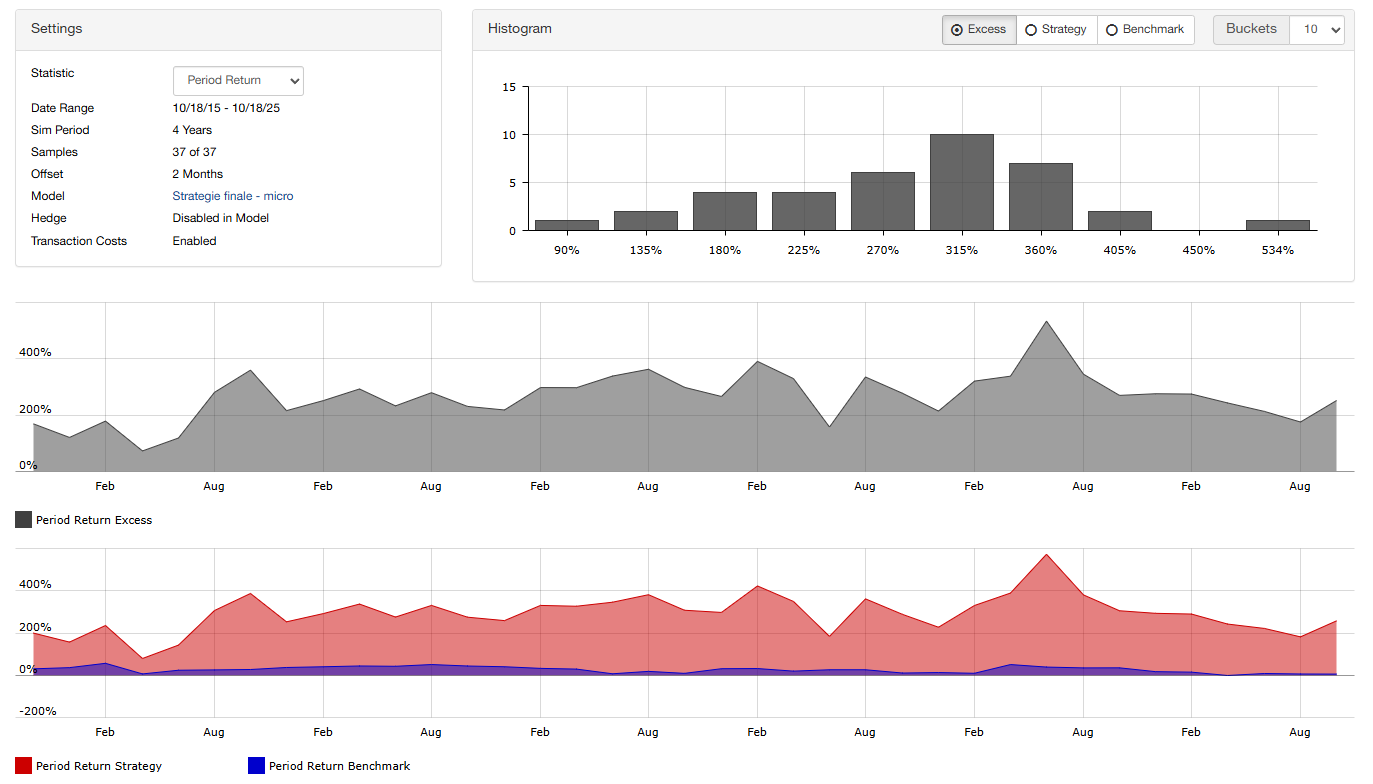

Is the rolling test sufficient to confirm the credibility of a strategy?

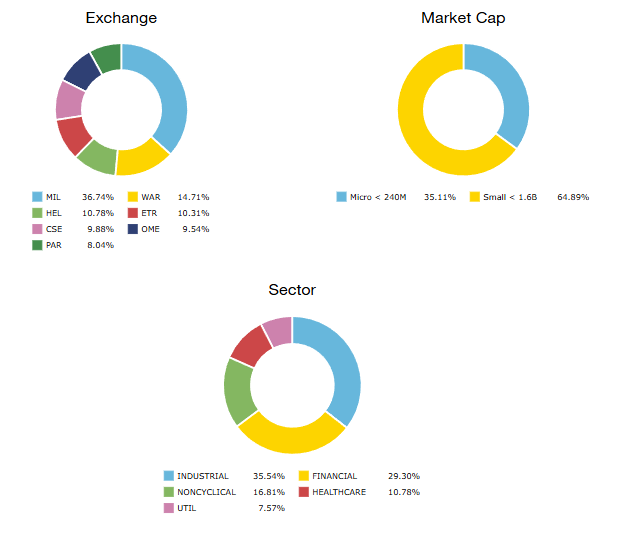

The strategy mainly invests in small caps and micro caps, since that’s what has shown the best returns in my tests.

Also, I used the “Core Combination – Europe Version” Ranking System without modifying it, as I don’t feel skilled enough to build a better one. What do you think about that choice?

Finally, I realize it’s a bit bold to invest in a portfolio of only 12 positions, but that’s what seems to deliver the highest CAGR, and I feel fairly comfortable with that level of concentration.

Please don’t hesitate to share doubts, critiques, or suggestions—that’s exactly why I’m posting this.

Thank you for the value you all bring here, especially the P123 team, and in particular Yuval, whose writings I’ve enjoyed reading.

Congratulations on creating such a powerful tool—P123 is exactly what I was looking for to put my ideas into action effectively.