@pitmaster reminded me about make_regression. It creates features for which you can control the number of informative (non-noise) features, correlation of the feature and the global amount of noise in the data.

I thought I would use it to answer questions like "How many noise factors can I add before ExtraTreesRegressor stops working?" I am not sure I can simulate stock data exactly but at least I know which are the noise factors and how may of them there are with make_regression as I can control that. That question was kind of interesting.

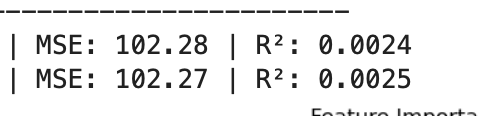

What was unexpected is that when I made more features informative the MSE increased (generally a bad thing)!!! While the R^2 increased (generally good). So contrary indicators with the MSE being suspect as it got worse when more features were informative.

MSE and R^2 for 2 models I was checking out with 10/50 informative features:

Now with 40/50 informative features:

So question:

-

Will MSE give you a false impression--at least when you are trying features? Honestly this is new and I am not sure how to interpret this. ChatGPT had some ideas but you can go to ChatGPT directly.

-

Is make_regression useful to us? And if so how.

I was comparing 2 models that Yuval and Pitmaster were recommending. Pretty much a tie (with these parameters) so maybe ignore that. If it was not a tie I probably would have modified the code to avoid getting sidetracked. I am just interested in the above questions.

import numpy as np

import matplotlib.pyplot as plt

from sklearn.datasets import make_regression

from sklearn.ensemble import ExtraTreesRegressor

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_squared_error, r2_score

# ----------------------------------------

# 1. Generate synthetic regression data

# ----------------------------------------

X, y, coef = make_regression(

n_samples=100_000, # scaled down for speed

n_features=50,

n_informative=40,

effective_rank=10, # adds correlation structure

noise=10.0,

coef=True,

random_state=0

)

# ----------------------------------------

# 2. Train/test split

# ----------------------------------------

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.2, random_state=1

)

# ----------------------------------------

# 3. Define Yuval's model

# ----------------------------------------

model_yuval = ExtraTreesRegressor(

n_estimators=100,

max_depth=8,

min_samples_split=2,

#min_samples_leaf=100,

max_features = 0.3,

random_state=42,

n_jobs=-1

)

# ----------------------------------------

# 4. Define Pitmaster's model

# ----------------------------------------

model_pitmaster = ExtraTreesRegressor(

n_estimators=100,

max_depth=None,

#min_samples_split=2,

min_samples_leaf=500,

max_features = 0.3,

random_state=42,

n_jobs=-1

)

# ----------------------------------------

# 5. Fit and evaluate Yuval's model

# ----------------------------------------

model_yuval.fit(X_train, y_train)

y_pred_yuval = model_yuval.predict(X_test)

mse_yuval = mean_squared_error(y_test, y_pred_yuval)

r2_yuval = r2_score(y_test, y_pred_yuval)

# ----------------------------------------

# 6. Fit and evaluate Pitmaster's model

# ----------------------------------------

model_pitmaster.fit(X_train, y_train)

y_pred_pitmaster = model_pitmaster.predict(X_test)

mse_pitmaster = mean_squared_error(y_test, y_pred_pitmaster)

r2_pitmaster = r2_score(y_test, y_pred_pitmaster)

# ----------------------------------------

# 7. Print comparison

# ----------------------------------------

print("Performance Comparison:")

print("-" * 40)

print(f"Yuval's Model | MSE: {mse_yuval:.2f} | R²: {r2_yuval:.4f}")

print(f"Pitmaster's Model | MSE: {mse_pitmaster:.2f} | R²: {r2_pitmaster:.4f}")

# ----------------------------------------

# 8. Optional: Plot feature importances

# ----------------------------------------

plt.figure(figsize=(12, 4))

plt.bar(range(50), model_pitmaster.feature_importances_, alpha=0.7, label='Pitmaster')

plt.bar(range(50), model_yuval.feature_importances_, alpha=0.7, label='Yuval')

plt.title("Feature Importances (Comparison)")

plt.xlabel("Feature Index")

plt.ylabel("Importance")

plt.legend()

plt.tight_layout()

plt.show()

# Show the true coefficients

print("True coefficients (non-zero features):")

for i, c in enumerate(coef):

if abs(c) > 1e-5:

print(f"Feature {i}: {c:.4f}")