I get the following message: Error in Weight Rule 'Weight': In $sma_scores: Ticker BNDX is not a Stock in GetRankPos()

Basically, I run a similated strategy and use a custom formula in the dynamic weighting formula. The custom formula checks the rank of one of the ETF tickers in the universe, or at least that is what I'm hoping to do.

The respective ETF is indeed in the universe I am using. Is it not possible to use GetRankPos in dynamic weight formulas? Is this only available for stocks and not ETFs? Or could something else be going on?

Wanted to give some additional info, perhaps then someone can help me out.

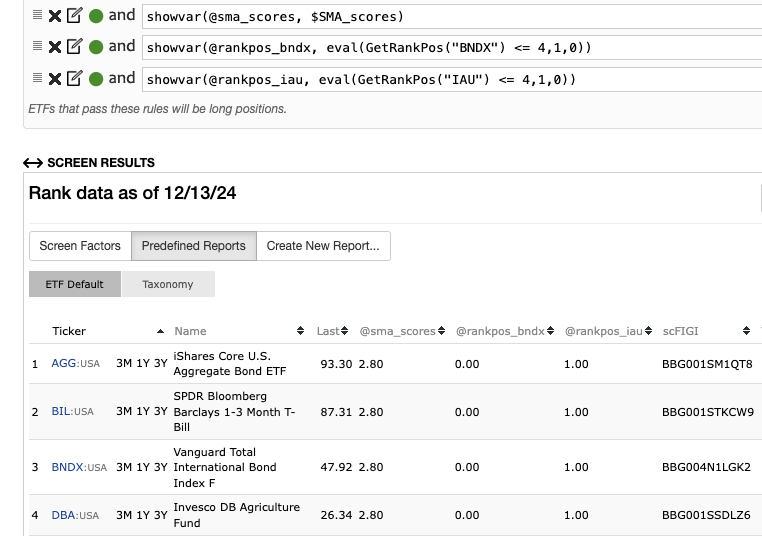

I use a formula named $sma_scores that has a term like this: eval(GetRankPos("BNDX") <= 4,1,0)

I can run that term in a screener on the same Universe and using the same ranking system as I use in my simulated strategy. If I do that, I get no errors (see below).

ETFs are supported with Dynamic Weights. Here is one example of a position weight formula for ETFs:

1ticker("iwf iyw xly xlk qqq smh soxx pnqi xbi onln xle xlu idu dvy sphd vymi dgrw iye efv dbc iym" ) +5 ticker("UUP ") +5* ticker("gld ")

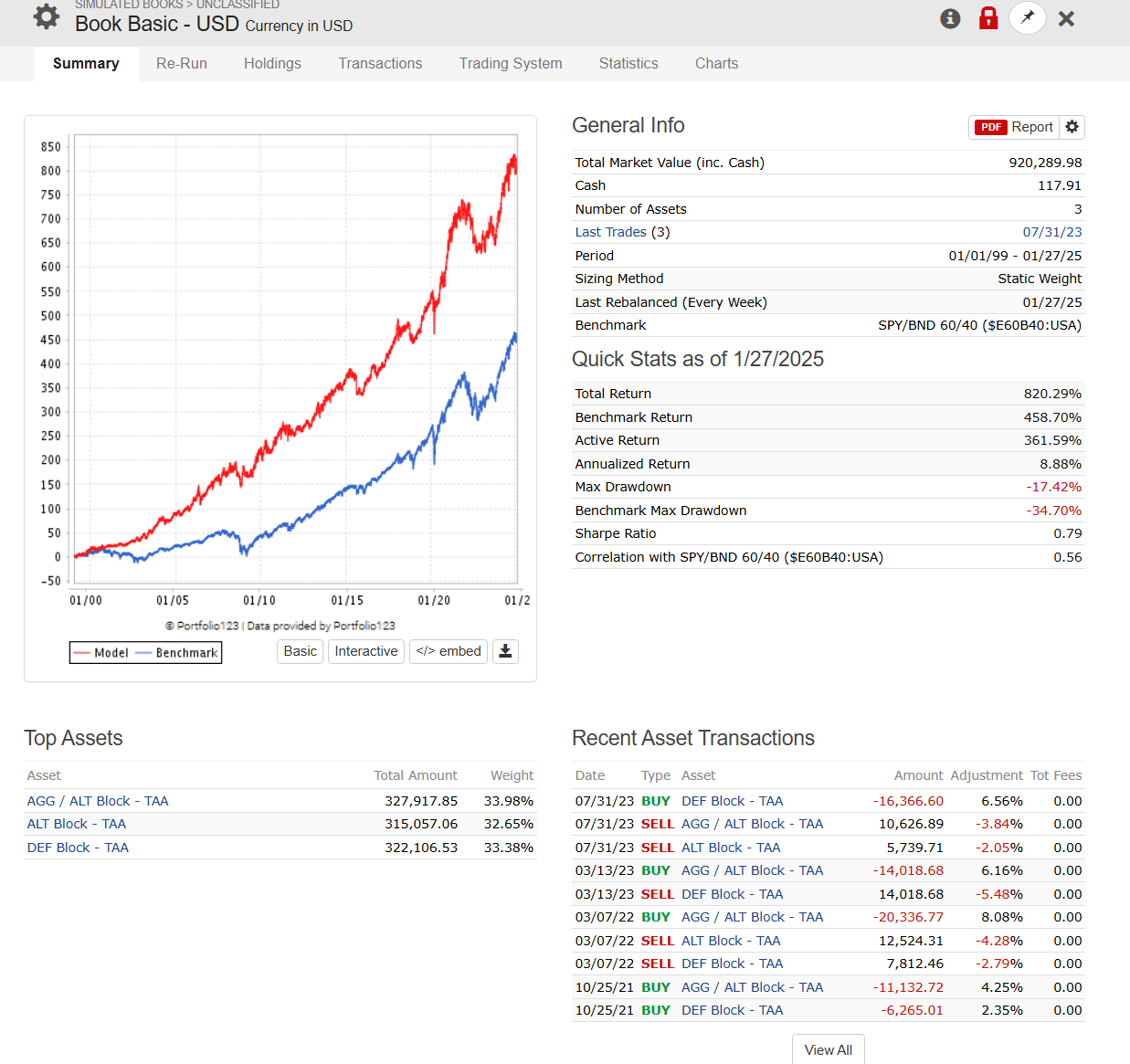

Because of this, I managed to create this strategy in Portfolio123: ETF strategy in Portfolio123 and do not have to use an other platform anymore that I 'had' to use before. Great!

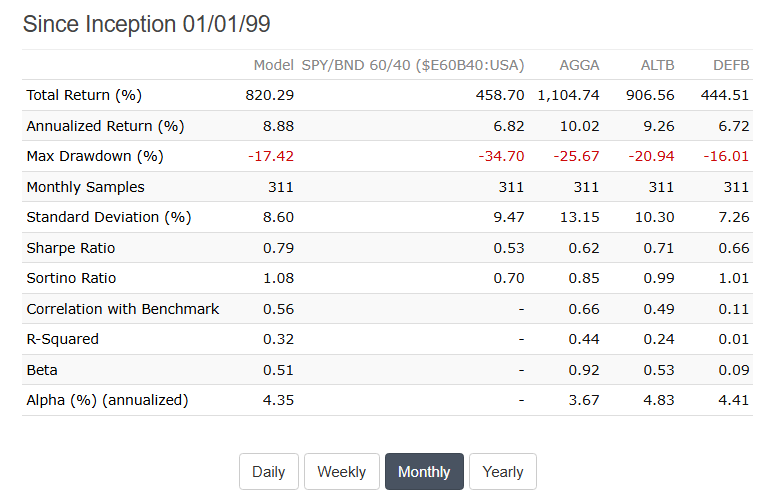

The results of that strategy are as below. My goal was to make something robust that has potential to outperform a 60/40 allocation without lagging too much when the US markets rip like they did in the last 15 years, using just price/return data.

The result is for the strategy I described earlier with one minor change. When the US dollar compared to other major currencies (UUP) is trending lower, it will allocate a portion of the 'risk-off' not only to US treasuries like IEF, SHY or BIL, but also to international bonds (BWX), gold (IAU) and commodities (DBC/DBA), depending on their relative standard deviation at such times.

Reason for the change was the article of Ray Dalio about a possible dollar devaluation in the future. In the case I would not make a change to the system as described and things would somewhat pan out as he describes somewhere in the future, than the strategy might hold more dollar exposure than I would like. Without the change, backtested results would have been similar though.

EDIT: wanted to note that for some ETF's, data is only available after the inception date of the strategy.