Thank You Whycoliffes. I use P123 and overweight the P123 models in my portfolio. I have confidence in P123 and none of this reflects any lack of belief in my P123 models at least.

But I have simplified my portfolio recently by using risk parity (equal contribution of risk). People can look at that on their own without my input and judge for for themselves.

I will say that Portfolio Visualizer goes beyond a backtest for some models and an allows for a true walk-forward cross-validation. To be clear, over-fitting is still possible with this method if you run it multiple times with different parameters.

Maximizing Sharpe ratio based on historical returns has the problem that the equations are too sensitive to any error in the returns portion. Your out-of-sample returns will be different no mater what. Even if due to a changing market. So maximizing Sharpe ratio tends not to work

I have considered shrinking the returns using Bayes to shrink the returns and maximizing the Sharpe Ratio with the Shrunken returns.

But it recently occurred to me that Black (of Black-Schoals fame) has already consider this approach a while ago with the Black-Litterman model.

Black-Litterman is considered a Bayesian approach and is probably more complete that what I would do. For example, it allows you to consider your confidence in your return estimates for a P123 model included the portfolio.

So, for example, if you are using several P123 models you could enter how much confidence you have in each model.

I do not have a lot of results to share. My only point would be: Wycliffes thank you for the article. I think there is value in it and I am already using the equal contribution of risk form of risk parity with an overweighting of my P123 models. I do believe P123’s models can work.

TL;DR; I am not sure about Black-Litterman but I want to learn more and this article helped some. Thanks.

BTW, it would need confirmation but ChatGPT 4.0 thinks a person could shrink recent returns using say PyMC (a Python library) and plug that into a Black-Litterman model. Essentially, making this a Hierarchical Bayesian model that incorporates what is happening recently in the market while using historical information about an asset.

For example, TLT might be doing weill now but you know what has happened recently will regress to the mean. This can be taken into acount by shrinking the recent returns (using PyMC). Black-Litterman would incorporate past history: e.g., TLT has had lower returns historically.

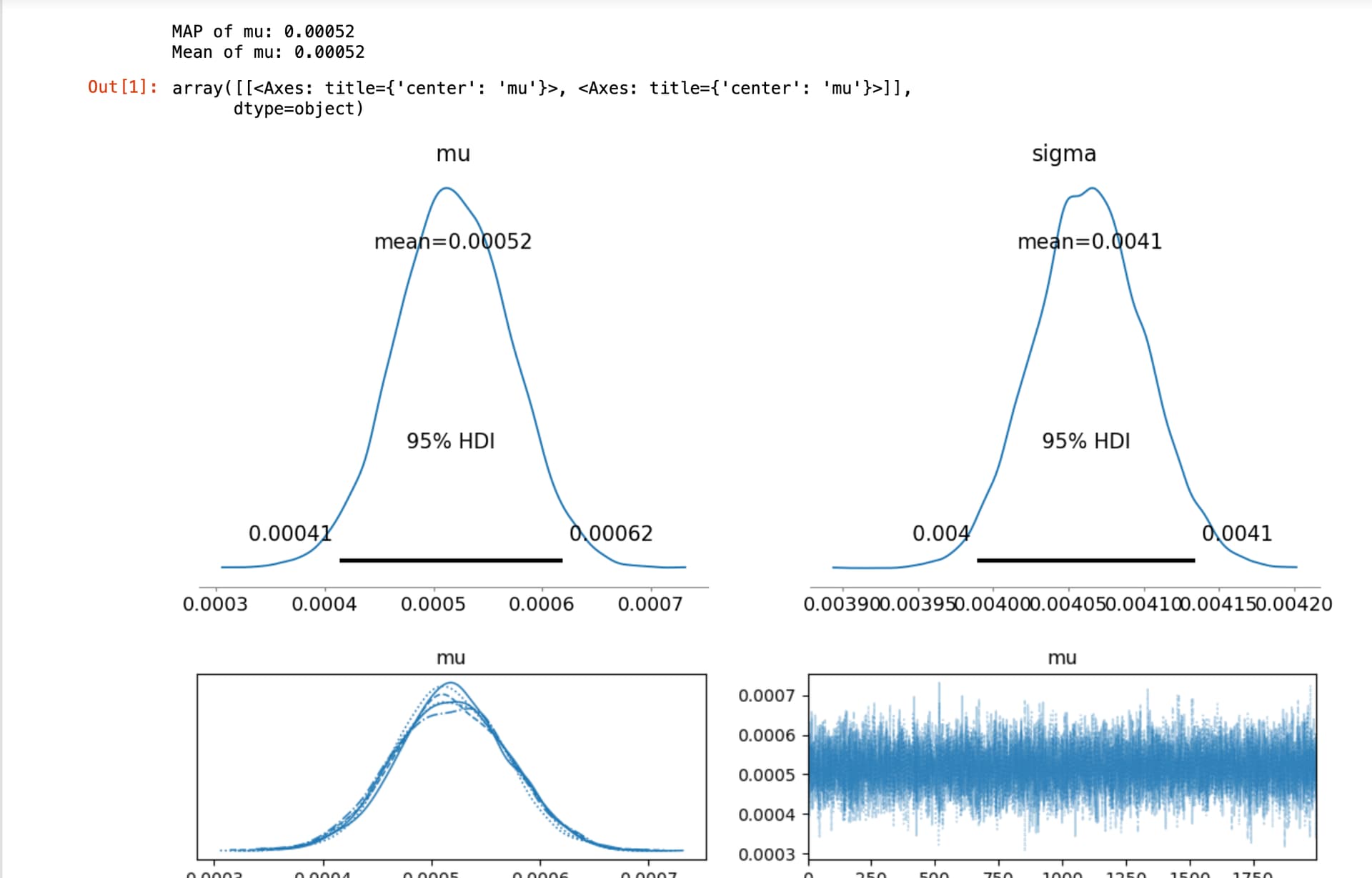

For those interested in this, here is an example of the posterior daily returns of an asset using empirical Bayes were the returns or a number of assets are used as the prior. You will want to use your own assets and no need to discuss the specific asset used here.

Some of this looks complex because it is. But you would end up just using the MAP output as your expect ed (shrunken) daily return once you figured out the code:

Jim