Can the community provide some guidance on how to make overlapping Entry/Exit signals function together? I hope to understand how to deal with this fundamental challenge I'm sure I'm not the first to face.

I have multiple composite risk control series that work well independently, but I'm getting bizarre in/out-of-market signals because the signals overlap. The details of my custom series don't matter, but they include breadth, volatility, advance/decline, and multiple other measures built into composites.

Rather than get mired in those details, I'll use simple examples for the signals to make this more straightforward. To demonstrate, I created a chart showing a basic exit signal when the S&P 500's 5-day EMA drops below the 200-day SMA and a simple re-entry signal when the EMA(5) moves back above the 100-day SMA.

The objective of different thresholds (200-day SMA on exit and 100-day SMA on re-entry) is to enable the portfolio to get back into the market earlier, nearer the start of a rally. If we used the same entry and exit signals (5-day EMA and 200-day SMA) on my example, there would be a two-month delay, remaining out of the market and missing the rally's start.

Here is a chart showing these signals on the S&P 500 before and during the 2008-2009 Financial Crisis. I'm using this period because, again, it simplifies the example.

The first chart shows an EXIT signal when the 5-day EMA (blue) drops below the 200-day SMA (red):

The second chart shows my simple example for RE-ENTRY when the 5-day EMA (blue) moves back above the 100-day SMA (green):

However, the EMA(5) would STILL be below the SMA(200), so the portfolio would exit the market again a week later!

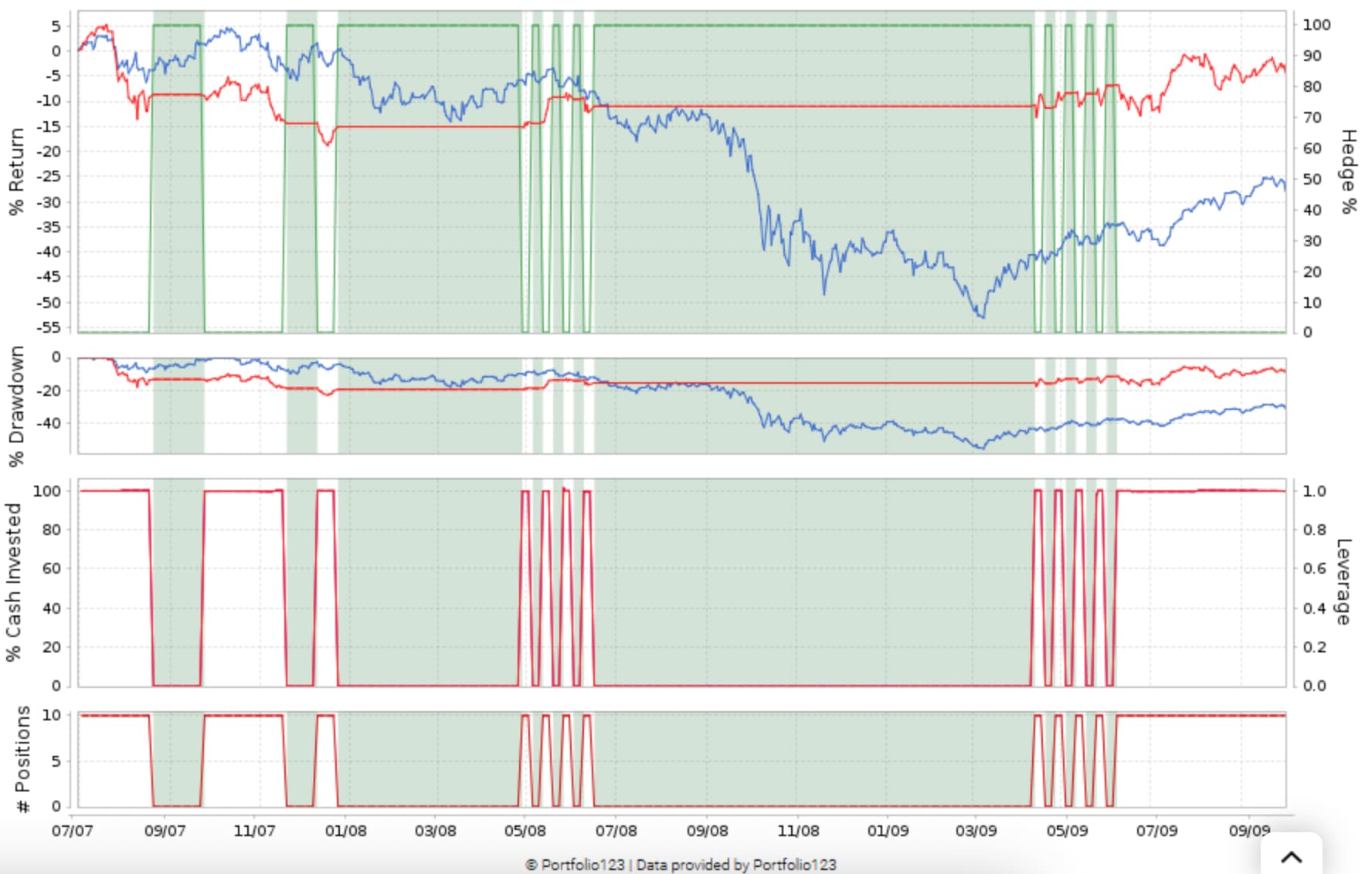

Here is the result when these signals are used in a simple portfolio's hedge rules from Mid-2007 to Mid-2008:

Obviously, this is not a desirable outcome with the weekly whipsaws in and out during the periods in April to June 2008 and 2009 when prices are above the 100-day SMA but below the 200-day EMA. Is there a way to resolve this quandary and make the strategy work as intended, or is this not possible?

Many thanks for any insights shared!

Chawasri