Paul, I always knew you had a great . . . uh, let’s skip the metaphor. FWIW, you’re spot on. GE and many other companies don’t report current assets and liabilities because it’s not relevant to them. These situation, and others like them, are not data holes. They are the inconvenient and statistically irritating but in fact inevitable reality that the corporate world is not a singular monolith in which all data-points are relevant for all companies. Much can be standardized, and Compustat does an amazing job of it. But sooner or later, we all run into areas where standardization can’t go.

Thus current asset/current liabilities thing came under discussion because somebody got tripped up trying to do a uniform analysis on the database. Think of how many years this oddity has been out there (as many year as financial results have been tabulated, audited and reported) and not discussed. Now, imagine all the other oddities out there that haven’t been discussed only because nobody has – yet – done a study or something like that which bumps into them.

If you tackle REITs or biotech, you’ll find oddities that are at least as poignant if not more so but harder to spot because conventional data exists – its just that the numbers don’t mean what you might think they mean. Media companies are often like that too. Tech is a whole different class because the accounting rules that force companies to charge all of R&D against earnings in the period in which they were expended as opposed to allowing them to do what other companies do with less human but similarly future-growth-seeking expenditures (depreciate them over the expected life of the asset).

It’s important, if you aren’t well versed in financial statements and fundamental analysis, to manage your expectations.

P123 users have seen again and again and again and again that they can succeed using the tools and ideas we offer even without getting into the weeds of financial/fundamental analysis. But for that to happen, you’ll have to ease up and allow it to happen; i.e., refrain from approaching p123, the data and the tools with expectations of precision and uniformity you might import from other disciplines.

The following from British logician Craveth Reade sums it up: “It is better to be vaguely right than exactly wrong.” Or to paraphrase one of Paul’s former professors, Aswath Damodaran, Don’t got bogged down trying to be right (as if anyone ever could be). The goal is to be a bit less wrong then everyone else.

This said, I also think we need a better tool to have a look at the data before starting to plug in variables into formulas. Otherwise, we might get unexpected results which might look vaguely right on backtest but will fail at some point when using live money.

We can do it on the screener but it is very cumbersome.

I think this is what “Data Views” was intended for. But right now, it is not very helpful.

A helpful first fix which would still be a step change would be to allow us to select custom universes in data views (see screenshot attached).

Could Aaron maybe chip in to let us know how easy or not it is to implement?

I think that plussing up the single company views is he best way to tease out the nuances between “as reported” values and Compustat “normalized” values.

Plussed up financial statements, with all articulating items shown, with option for displaying different time periods and normalizations (e.g., TTM) over custom rolling time windows, are the easiest and best way to satisfy our information requirements.

The ability to look at this data cross-sectionally is not going answer your questions about the nuances, IMHO.

Plussed up statements shouldn’t be a lot of work for P123 since the bones are already built in the panels tool.

Please make this happen.

…

For those who are not familiar with concept, CompuStat should be using an articulating financial statement balancing model to ensure the primary financial statement line items aggregate properly. While Capital IQ analysts make exceptions to Compustat’s original rules, the normalization priced does a fairly good job at standardizing different reporting paradigms.

It would require a revision (and likely a very costly revision) to our data license. P123 is an investment modeling platform and whatever display we do is tangential to it.

What you seek is a full-blown financial data reference capability. Firstly, that is not our business model. Secondly, if it were, we would not use Compustat but would have instead prefer the Capital IQ offering (see data white paper in Help area). And thirdly, the chances of our expanding into the data reference area are slim to nil since it has not proven to be an attractive business for third-party providers; the only providers I know of who do it well are the data vendors themselves, who own the data and sell subscriptions to their own platforms. As to third party providers, there’s a severe mismatch between the costs associated with licensing, developing and maintaining versus potential for monetization via advertising (not even close) or subscriptions (not enough demand at the price it would take to do it properly).

I understand your desire for it. But there are times in the life of every business when it has to simply decline a request.

I also understand, from your profile, that you hope to launch an equity fund in the future. If you go down that route, you may want to consider subscribing to the Capital IQ platform (which is, actually, quite good), and take an entitlement to Compustat data with the full reconciliations you seek and/or Capital IQ data.

I didn’t anticipate that expanding the financial statements views by several line items would’ve resulted in an issue with your data vendors.

I’m sorry to hear that this is the case.

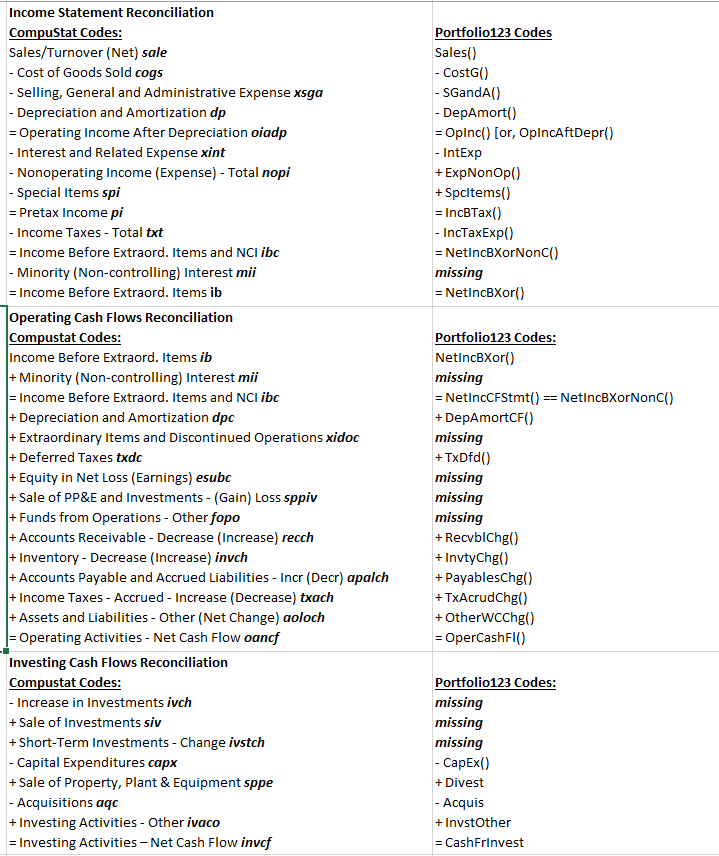

In case you decide to revisit this, I am attaching a snippet of an analysis that may helpf reconcile P123’s holding versus the Compustat’s articulating line items. In an ideal world, there would be a financial statement view to break out as many of these as possible. I don’t think anyone is asking for the supplemental data points, metadata, and footnotes that are included with a Capital IQ license. Note, that there are differences between quarterly and annual line items that affect this reconciliation.

I knew exactly what you are talking about. As noted, this is not part of our business model and not even in our radar for expansion. So it will not happen on Portfolio123.

That said, it’s clear that it is important to you. It may, therefore, be a good idea for you to look into the Capital IQ platform with a view toward subscribing. When I first mentioned it, I did so in the context of your indication, on your profile, that you may want to, in essence, become an institutional investor (that’s what funds are). And that is Capital IQ’s target market. But on reflection, I believe they are not strict about this; it strikes me as more likely an informal thing that arose out of an assumption that individuals would not want or play for the service. But if you want and are willing to pay, I expect they will work with you.

Also, as I recall, there were others who also expressed interest in this. Perhaps if there are multiple potential potential Capital IQ subscribers, a better subscription price might be negotiated. (From dealing with data vendors, it is our understanding that there is no formal price schedule – at least not a schedule that’;s shared with the outside word – and that everything is negotiable).

Let me know if this is something you (you, the singular user, or you, a plural group of users) would like to investigate further.

I am up to try getting a better price. The amount I was initially quoted for Capital IQ license was too high, but I would think again if I could I leverage collective bargaining power to reduce the asking price by one-half.

David, would you share the CapitalIQ quote? I’m not in the market now, but may be in a year or two. If you want to move the discussion off the forums, I could setup a private group.

Thanks,

Walter

I’m glad I found this older thread, as I have some similar questions on how total liabilities is calculated.

According to the balance sheet output on the “panels” screen, the formula for total liabilities appears to be:

total liabilities = current liabilities + LT debt + other liabilities

The first two factors are available in P123, however I cannot find a factor for “other liabilities” (only other non-current liabilities).

Take BIO as an example, according to the panel data, “other liabilities” makes up over 75% of total liabilities (3,231 / 4,109) , so it would be helpful to understand what it consists of.

Total liabilities = current liabilities plus non-current liabilities. Non-current liabilities = long-term debt plus provisions for risk and charges plus deferred tax liabilities plus other (non-current) liabilities. However, for banks and REITs you add total debt and total deposits to the last three items, and for insurance companies you add total insurance reserves and total debt to the last three items; these companies do not have “current liabilities,” so that’s what you use instead. While we report long-term debt and other non-current liabilities, we do not report provisions for risk and charges or deferred tax liabilites or total insurance reserves or total deposits.

I hope this helps, but please ask other questions if not.

Thanks Yuval, this clarifies, but unfortunate we can’t see the other lines. No worries, for what I’m after this should do.

A similar type breakdown seems to exist for the Total Assets. Again, referring to the stock panels balance sheet, total assets appears to be:

Total assets = current assets + non-current assets (net plant + intangibles + other non-current assets)

This lines up within +/- 5% for 230 stocks of the 400 non-financial stocks in the S&P500. For some outliers the difference in the reported total assets and the formula above is off by a factor of 1.5-3x or more.

Can you let me know what else is included in the Total Assets factor?

Total assets for companies outside the financial sector consist of total current assets + long-term notes receivable + total investments and advances + property, plant and equipment + other assets (including intangibles) + deferred tax assets. As you know, we do not have line items for some of these.

For stocks in the financial sector, it’s very complicated, to say the least.

Thanks Yuval, I was curious how the actual formula for total assets worked in P123, as it looks like many of these items are not available as line items. I’ll make it work.