Thanks @nzbryant . Please DM me and we can certainly discuss.

Cheers,

Ryan

Thanks @nzbryant . Please DM me and we can certainly discuss.

Cheers,

Ryan

I ran 3 portfolios:

Short Term 1: +44.93%

Short Term 2: +5.41%

1-Yr Hold: +25.26%

The crazy part of the performance is Short Term 1 and Short Term 2 are essentially the same systems with a couple of small differences. They both hold 15 positions. Short Term 1 sells if the rank is greater than 30, and Short Term 2 sells if the rank is grater than 60. The only other difference is the first re-balances on Tuesdays and the second re balances on Thursdays. Kind of wild that there is that much dispersion in returns.

Two live USA portfolios with the following returns according to Portfolio123:

(Benchmark S&P500 equal weight etf RSP 12.8%)

10 small to mega stocks 26.9%

40 micro to mega stocks 21.1%

As long as I outperform RSP, I am satisfied!

My easy to trade (i.e) Microcaps, similar to other models discussed here, returned 55% in 2024. However, over the past 10 years, for me they have averaged around 20% annually, gross of taxes.

Small caps (excluding microcaps) ranged from 15-20% 2024 (north of 8% excess of my benchmark), but net of taxes, thanks to tax-loss harvesting and longer holding periods. This has been my primary area of focus for some time. I’ve found that capacity is extremely limited in the microcap space, especially with weekly or monthly turnover strategies.

Years ago, I realized that you could achieve around 10% annual returns by indexing, with no tax implications. This seemed difficult to outperform compared to model-driven approaches, which often involve drawdowns and uncertain returns. Depending on your tax jurisdiction, you'd have to almost double the index return. Now with indexes like USMV, like what's the point?

I’m curious if anyone is consistently achieving annual returns above 25%, particularly outside of microcaps, gross or net of taxes! Love to hear about it.

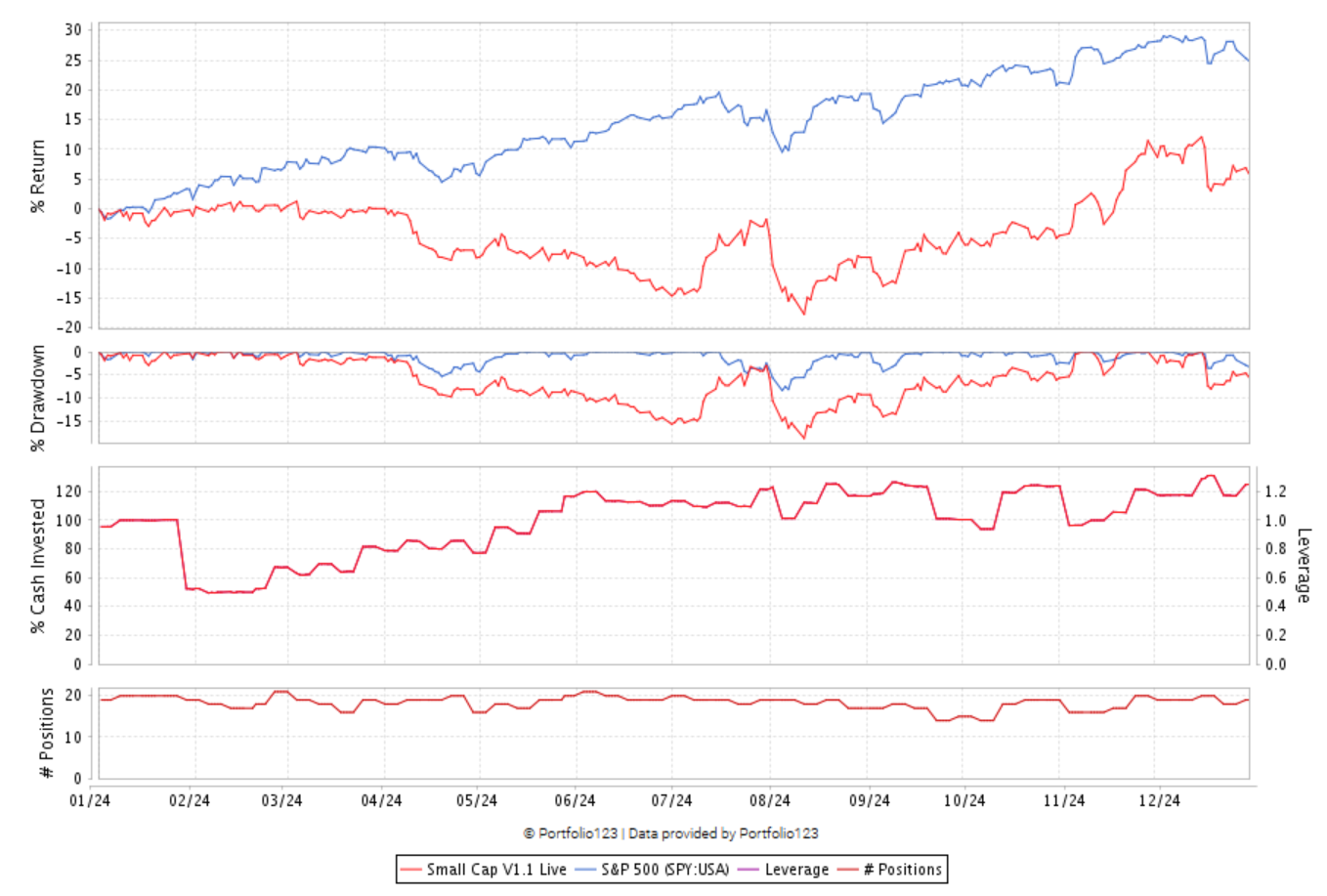

This is also my first full year using P123! I had two accounts running slight variations of the Small and Micro Focus ranking system, but the difference in returns was significant. The first system I suspect that I over-optimized while I was testing out trying to group formulas based on a 5-factor type model.

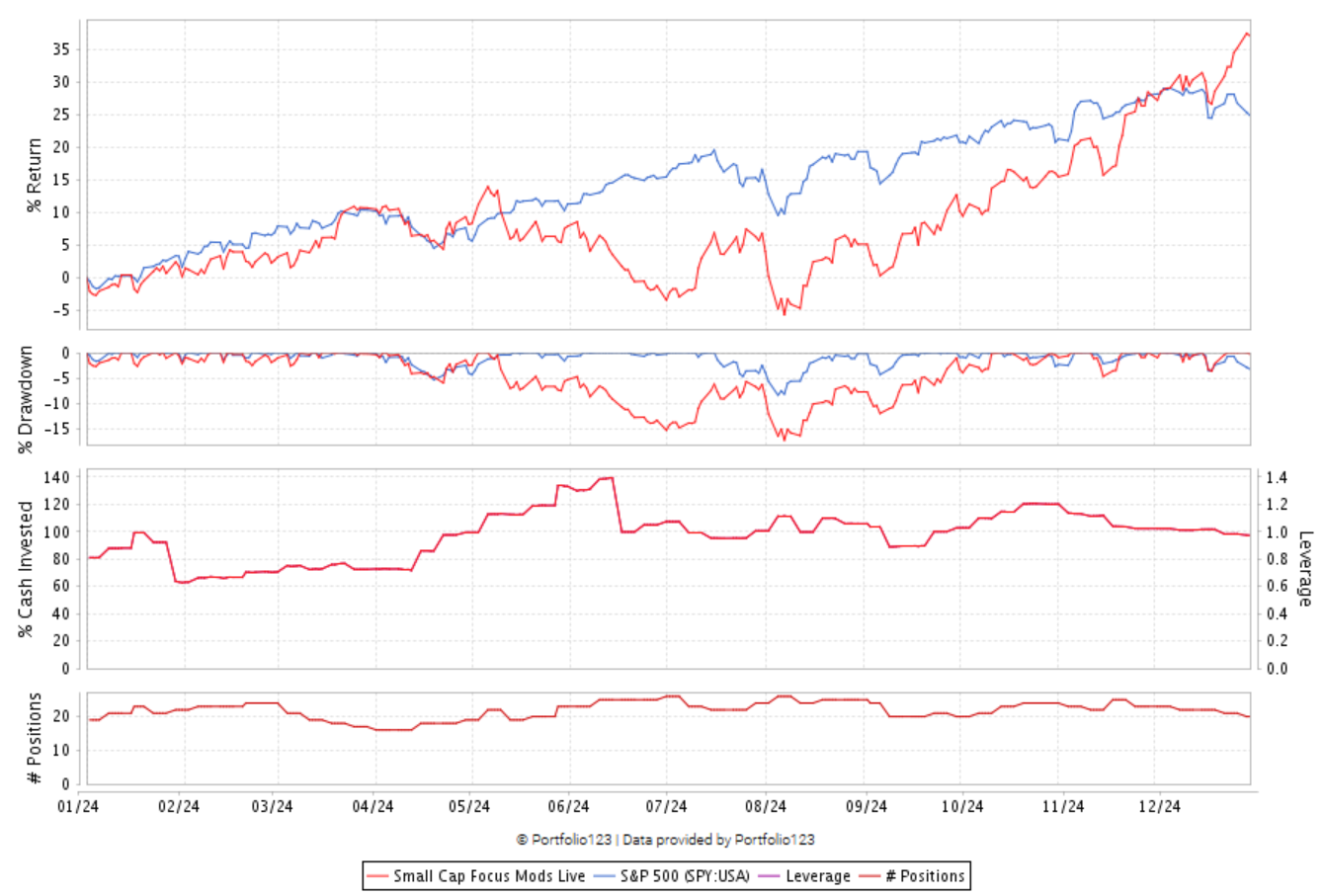

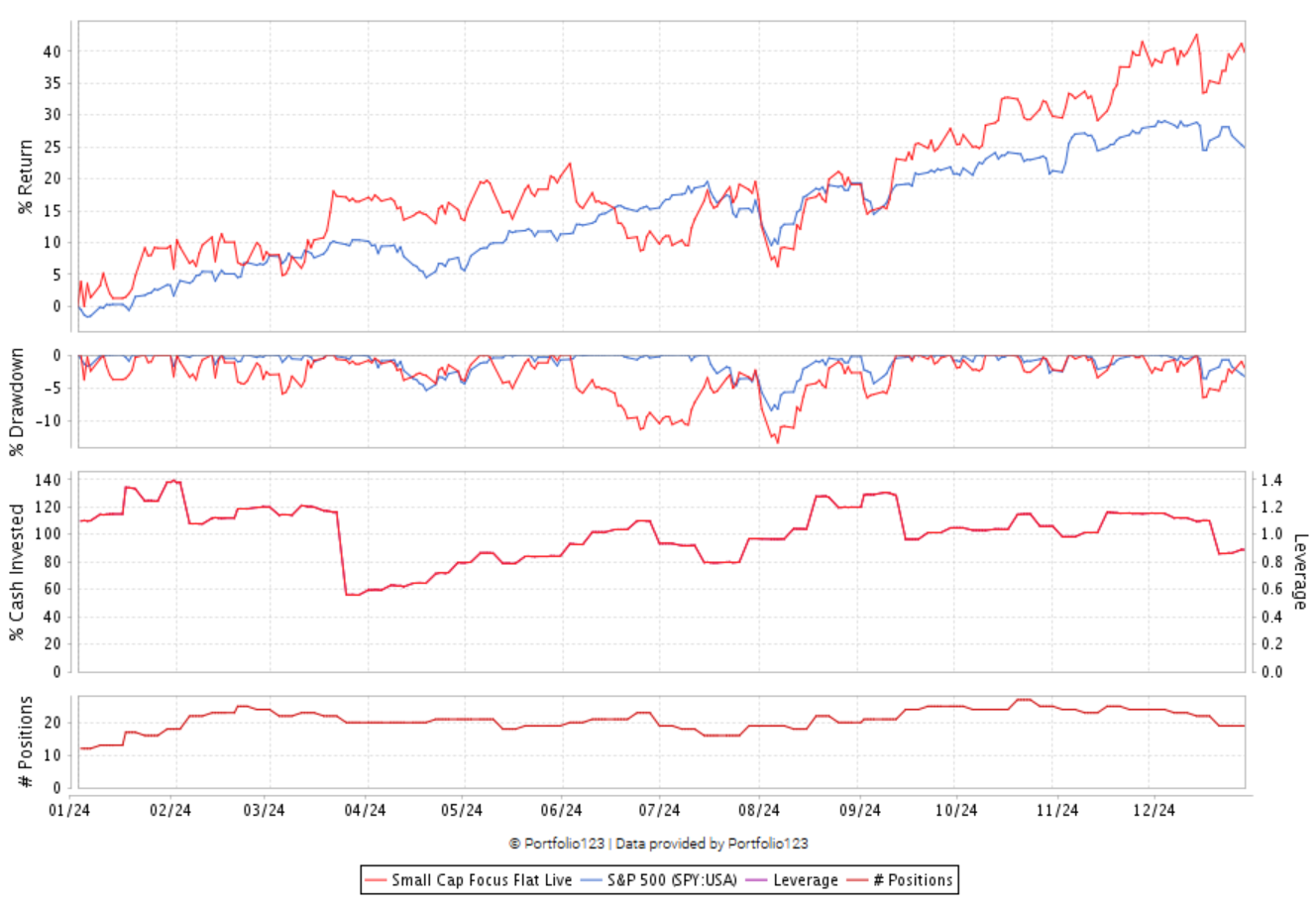

Note in both of these I hold about a 20% cash buffer as I do dynamic position sizing, but without actual margin. Also they are nominally 20 stocks when fully invested.

System 1:

Real: 21% (I switched half way through the year thankfully)

Live port: 6%

System 2:

Real: 41%

Live port: 37%, sharpe 1.5, max DD 17%

I have one more system I am thinking of switching to:

3rd Small micro focus based system: 39%, sharpe 1.8, max DD 13%

But I still have most of my money in other investment methods:

Stock picking/ETF accounts: 30-60%

Crypto accounts: 75% (not really fair, its still close to my cost basis from 4 years ago ![]() )

)

Private investment accounts: 6-70%

Overall a good year and if it was not for a complex tax situation I would load up more on my 3rd live system. As it is I think I will increase my P123 investment in my tax sheltered account and continue to work on developing a AI portfolio with ideally more diversity and less volatility. Unfortunately I have not had time recently to work on the AI model...

Outstanding work—congratulations on those results!

I’ve been reflecting on a conjecture I have: skilled members like you often achieve returns in the 35% +/- range over the long term, with the potential to exceed that in particularly strong years. While this is still unproven, I’ve noticed that most posts in this thread fall within a range of +/-10% around that number, with a few outliers. This provides some evidence for my conjecture, which is also based on my personal experience, Designer Models, and other forum threads. The results seem to cluster around that number, though I haven’t attempted to formally quantify it.

Another piece of evidence for this is that when I expand some models to 50 or 100 stocks, the returns tend to move toward that 35% range. Better results are often more fleeting and could involve overfitting, selection bias, or other factors. Expanding to 100 stocks seems to eliminate outliers—whatever their cause—making the results more consistent. That is the theory at least.

I’m sure the numbers aren’t perfect and shouldn’t be taken too literally—it’s more of a general observation. In any case, great results all around—keep up the fantastic work everyone!

I keep wondering what 2025 holds in store. If you listen to folks like Cliff Asness, Howard Marks, Nir Kaissir, or David Einhorn, the prospects are truly bleak for those who just index or are growth investors. The fact that we all made around 20% to 40% this year doesn't necessarily indicate any particular skills: it was a relatively easy year in which to make money (and it wasn't so hard to lose money either, as I can attest). I have no confidence at all that 2025 will be like 2024. Do you?

Yuval,

Thank you for sharing those interesting references. I've been reflecting on how to best answer your question, and I often like to start by considering the base case and adjusting those odds with additional information. Of course, what we mean by "base case" can be debated, but I think there are two straightforward ways to approach it:

Combining these, I’d estimate the odds of a down year as roughly 1/2 × 4/1, or 2:1 against us having a good year next year. This approach borrows from Bayesian reasoning: starting with base case probabilities and updating them as we gather more information.

I do think these two base cases are independent enough to multiply, or at least close enough to make it useful for framing probabilities. And even if one questions this, the conclusion that the odds are not better than 1:2 was an eye-opener for me. It reinforces the idea that the likelihood of a drawdown in the next four years is high—at least for my benchmark.

Of course, everyone should use a benchmark that aligns with what they’re doing. Some might prefer the cap-weighted SP500 or an equal-weighted version, as long as it has some relationship to their strategy.

So yes, I share your concern. That being said, timing is everything. It wouldn’t be impossible for us to see markets go parabolic first, pushing valuations even higher. The drawdown might not happen in 2025—it could be a great year before things turn.

BTW, using the CAPE in this analysis, as Geov does here, would also be a good idea in my opinion: No, the Market is NotOvervalued Relative to Its Past. I think this is clearly not independent of what the FED is doing, and even then, it doesn’t give us clear odds for next year. But Geov makes a good point, and it suggests a drawdown in the next few years may be even more likely—though quantifying its effect is challenging. Others may not think the CAPE is reliable and might use another metric to adjust the odds.

I’ve been known to be exactly wrong about these things before, but I appreciate the interesting topic and discussion. Thank you again for raising it!

Jim

Whenever I feel tempted to focus on market timing or similar strategies, I remind myself of one key fact: the vast majority of successful long-term investors and investment products never rely on market timing.

A prime example of the risks involved is the zero-interest rate policy, where many bet that bond yields couldn’t go any lower—only to be proven spectacularly wrong.

Trying to predict market dynamics for the next year is ultimately a futile exercise. It's more about marketing to the masses than delivering real value.

I agree 100%. But a good strategy should perform well not only in years like 2024 but also in crashes, bear markets, and corrections. Whether we have one or more of those in 2025 is quite uncertain, but it's worth thinking about and planning for. As I understand it, market timing involves making changes to your strategy according to your perception of future events, not creating a strategy that--if you stick with it--will withstand those future events. The latter is what I'm aiming for.

Ah, that makes sense—thanks for clarifying.

In an effort to repay the favor of your help, here are my thoughts - admittedly not too helpful.

The market environment feels somewhat reminiscent of 2015, during Trump's first year, with tariff threats and similar uncertainties - with the exception of greater risk of inflation. Markets reacted similarly when he won last time in Nov.

There's likely to be a heightened sense of unpredictability, given the White House's apparent desire to disrupt the status quo. Even if no significant policy changes occur, the mere perception of potential shifts could drive securities to behave unpredictably.

Overall, I lean bullish on stocks but with greater risks compared to the first term. Trump seemed to use the U.S. stock market as a key measure of his economic success during his presidency. Based on his cabinet picks and rhetoric so far, it seems likely he'll take a similar approach again. He’s likely to pressure the Fed to maintain a favorable rate environment—potentially jawboning any rate hikes to prevent them from becoming a significant headwind.

"I have no confidence at all that 2025 will be like 2024. Do you?"

No, I don't have any confidence in 2025. We've had a good ride for 2 years but face real financial and structural concerns in the USA which will make the next few years potentially very volatile.

I focus on models which, in back testing, outperform in down periods as well as up periods by holding some cash at times. And I try not to second-guess them or project what the near future holds. My 40 stock model holds some cash when it can't find 40 businesses to invest in. It has not been fully invested since May of 2024, outperformed anyway, and now holds 31 stocks. It just moved from 35 to 31 today. It may rebound, but may not.

Very interesting times, but not reassuring!

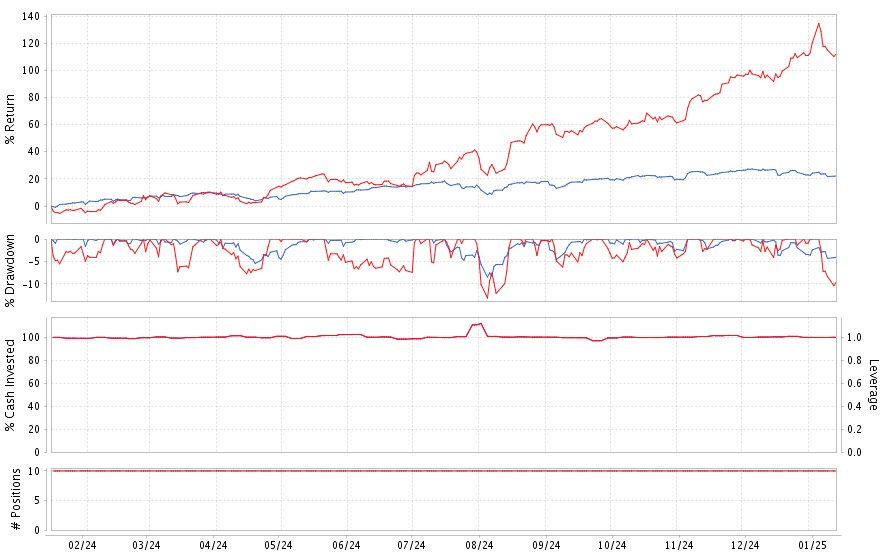

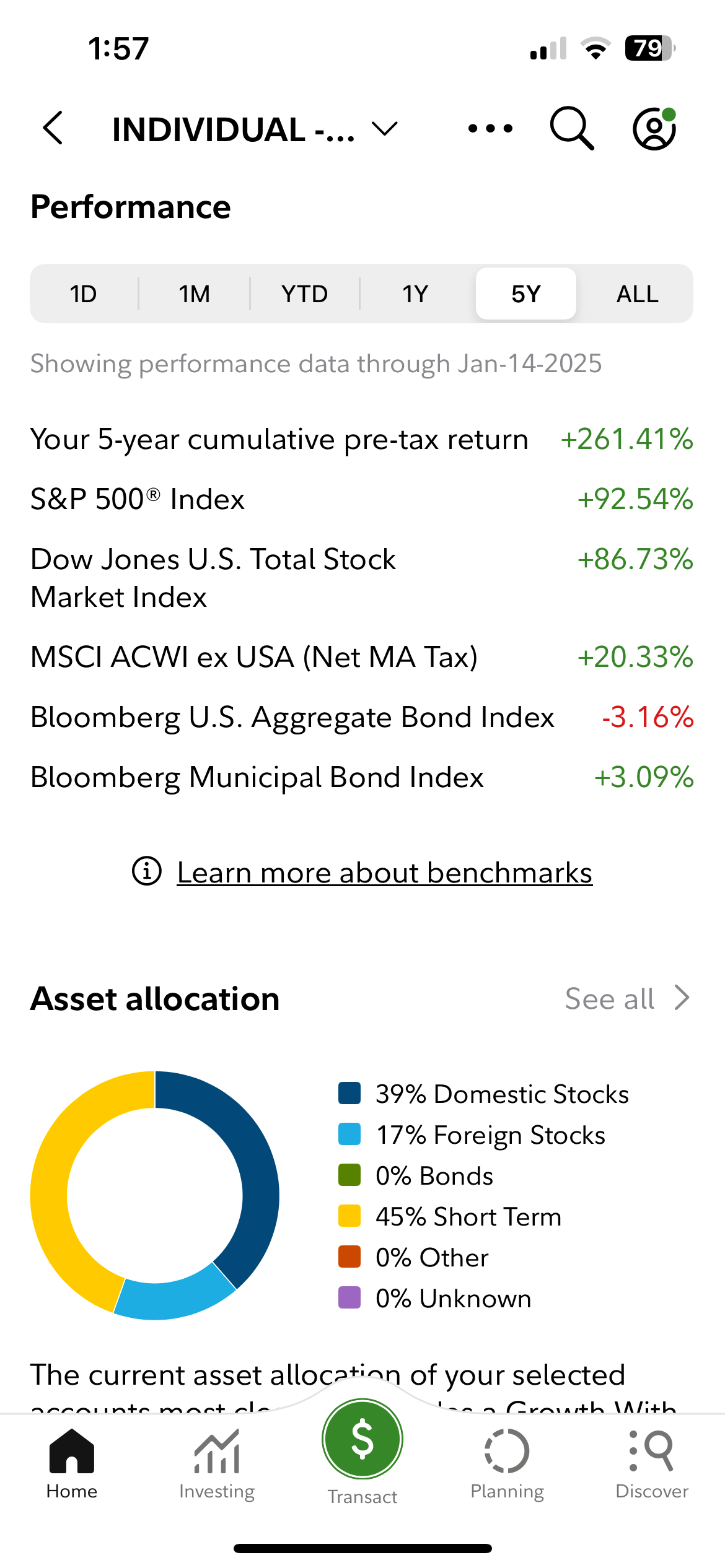

This chart showcases the one-year performance of my best P123 model, focused on micro-cap stocks. Originally developed in 2008, it consistently delivers outsized returns. Implementing its buy recommendations has been a learning process since the suggested stocks are often unconventional and speculative, frequently having already risen significantly. Despite this, the model has remained my top performer after five years of active trading.

In addition to this model, I’ve developed others that outperform the market, including QQQ, R1000, and large-cap-focused models. However, none surpass the performance of my micro-cap strategy. Over the past five years, I’ve achieved a 261% gain, even without compounding, as I typically spend most of the profits.

Given my track record of consistent results and live outperforming models, I am open to exploring opportunities to trade on behalf of others.

From reading the current thread and this thread from July, it seems like The Tale of Two Cities. Then was the worst of times; now is the best of times. An interesting dichotomy for sure.

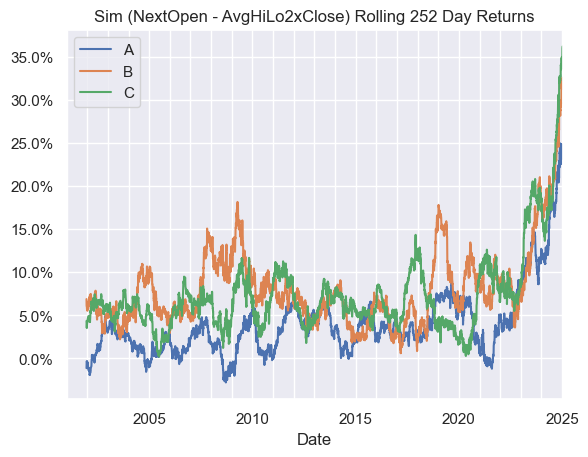

Personally, I have noticed one emerging area of concern with some of my strategies over the past year for which I'd like to raise awareness. For each of three strategies, I run two sims, one that fills at "Next Open" and one at "Average of Next High, Low, and 2X Close" and compare the difference of the 1-year rolling returns. Over the past 18-24 months, the delta in performance has skyrocketed to never before seen levels, meaning the Avg Hi/Low/2xClose sims are badly underforming their Next Open counterparts. The Next Open minus Next Close rolling returns are even bleaker, lagging by up to 45 percentage points last year.

My current hypothesis is that some of the shorter term factors in the ranking systems are now realizing faster than before, within one day. I first considered market impact as one hypothesis but 1) I'm not trading one of these sims and 2) I don't see any reversion, at least over a 5-day horizon. I need to do a further study to see if there is some impact occuring over a longer horizon though.

In response, I've already rolled out new version of these systems that tilt away from shorter term factors, but I have several other takeaways even while I still continue to investigate.

Price for Transactions = VWAP(-1)/2 + VWAP(-2)/3 + VWAP(-3)/6

I don't want to shout fire in a crowded theater prematurely here, but I do sense some smoke in the air and at least want to proceed cautiously and better understand what's occuring.

I had very mixed results similar to Yuval.

A very simple book I run returned 65%.

I have a more advanced book that back-tests better (higher Sharpe, lower drawdown, higher returns), uses formula-ranking and some other techniques that only returned 8%.

What is probably more interesting going forward though, is the first book's backtest (using Variable Slippage and never attempting more than 5% of the daily volume) reports 80% returns. I wonder if this is due to @feldy's observation.

Hi, I would like to know the impact of stock buy and sell commissions on the annual return of your portfolio. I am thinking of starting to use portoflio123 to invest, but I don't know if it is worth it for a retail investor with low capital like me. By worthwhile I mean that it will be profitable in terms of operating costs for a portoflio with 100+ stocks. Thank you

Are you US based? In my experience using Fidelity, commissions have almost no impact on my results. (US Buy and Sell orders have $0 commission and only a small activity fee (~$0.02 per $1000) for Sell orders). Slippage is a much bigger issue ![]()

No, Europe based. In most brokers there is a fee to buy and sell... So you do not connect portoflio123 with Interactive Brokers? You manually place the orders that portfolio123 strategy suggests? Thank you

You say low capital and 100+ stocks. I cannot say what is right for you but in that case I would go with fewer stocks (I have around 20 in my portfolio). I am based in Europe, and even though I pay a commission for each trade, it doesn't matter much. The cost to exchange currency and the bid/offer spread are both higher. Even though, when it comes to currency, I have accounts in the major currencies so I can eg. sell a stock from a Euro country and buy another stock from a Euro country and in that case pay no fee for currency exchange.

A long drag of flat nothing with my old data provider. Then finally full switch to P123 in November and 18% in 2 months making my my whole year.

Painful to see in simulations how the base multifactor strategy I applied since 2019 could have performed with P123 data and tools in the same time frame. Bad data sucks, really regret not switching earlier.

Anyway, now full throttle.