If I check ranks/ rebalance recoms in my running manual live strategies, they get updated daily and I can act on it, e.g. if Ticky XYZ reported earnings yesterday strongly impacting the rank, even though the predefined (weekly) rebalance is scheduled for let's say in 2 days.

If I want to backtest the impact of such daily vs. weekly rebalancings in a simulated strategy, I assume daily rebalance applies Buy/Sell Rules, Universe changes, position sizing etc. on a daily basis but what about the underlying ranking?

In single Ticker rank tabs, the highest rank resolution is weekly. So does a daily rebalance sim actually apply weekly ranks in the background or is there a true daily reranking as in manual live strategies?

Weekend ranks include Monday morning updates around 3AM CDT. Data is continually flowing, so we do one last update before the market opens which is then included if you rebalance after 4AM CDT.

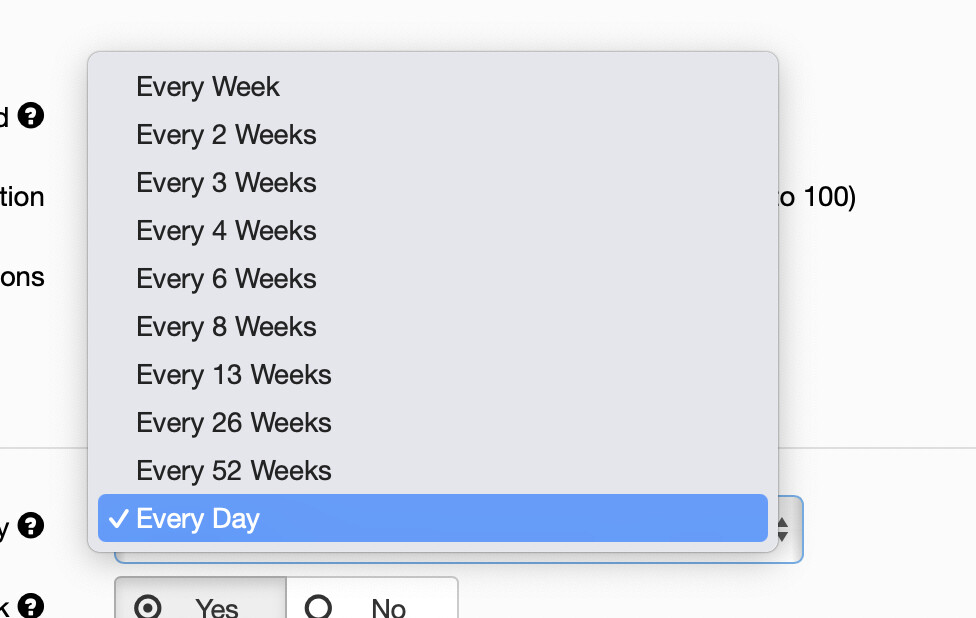

You can actually rebalance every day. The buy/sell rules are updated every day whereas the rank is updated weekly as Marco describes above. But technical indicators and even the price of value ratios like price to sales have the price updated in the buy/sell rules. You could also get an idea of how a stop-loss might work (prices updated).

To be clear something like FCF will not be updated in the rank but I am not sure about what happens in the buy/sell rules. I am only sure that the price changes in the ratio of FCF/Price. I defer to Yuval or others for a definite answer on whether FCF is updated daily in the buy/sell rules.

So it can work for some and it is not rare that people rebalance daily (highlighted at the bottom):

Ok, thanks. That helps a lot. To clarify: I tested my main weekly strategies (which are only based on ranks) as a function rebalance weekday (shifting start date to match Monday, Tuesday, etc.). If I understand it right, the monday strat should exhibit the lowest time lag to the rank information whereas the Friday rebalance should exhibit the highest time lag? That said, I can share the result that the start date did not matter that much in my case. If anything, rebalancing on Monday was slightly worse than average.

Still wondering if there is an effective way to backtest if daily manual rebalance with "real" daily ranks would make a difference (positive or negative). In theory I would assume that incorporated trades following new earnings data directly the next day after release should improve results. On the other hand (depending on the system/signal), a lag could even be beneficial (short-term reversals etc.)?

One could backtest with 4-week rebalancing, 3-week rebalancing, 2-week rebalancing, and 1-week rebalancing and if the results consistently improve one could extrapolate from that to conclude that daily rebalancing will improve results. You definitely have to factor in the increase in transaction costs, though. Also, there is a concern with piling on trades after earnings announcements, as you point out.

For what it's worth, I have found, after about ten years of experimentation with different frequencies of rebalancing, that about twice a week is my sweet spot.

Thanks for sharing your experience. Do you set specific weekdays or systematic criteria for that? Or do you schedule rebalancings intuitively based on signals, days since last trade etc.?

Do you set a minimum holding period before selling? Like generally (unless there is specific reason like a stop-loss) hold for a week or more before selling based on RankPos (or Rank) which can be set up in the sell rules as you know?