If I use a ranking system to rank stocks, that will only be updated on Saturday night and then those rankings will apply for the following Monday - Friday… but if I use buy rules that are based on price or volume data then those buy rules actually work on a daily basis?

If yes, are there any other variables other than price / volume that work on a daily basis?

Thy all work in a port (not looking back in a sim) except for earnings revisions. I had hope for this idea but have been disappointed to date. For some reason I have trouble showing positive cherry-picked examples. I could show some. But no worries with this port or the rebalance daily idea so far (I do not have anything else that I rebalance daily).

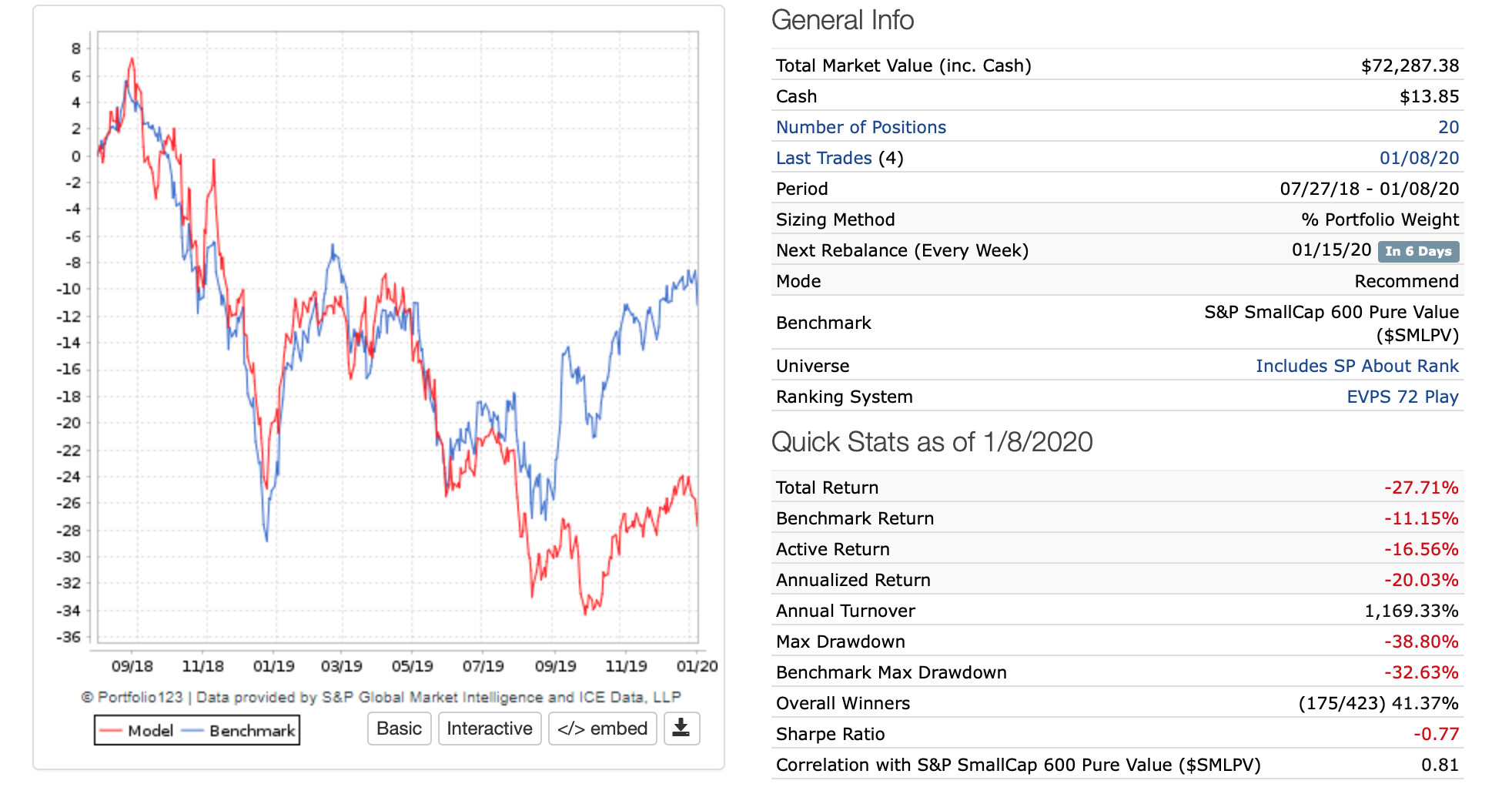

I have no trouble showing this paper-traded port that I take the time to rebalance daily. It even has the benefit of “yesterday’s close” as I just click rebalance each morning with no editing later.

Just to share that it is, surprisingly, not so useful for the factors I use in my port.

Obviously, could be just the factors or the market (value factors, momentum and others).

Yep that’s it perfect thanks. Would it be possible to allow ranking to be done daily in a backtest, assuming the ranking system only uses price / volume data?

That is a good idea, especiall bc. earnings estimates are updated daily. Not sure if it really helps the performance, but worth a try…

Best Regards

Andreas