Good morning P123 team,

I’m looking at some simple calcs for equity.

The basic formula: assets - liabilities = equity (common + preferred)

P123 documentation for comeq:

Common equity is common shareholder’s interest in the company as reported in the shareholder’s equity section of the balance sheet. It is the sum of common stock, capital surplus and retained earnings.

I’m assuming the capital surplus, ret earnings is already included in the comeq value, does not need to be added separately.

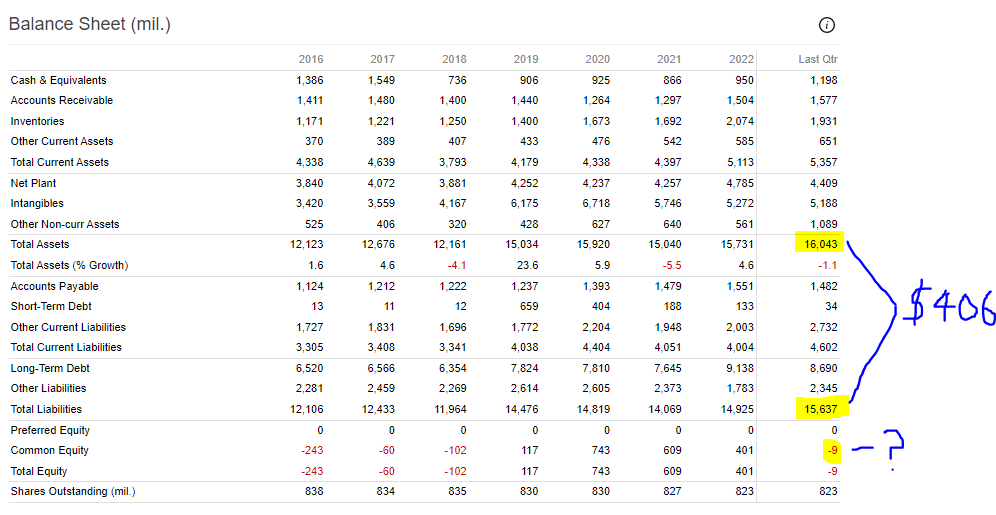

For several balance sheets the basic calcs appear off. For example, CL:

Reported value in the balance sheet (and comeq.q) is -$9M, but simple calc is +$406M?

Is this an accounting nuance, or a data issue?

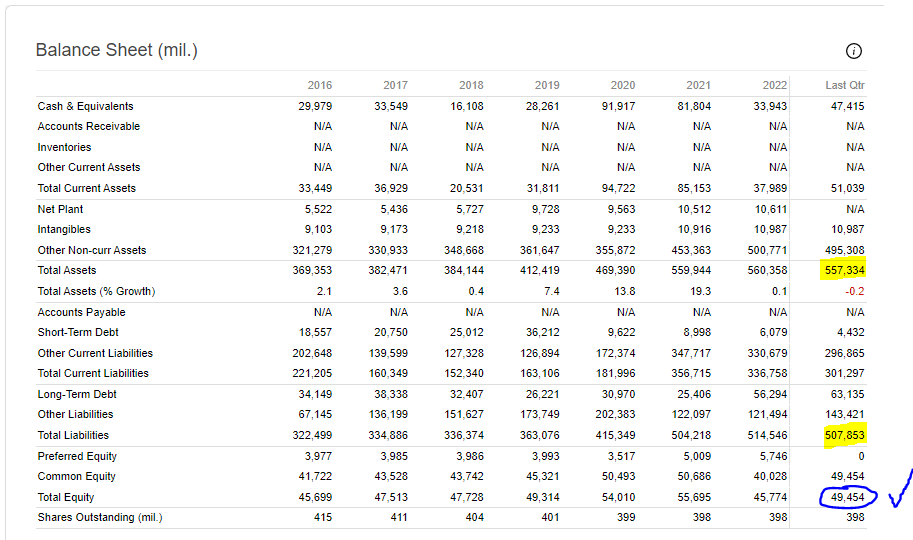

A different issue is where the balance sheet output is different that the comeq value. For example, PNC:

The balance sheet value here works out, $49,454 (not perfect, but very close), but the comeqq value is -$10,261.00.

Any thoughts?

Just screening the R3000 universe, nearly 400 of the 3000 stocks have appreciable differences between the calc’d version/balance sheet version/comeeq values.

First off, just want to ensure I’m understanding the accounting and any nuances there first. But data wise there may be some misalignment as well.

Thanks,

Ryan

Thanks Yuval - I was just about to add to this thread. Looks like most of this stems from my (incorrectly) assuming that “common equity” and “total equity” are synonymous all the time.

Total assets - total liabilities = total equity* (or shareholder’s equity)

*But total equity = common equity + minority interest

And yes, the troublemaker here is minority interest. If a stock has no minority interest, then chances are common eq = total eq. However for companies with significant minority interest, the two values can be very different.

Common equity can include retained earnings and paid-in capital (as the P123 documentation indicates), however they are already included in the “common equity” line and do not need to be added separately.

I’m hoping this will answer my question and resolve the differences, however I did notice a few oddities in the data after considering the minority interest. I’ll do a more comprehensive scan tomorrow and get back to you.

So now another observation - “Return on Equity” - the P123 documentation uses “common equity” in the denominator. Looking at other sources, i.e. Investopedia and others, looks like “total” or “shareholder” equity is used. These could be very different, depending on the value of minority interests. Will need to look at this closer…

Digging further - I think I see where some of the other confusion is coming from.

Total assets - total liabilities = total equity* (or shareholder’s equity)

Total equity = common equity + minority interest + preferred equity

P123 “comeeq” reports common equity, but the total equity “eqtot” appears to capture only the common equity, it does not include minority interest or preferred equity.

In the summary balance sheets on the “panel” views, this is particularly confusing, as the total equity line does not resolve with “assets - liabilities”, as in the case with CL:

In CL’s case, the minority interest makes up more than 100% of total (shareholder) equity (common equity -$9M), but does not appear in the balance sheet view or in the total (shareholder) equity value.

From other P123 documentation, it’s indicated that common equity is used in ROE calcs, book value etc, to remove “distortions” from preferred and minority shares. These are good points, but strictly speaking, I would think SH equity should report all of these items, and then the user can at least have the option to use total equity or common only in their ROE, book value etc.

Thanks,

Ryan

Very interesting discussion. For ROA, if minority interests are added back to equity, adjustment is needed for the income statement as well for consistency. Also there are debates on whether such accounting line items are useful. See for example a paper here Valuing Minority Interests by Doron Nissim :: SSRN