I came across this article which shows that a risk scale of 0-100 can be achieved by multiplying the volatility by five, in which case the risk score of cash is 0, and equity (SPY) is 100. Using this scale, the risk score of bitcoin is 400 and TSLA (Tesla) 300.

The article from your link compares the risk/return profile of a buy & hold (B&H) strategy for Bitcoin/Telsa vs spy.

This may not be a realistic measurement as most successful traders that makes money in Bitcoin trade it (long/short) based on some form of trending following technical analysis (TA) like moving average/MACD/Parabolic SAR. I have added a number of research papers in my Bitcoin thread which has validated using TA to trade Bitcoin/Ethereum which improves the Sharpe ratio by reducing the max drawdown to 25-35% (as compared to over 50%+ for B&H which happens every year).

From someone who has made money trading Bitcoin, I won’t recommend a B&H strategy unless anyone is ready to stomach a 80% max drawdown.

Disclosure : I have no position in Bitcoin after taking profit at the 53,500 level based weekly Parabolic SAR.

Thank you for posting that article. The author compared the return /risk ratio of Tesla to Bitcoin by limiting Bitcoin to 252 trading days and found that they were very similar. He didn’t consider correlation between Bitcoin and TSLA or the stock market which would make it complete (Bitcoin has the lowest correlation to both at .15 and .18 respectively).

I don’t get the premise. Would anyone buy just Tesla? Or just Gold? Or just Bitcoin for that matter? Maybe I would use a timing method for an asset or asset class, but I would never go 100% into anything with my entire portfolio.

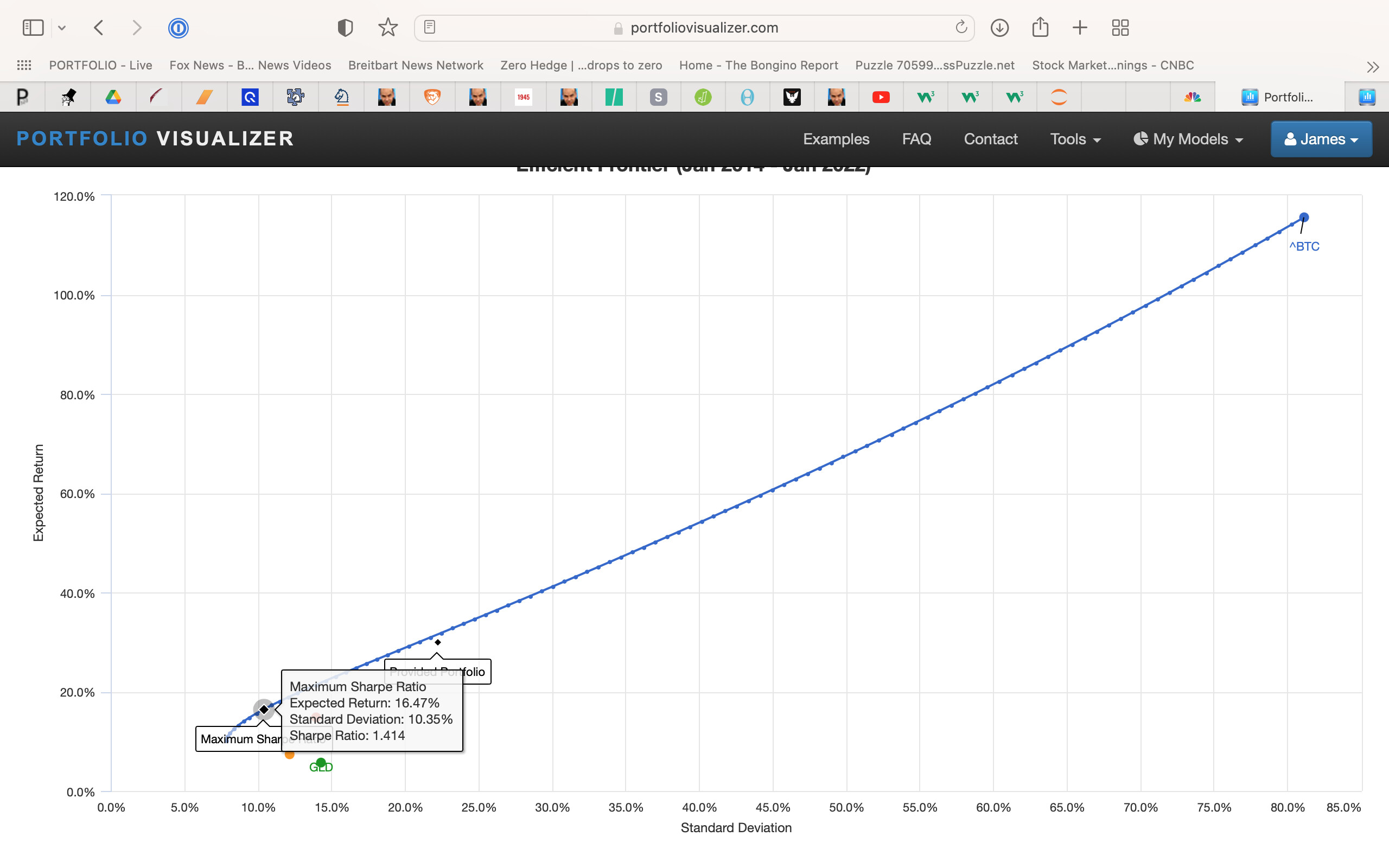

Looking at the volatility of a single asset does not make any sense if you are going to hold a portfolio of assets. And looking at beta in relation to SPY when it has very little correlation to SPY or the stock market in general. What? I think that has no meaning whatsoever.

Not only is Bitcoin poorly correlated to SPY as Scott points out, it is not very correlated to anything it seems. Not even GLD or XLE (commodity stocks). In fact, it is inversely correlated to gold and has almost zero correlation to XLE.

So assuming one does not think Bitcoin is in a bubble or that governments will regulate it out of existence one should probably own some Bitcoin (timed or not).

By doing so one can REDUCE THE VOLATILITY and increase the return of your portfolio at the same time.

A portfolio of SPY, TLT, and ^BTC, historically, has a standard deviation of 10.35% while holding 6.79% Bitcoin (^BTC). One can (should) adjust this based on how one thinks these assets will perform in the future of course.

This is one way to trade Bitcoin. I do something similar but not exactly the same way. Right now I don’t have any with my risk parity model it’s ranked the lowest out of 10 uncorrelated portfolios. If your crystal ball says bitcoin is going to zero then yes it’s a bad idea. I don’t think it’s going to zero.

Crypto could be at a pivotal point in its evolution as per this article

" Now, as we near the implementation of potentially restrictive guidelines and increased oversight of the industry, crypto firms have a decision to make: grow up and be regulated while dishonoring Bitcoin’s anti-censorship ethos, or continue to rebel and face the consequences. "