You’re welcome Alan. I find that the quality of my work noticeably improves when I share it because of the feedback and because it forces me to think a little more.

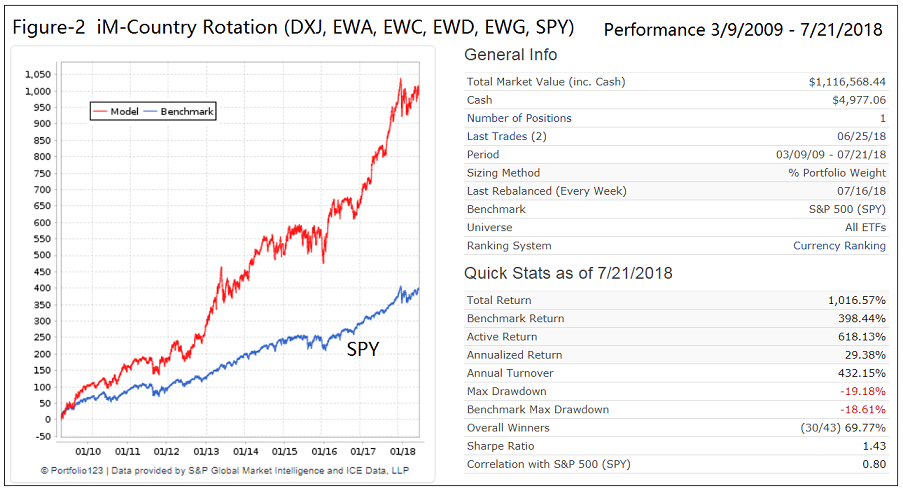

BTW, the equity curve is not nearly as beautiful as the ranking system buckets. I suppose it’s because the major world stock markets are correlated with each other and rotating from country to country is not enough during volatile times. I wonder if there is a way to hedge this volatility.

I may be misinterpreting what you are trying to do as I do not usually use custom formulas but are you trying to create a system that buys a stocks index based on depreciation of its currency? If so shouldn’t you also consider the velocity and duration of the currency move (a short term 25% currency move will have a much larger impact than a 1% move over a year)?

"create a ranking system that ranks country ETFs based on the strength of their currencies. This is a proven method to rank the equity markets of countries. " Chaim, do you have a reference for this? My prior data search on this topic has shown no more than a short term correlation.

I may be misinterpreting what you are trying to do as I do not usually use custom formulas but are you trying to create a system that buys a stocks index based on depreciation of its currency? If so shouldn’t you also consider the velocity and duration of the currency move (a short term 25% currency move will have a much larger impact than a 1% move over a year)?

[/quote]Hi Scott,

Thanks for your interest. I tried other lookback periods and one year gave the best result for me.

I don’t always remember my sources. I have seen the link between a weak currency and a stronger stock market in at least two different sources with backtests going back about a century. But I tried to find the article that I saw but came up empty. I read dozens of articles (and a few booklets) a day related to investing. The chart looked very similar to Steve’s. Perhaps someone else remembers it? Was it in one of the Credit Suisse reports?

I became interested in developing this system after seeing the link between quantitative easing, currency depreciation and the stock market. First the US Fed eased and the US stock market went up. Then Japan eased and it’s market went up while it’s currency fell. Next the EU eased and we see the Euro weakening and the European stock markets rising. It seems a bit too correlated and predictable to be coincidental. I don’t [yet] fully understand the mechanism linking weakening currencies to rising markets. Perhaps a weakening currency is simply a sign of QE and it is QE that pushes up the market?

While this system works, I don’t [yet] know how to use this system effectively. It is not an effective hedge to US equity because world economies are interlinked. I’ll take my US stock picking models over global equity ETFs any day of the week until I have millions to invest. Perhaps once we get global data on P123 then we can use this type of system to choose which country to invest in.

What do you mean by “short term”? I made a simulation that mainly uses currencies to predict country outperformance and it beats the SPY easily.

The window for this sim is during a short period of time (this is a limitation of the currency data set) that as you mentioned in your post has had currency moves that have been initiated by quantitative easing. Currencies without quantitative easing can remain range bound for long periods of time (years). If currencies are range bound and/or have smaller movements in the future (assuming that quantitative easing ends) then the currencies will have less of an impact of the stock performance of the respective counties then what we have seen in the last few years. As such a system based on buying a countries index based on its currency direction may be less predictive in the future than it has been in the past. However I do not presume to be a currency expert so if anyone has a reference indicating a strong lead lag type relationship between currencies and country performance that extends to the period prior to quantitative easing then please post the reference.

Thanks for the link but I am specifically interested in any papers showing a statistically significant lead lag type relationship between currencies and country performance that extends to the period prior to quantitative easing (I have not been able to find one).

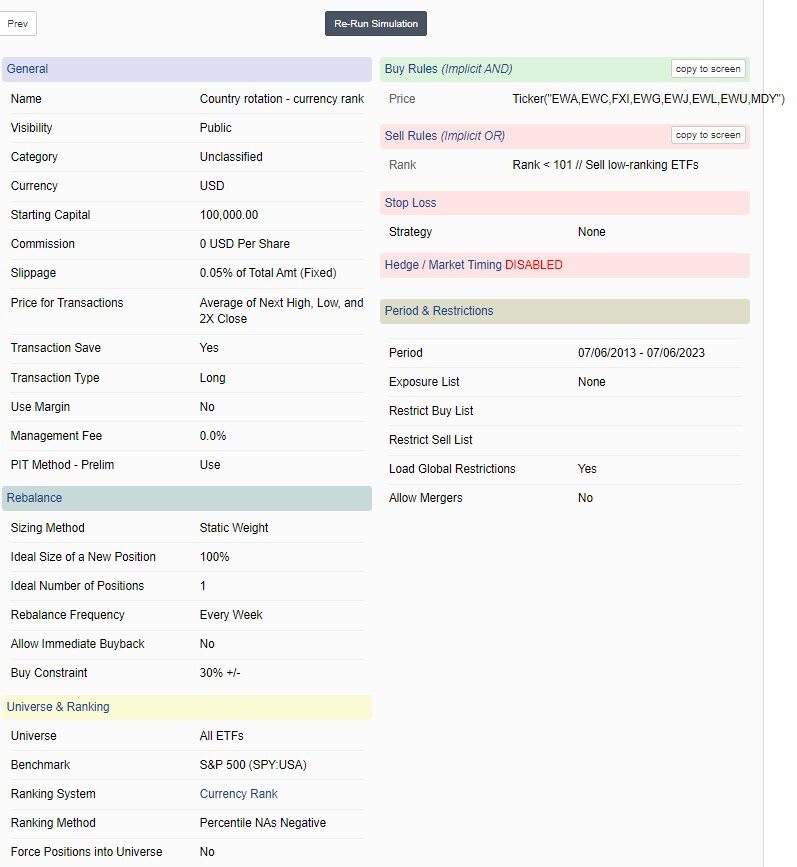

I looked at this topic from 3 years ago and based on Steve’s method developed a model that picks country ETFs based on the performance of their currency ETFs. I think this is a good method, because momentum ranking does not work.

Here is the link to the model description, which can be replicated using information contained in this view-thread. https://imarketsignals.com/2018/performing-us-market-im-country-rotation-system/

Thanks for the information. I’d like to update and add a risk on/off filter to this country ETF strategy. Unfortunately, I have not been able to get the base system (ranks by weakest currency) to work. Am I right that we create a custom formula? I’ve updated the text above to remove currency ETFs that are no longer available… my feeble simulation attempt is included below

How can this work in a ranking system? You are not measuring anything.

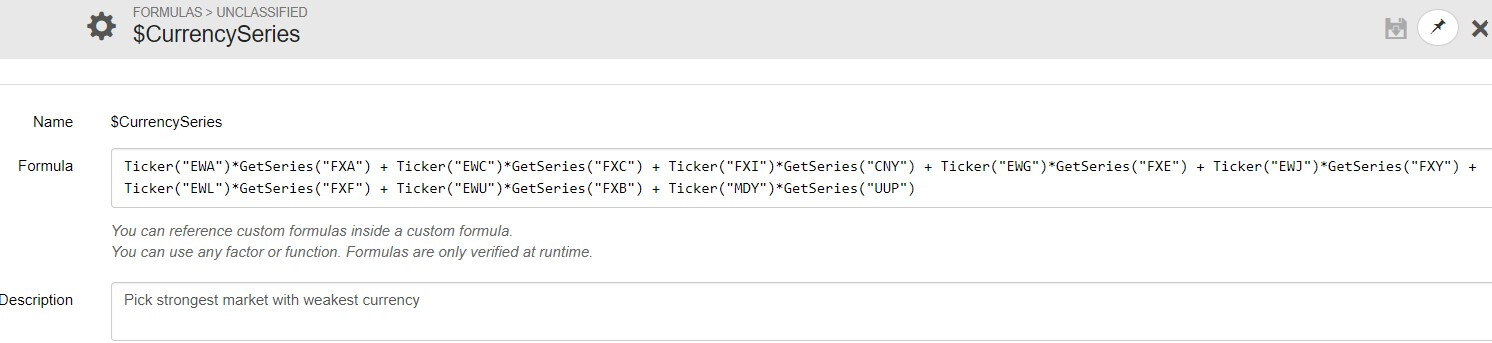

You want to measure the performance of the currency ETF over a specific period. For example, 1 year. Then this would be

Close(0,GetSeries(“FXA”))/ Close(252,GetSeries(“FXA”)) instead of GetSeries(“FXA”) .

Change your formula accordingly, with lower being better, and you will have a functioning ranking system based on the one-year performance of the currency ETFs.

Thank you for your responses, although I still do not understand a good way to do this. I’m willing to brute force calculate the total return for each currency ETF over the past year, then use an Eval function to set the ticker based on the ranking of the currency return (weakest is best). When I use showvar to create a variable for the total currency return I get an error.