I have a system divided into 7 factor themes, with around 150 nodes, where some nodes are weighted up to 10% and some down to 0.2%

I have noticed that when I test the ranking system in the simulator, even though I use 25 stocks in the portfolio and a test period of 20 years, with the US and Canada as the universe (5500 companies), very small changes in the weighting of the nodes can result in large percentage changes in returns. A change in weight on a node by 0.5% can cause the entire simulator to produce 3-5% worse returns (from 49% to 45%), although I tested it on a portfolio of 25 stocks.

Is that normal? I would have thought that since the portfolio is so large, and divided by the number of nodes and factor themes, as well as the period in which it is tested, it would be a little less sensitive?

I’ve been looking a bit for ways to reduce slippage. I see there are some that recommend VWAP orders when I trade in stocks with low volume, but if I don’t use market orders and only place limits at yesterday’s close (or close) until the order is filled, will there be anything to be gained on TWAP orders? (maybe I have misunderstood what the VWAP order dose)

The reason I ask is because that type of order is a lot more expensive to trade, and it can only be used for one day at a time anyway.

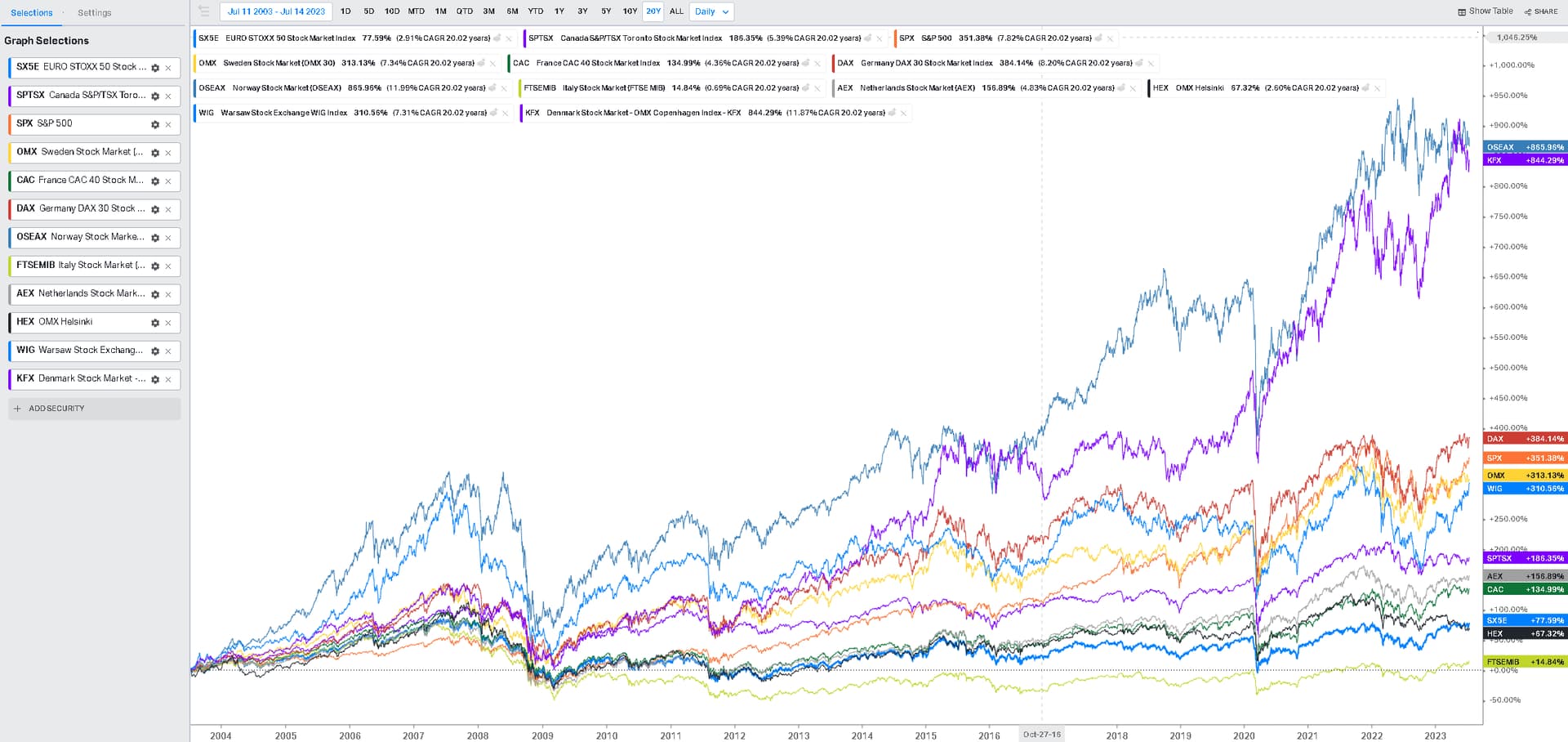

Until now, I’ve split the portfolio 50/50, between the U.S., Canada, and Europe, but how do you guys distribute?

There is no doubt that historically, the US has been the best over the past 15 years, and in the simulator tests I do, the US provides much better returns. So even though I achieve pretty much the same alpha in Europe and Canada, the total yield is much better in the U.S because of the overall market.

But we don’t know anything about the future; it may be overfitting - and a bad idea - to distribute the portfolio based on past history?