– THE NEW DATA WILL BE LOADED SHORTLY IN THE SIMULATION ENGINE AND WEBSITE

Dear All,

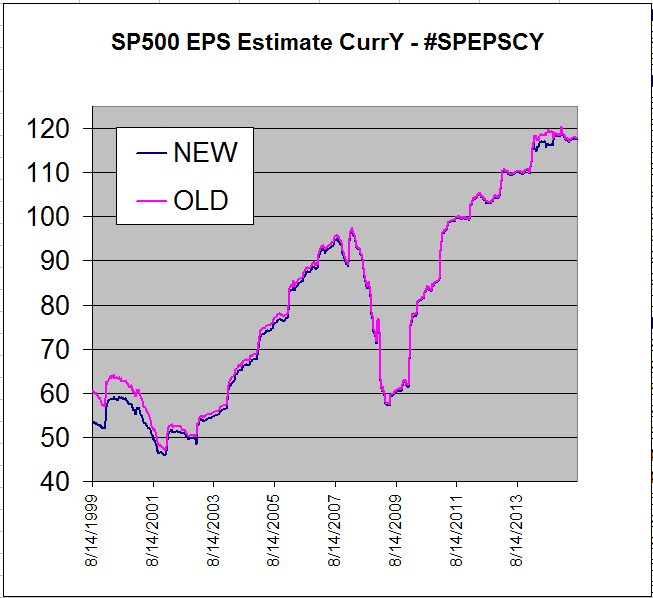

As mentioned in this thread we found a problem with the S&P estimate series (like #SPEPSCY, #SPEPSNY, etc) used for our Fed Model and used in many market timing signals.

The problem had to do with an adjustment factor when NA’s are encountered (typically with estimate data, and particularly at the beginning of our data in 1999-2001). The adjustment was being applied to both the numerator and the denominator thereby eliminating the effect of the adjustment, and simply inflating the values.

The new algorithm can be seen in the custom series samples: https://www.portfolio123.com/app/series/summary/37?st=1&mt=8

Enclosed please find an image of the new vs the old S&P500 Current Year estimates. I don’t think it will have a major impact in systems since the overall trend is the same. However notice the bigger differences found in 1999-2001 when more NA’s existed in the estimates data.

Very sorry abou this. Let me know of any question/issues.

Thank you