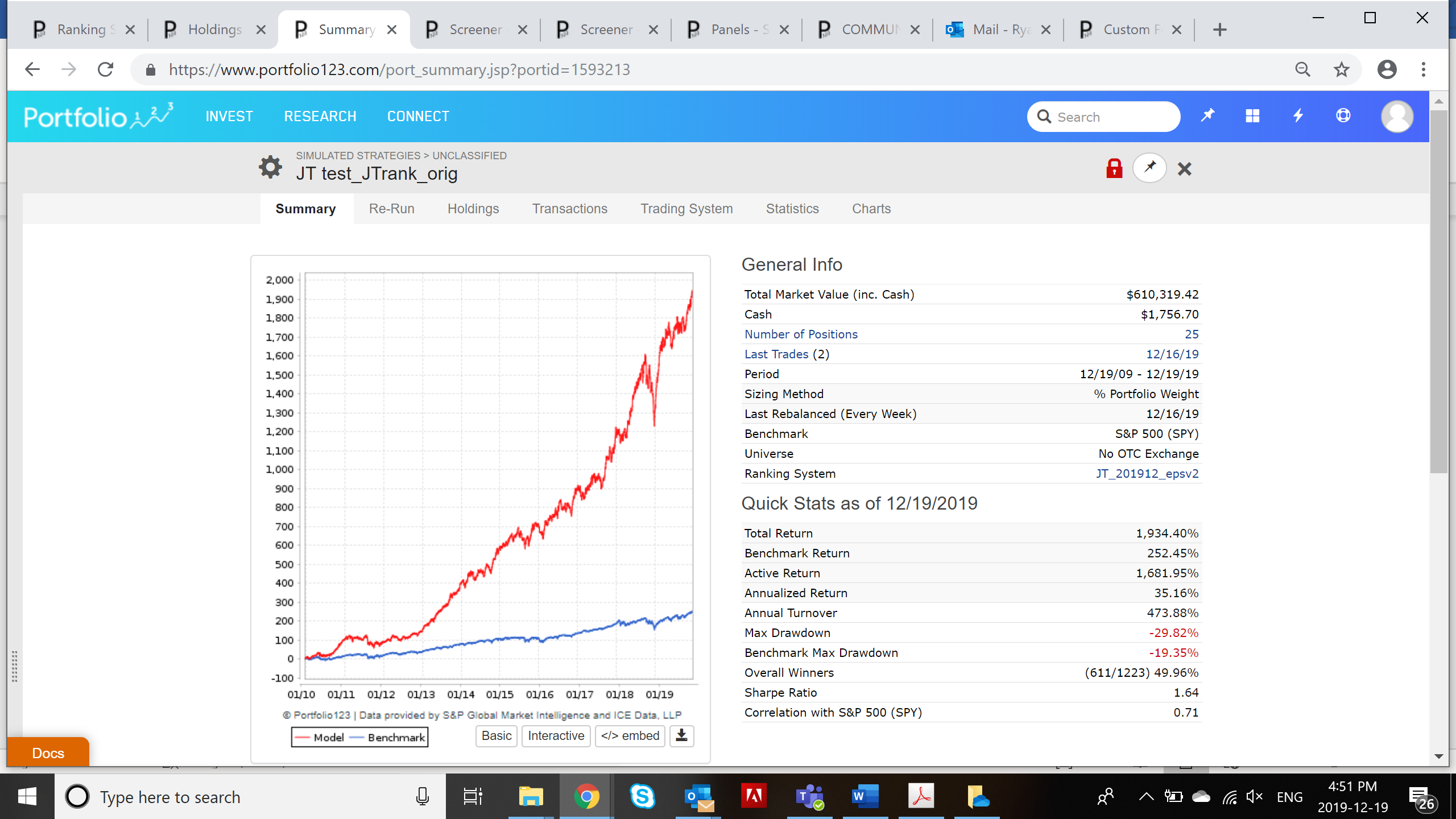

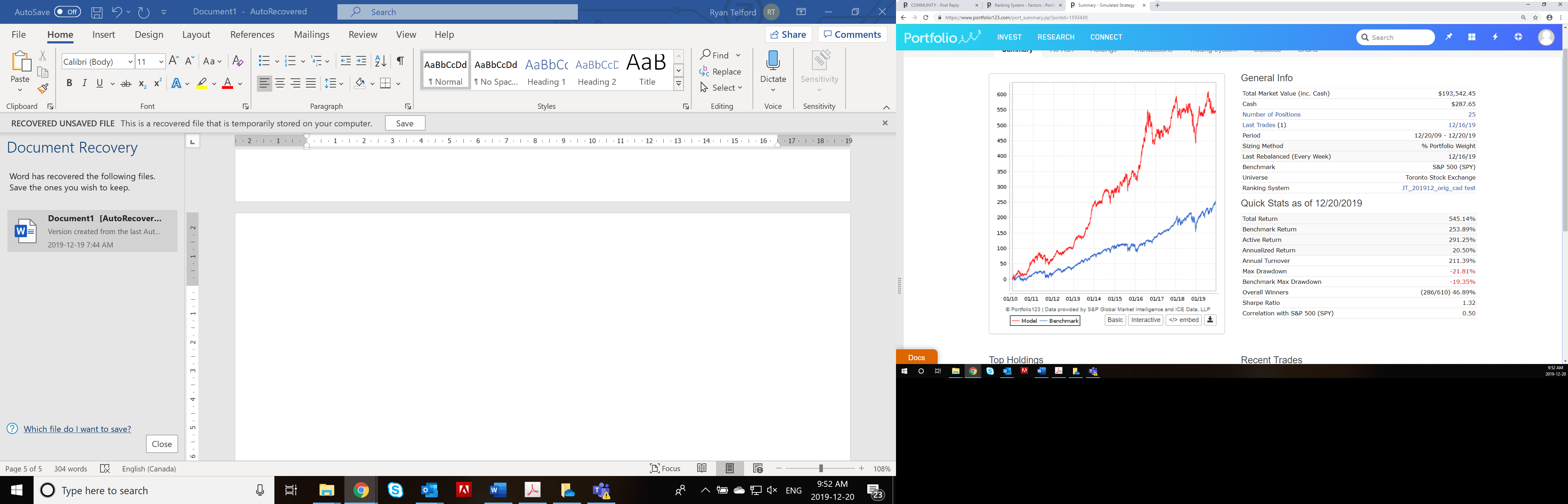

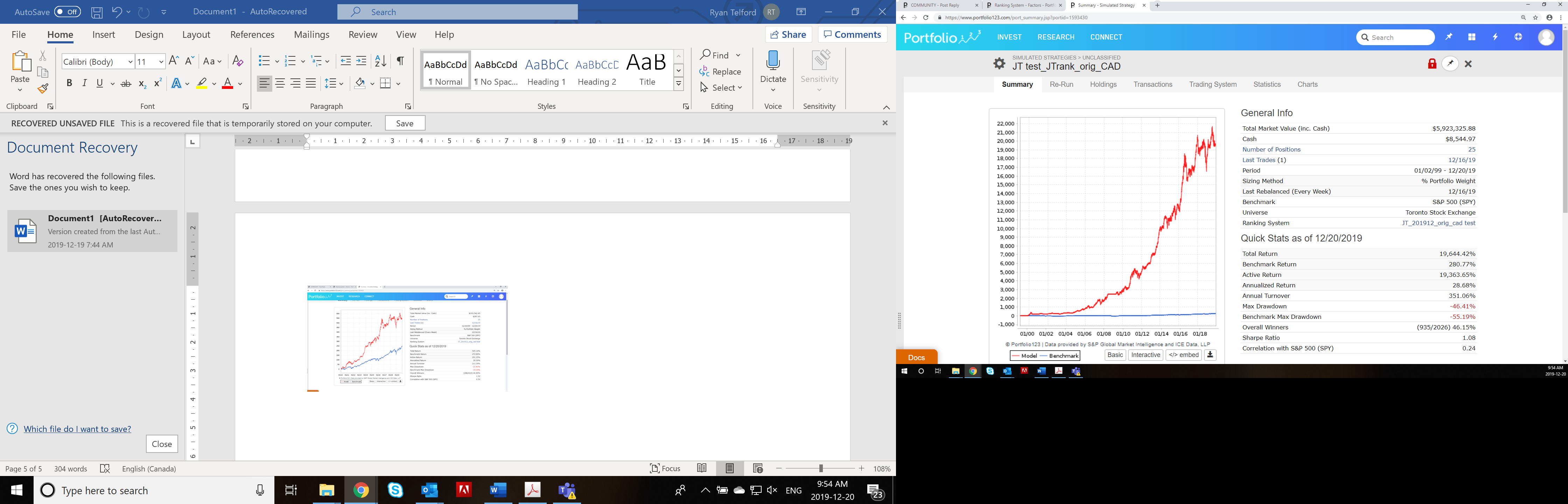

Good discussion here folks.

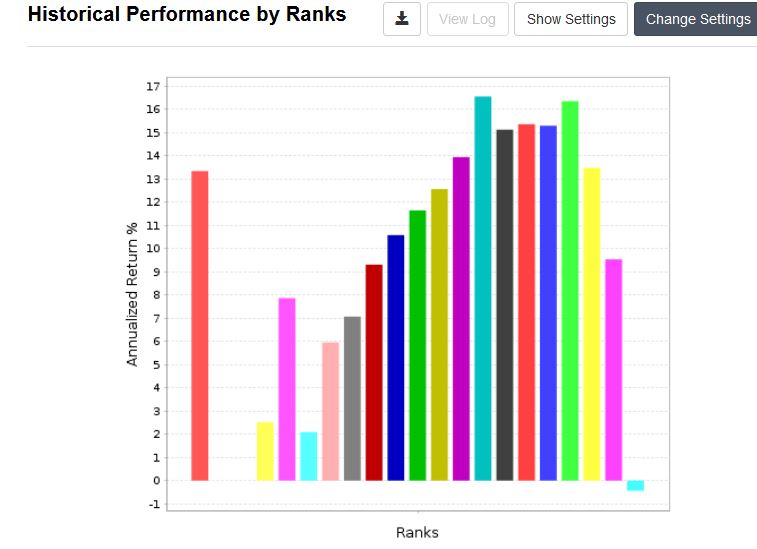

I agree that it’s important to see how multiple factors work together, however I’d have to agree with Yuval’s point above, many factors are mean-reverting, i.e. stocks with a particularly high factor score may be at the peak of their cycle for the given factor and can be positioned for a downswing, indicated by the drop in performance of top ranked deciles.

Another possible source for the drop-off in top ranked deciles is outliers. An exercise I find very helpful is to screen the stocks for the given factor and take a look at the actual values for the factor across the stocks, not just the overall rank chart.

I’ve actually been looking at this recently in the Magic Formula (and hopefully a Seeking Alpha article to follow). Take Return on Capital from the P123 Greenblatt ranking system:

OpIncAftDepr(0,TTM)/New Working Capital or ( NetPlant(0,qtr)+ Recvbl(0,qtr)+ Inventory(0,qtr))

If you create a screen report with this formula, you will find the median ROC values for the top 30 stocks today is 19%.

The stock ranked as #10 is INVA, a pharmaceutical firm. Its ROC is 365%, a significant outlier from the rest of the portfolio. Maybe there’s good reason for this, however it’s worth digging deeper.

INVA currently has no net plant or inventory assets on its balance sheet, so the numerator in the ROC equation will be quite small, resulting in a very high ROC value, and also a high Magic Formula rank.

Is a ROC value of 365% predictive of future returns? As INVA is an asset light company, ROC is likely not a good factor to use for INVA and may not be predictive of future returns as the Magic Formula intended.

For what it’s worth, INVA lost 24% since being purchased by the Magic Formula model one year ago.

This is one specific example, but the point is that it may be worth taking a look at the actual values of the stocks being screened by your factor(s), outliers like the above may also be skewing your decile ranking performance results.

Cheers,

Ryan