Andreas,

Thanks for sharing your system on this forum and Youtube, I have to say I like it so far!

I’ve made some assumptions on your remaining RS nodes and buy/sell rules, but staying within your criteria of low volume small caps, here is what I’ve come up with (consider this ‘base case’):

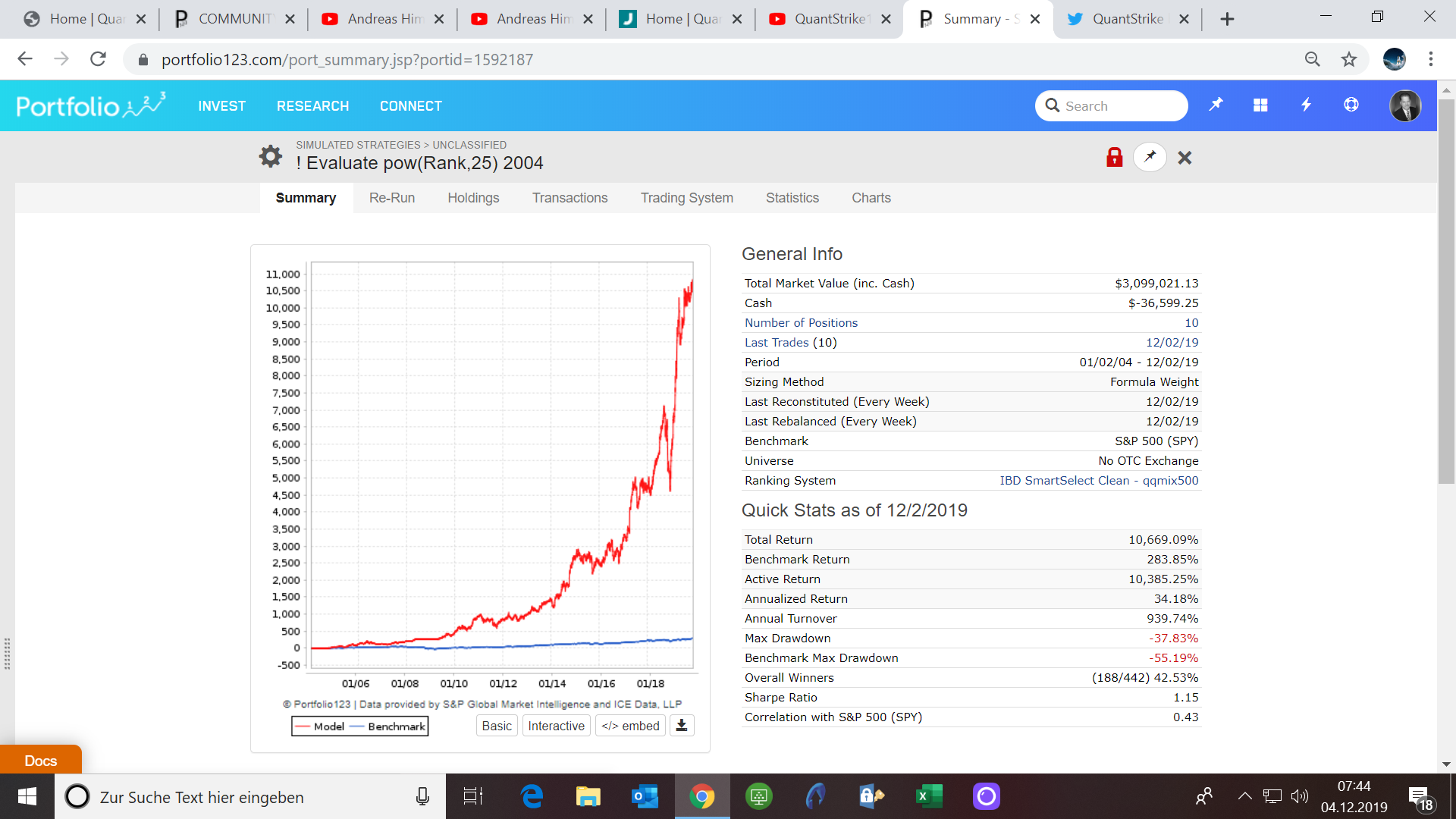

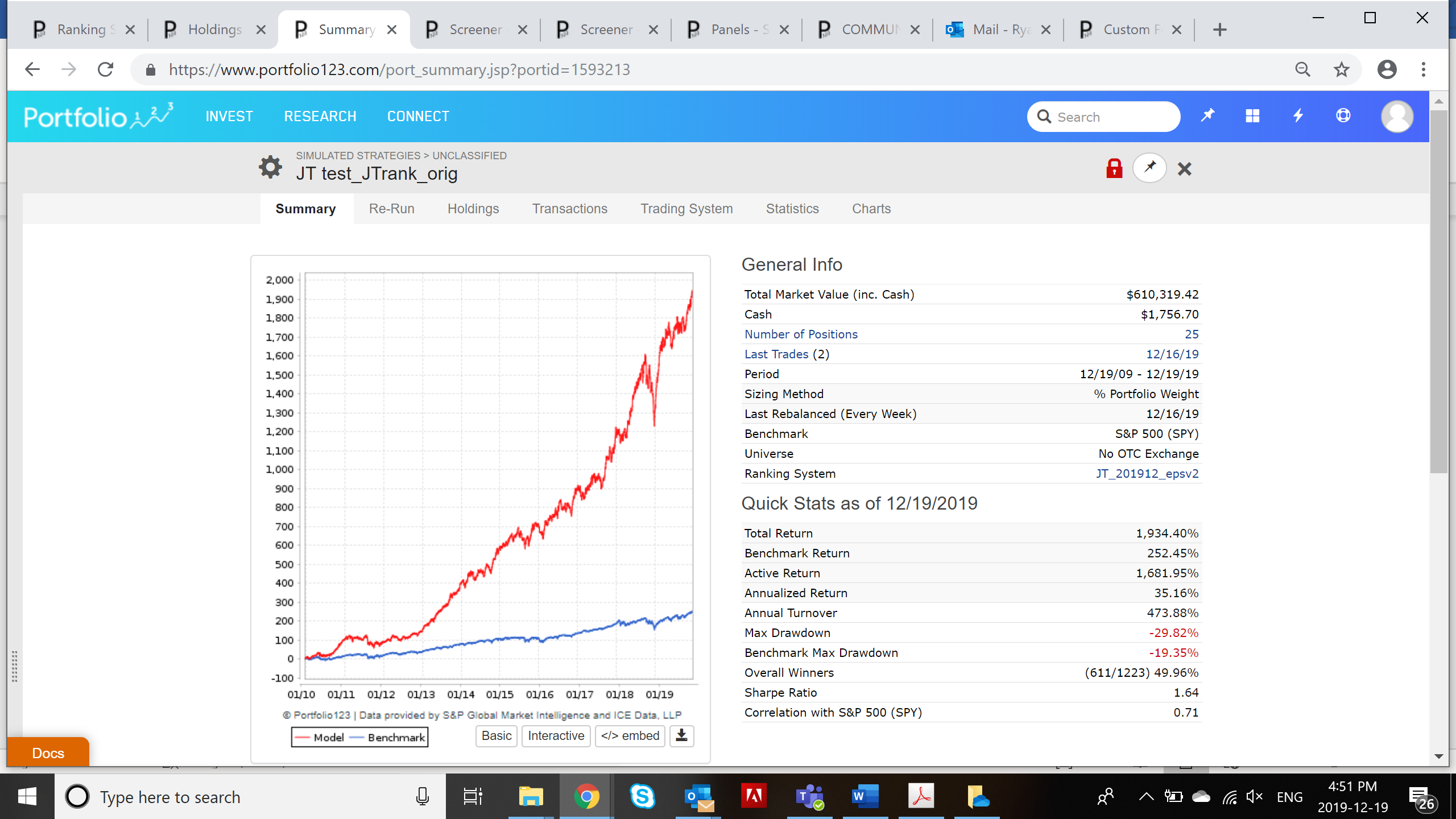

Variable slippage, w/ market timing, buy rank>80, sell < 70, all RS nodes you provided are unchanged:

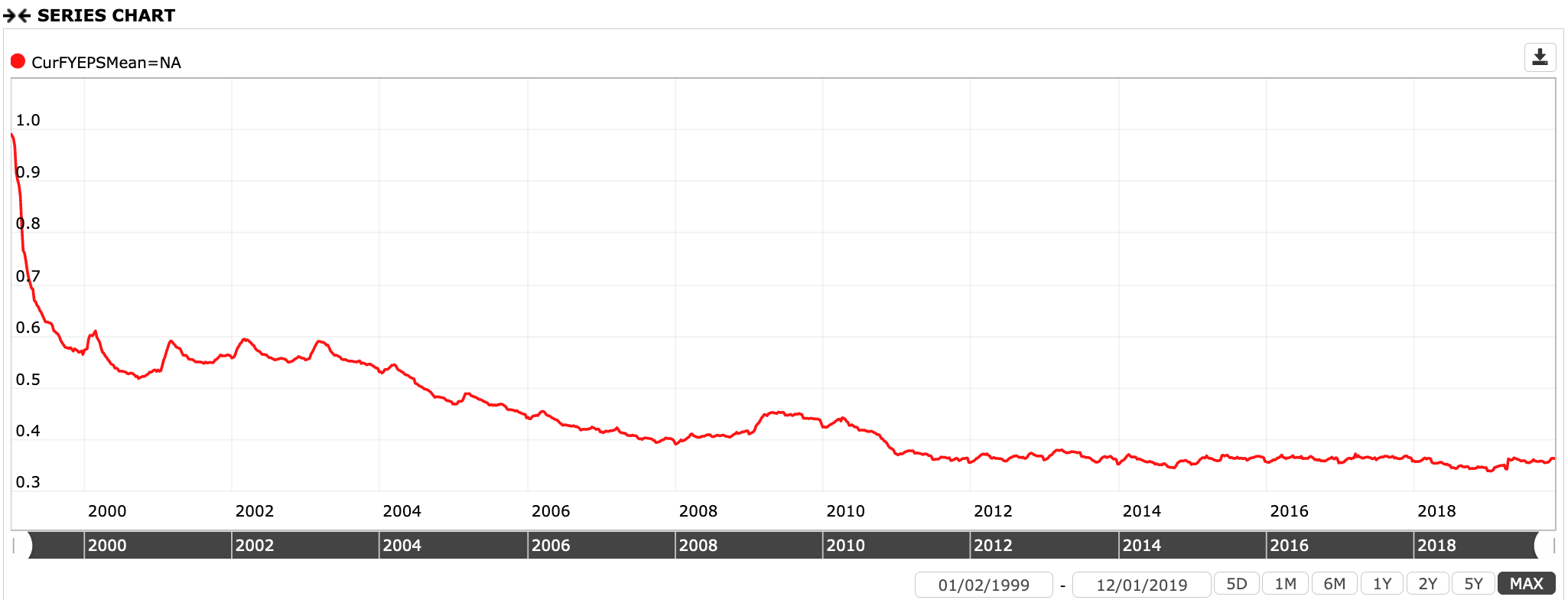

![]()

![]()

Very similar results, but slightly higher turnover.

I have variations of a buy rule that screens for high ranking EPS, results vary for different time periods.

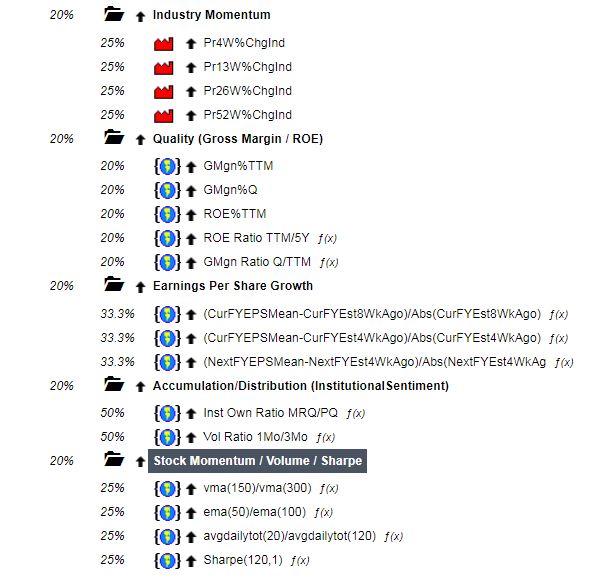

I’ve tried different tweaks on the ranking system with varying minor improvements, feel free to try some, sim results will vary depending on how our buy/sell rules differ, other elements of the ranking system, etc:

• EPS Growth

o Negative values can be problematic, the rule for TTM is nice as it screens out any -ve value EPS’s.

o For quarterly, can try this:

o (EPSExclXorQ - EPSExclXorPYQ )/max(0.01,abs(EPSExclXorPYQ))

• Quality

o Marc provided some suggestions on (a-b)/abs(b); I tried this as well, but with little impact.

o ROE% 5y AVG will result in NA for any companies less than 5 years old, which may skew results. On the other hand, this is also like a screen to give credit to any firms with a minimum 5 yr history. Could also tweak formula to rank NAs negative for this formula (haven’t tried this yet)

• Accumulation/Distribution & Stock momentum/volume/sharpe

o Can try using median volume instead of average volume in calcs. This will eliminate some of the outliers in average values.

• Rank industry/sector specific factors on “industry” or “sector” rather than “universe”

o Profit margins can vary by sector/industry, try ranking by sector/industry

o Same with EPS factors

Let me know if these work out for you.

Cheers,

Ryan