Here’s what I think:

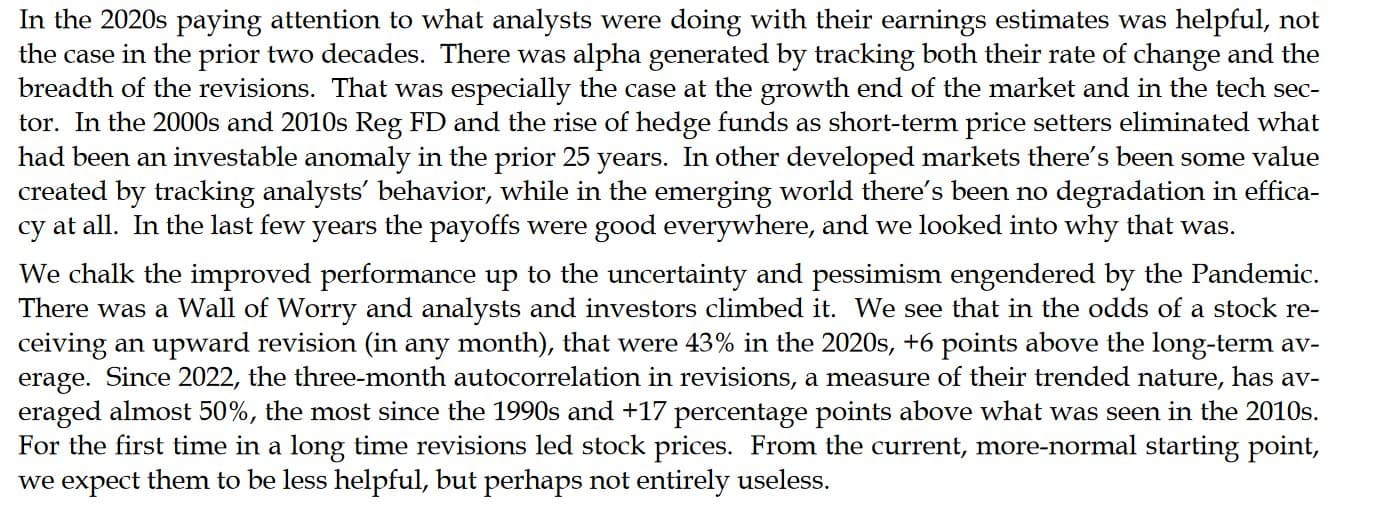

The article argues that "stocks are overwhelmingly moving on forward EPS revisions.” Furthermore, it states that "factors that are really continuing to work are quality and 3-month earnings revisions."

Later in the article, the author mentions that "when a factor is generating alpha, it has a tendency to trend. Its success attracts more proponents, which only makes it work even better."

Basically, the author observes that stocks scoring high on two types of factors (earnings revisions and general 'quality' metrics) have been performing well recently. The reason this is important, in his view, is because “factors trend.”

I think the article provides some interesting hypotheses that could be tested in P123, like the author does with 3-month EPS revisions. The same could be done with quality metrics. Other hypotheses might be, “Stocks with extreme valuation multiples (e.g., P/E ratios significantly above historical norms) are more susceptible to price corrections,” or “Stock price movements are more strongly correlated with EPS revisions than with analyst recommendation changes.” I think most people who have used P123 for a while have probably tested these hypotheses already in one form or another to try to enhance their strategies.

One statement I haven’t tested before is, “over time, if you buy the higher ERR (earnings revision ratio) countries and short the low ERR countries, you have another winning strategy.” When Asian stock data becomes available, this would be something I’d want to test. Meanwhile, testing ERR breadth in industries or subsectors in P123 could be interesting right now, using an aggregate function. I’ve tried similar approaches already, but it might be worth revisiting.

More interesting, though, would be to test whether increasing the weight on trending factors indeed boosts performance. I feel like the author assumes this without providing 'proof' or any indication that it’s true. I find it challenging to test robustly in P123 whether including trending factors would significantly improve my strategies' performance.

Ideally, I’d like to be able to dynamically adjust, for example, the weight of my "Growth" node over time in a ranking system when the "Growth" node has performed well over the past “x” years. However, I believe this isn’t possible for nodes in P123 right now. It can be done for individual factors, but that approach becomes cumbersome (requiring custom formulas for each factor) and limits flexibility (adding any new factor to the system would mean manually testing it for trendiness and adding a custom formula).

My $0.02.