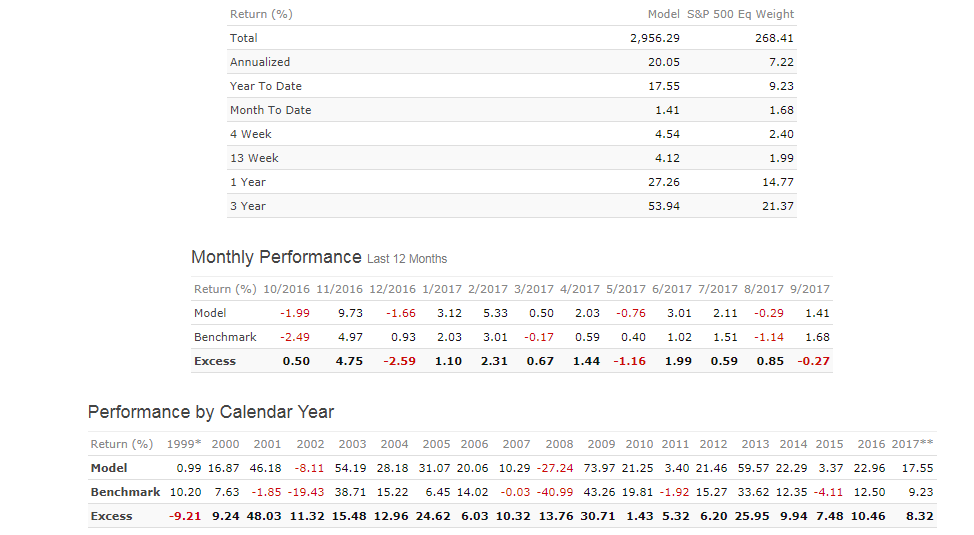

When I first began my journey on P123 as Quantonomics in 2013, I participated in the crafting of eye-popping annualized returns but I realized overtime the audience for these models is very small. I work in the financial industry for more than 10 years and I am currently a portfolio manager at a small boutique firm. I believe it’s impossible for any portfolio management professional to invest in 99% designer models because they don’t meet the necessary requirements of actual investable products. Not because these models cannot generate strong returns (a couple of them do!), but for a myriad of reasons, the main ones coming to my mind are:

1. Scalability / Liquidity

Most cannot be scaled. It is one thing to have $1-5 million invested in a strategy, it is another to have over $100 million + of assets under management and be able to get in / out without moving the stocks.

2. No Market Timing

Market timers embedded in model portfolio strategies are the root of evil because it is difficult for potential investors to dissociate market timing returns from the ranking / fundamental rules returns.

3. Diversified Holdings

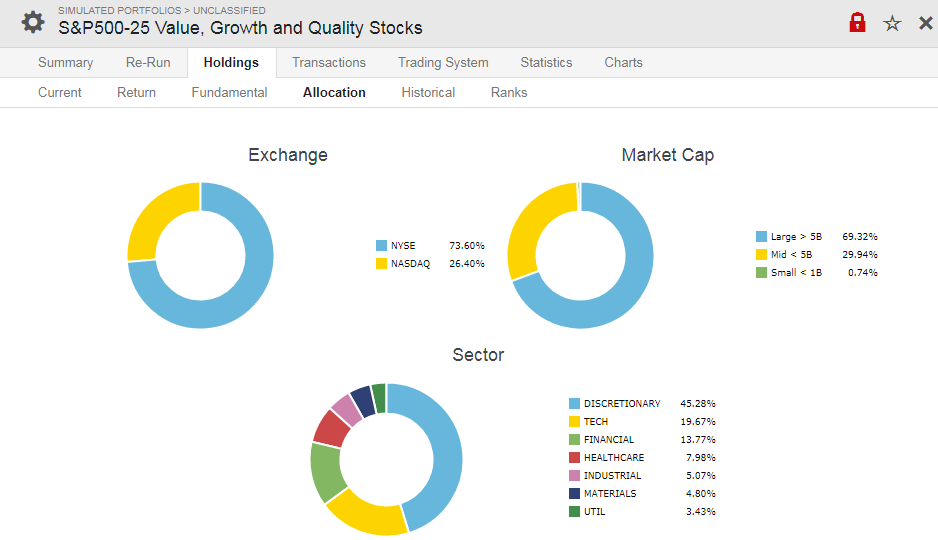

You would be hard pressed to find ETFs, mutual funds, pooled funds, etc. with less than 25 holdings. Most models on P123 are Top 5-10 holdings and would be considered portfolio complements at best.

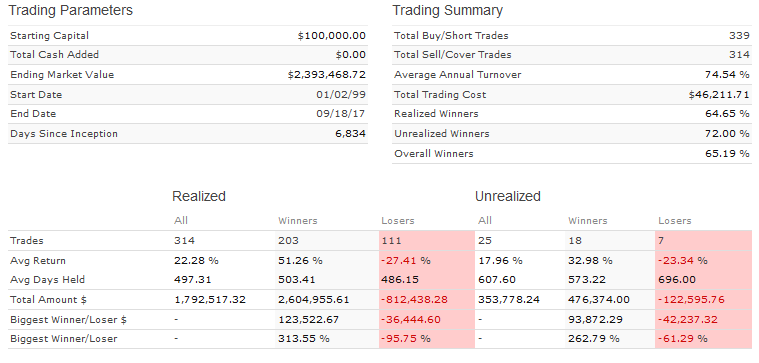

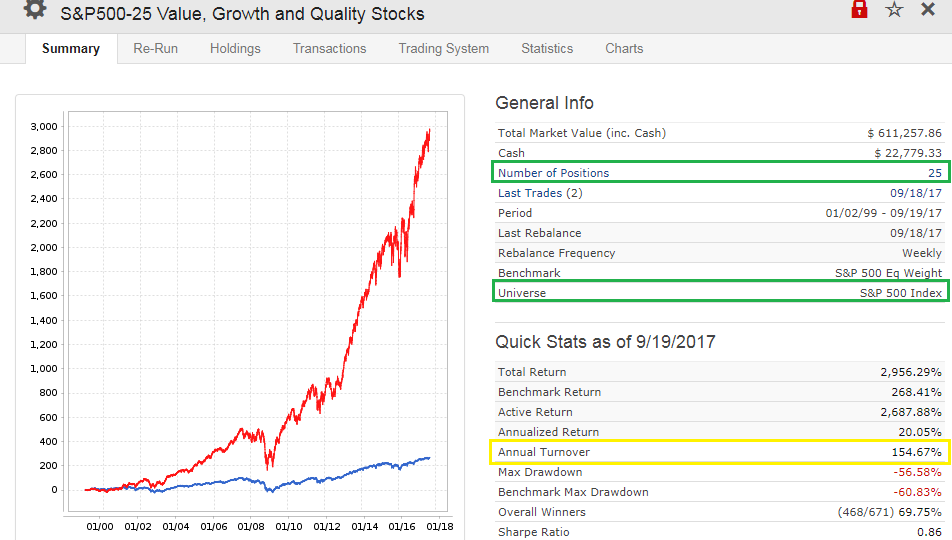

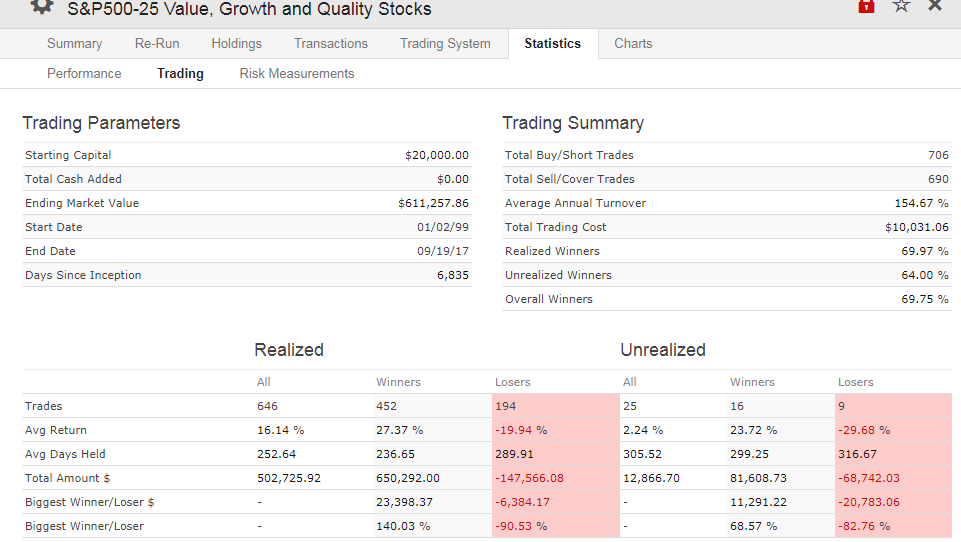

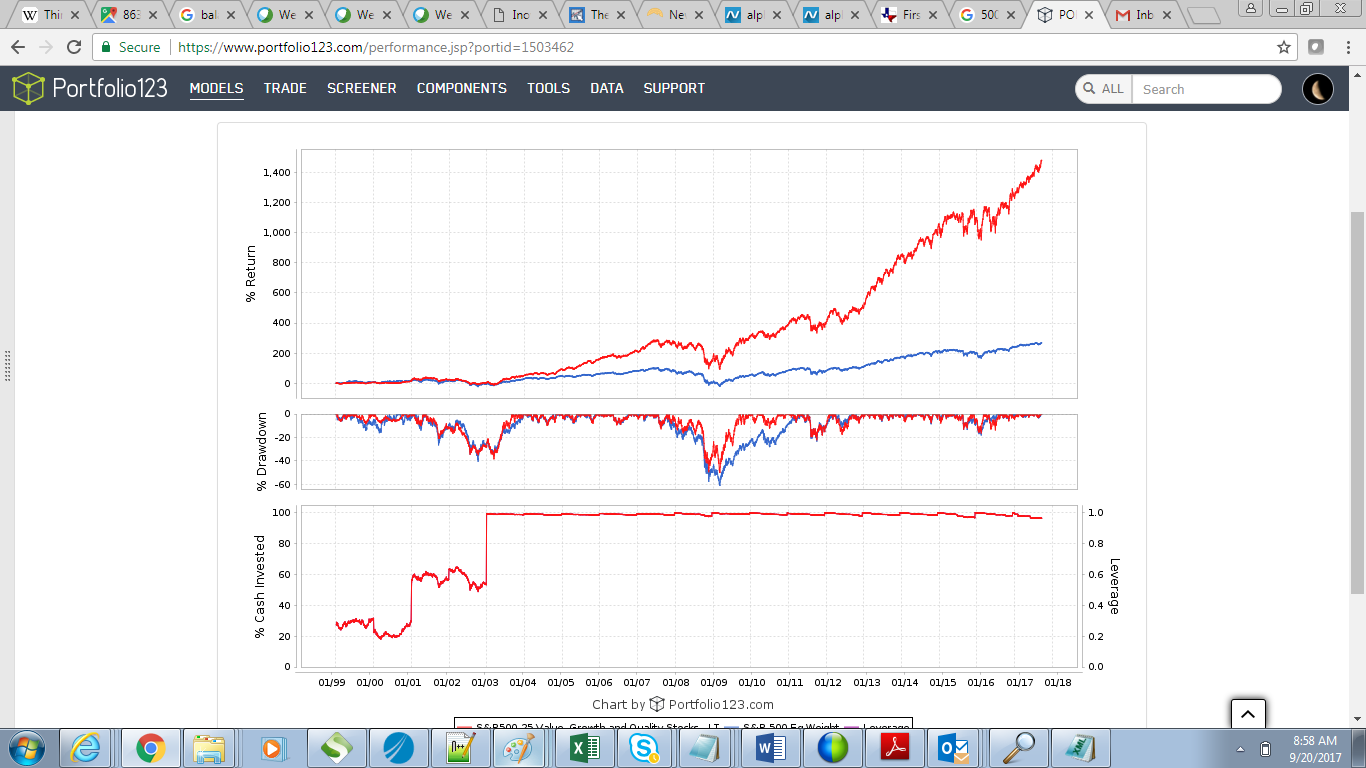

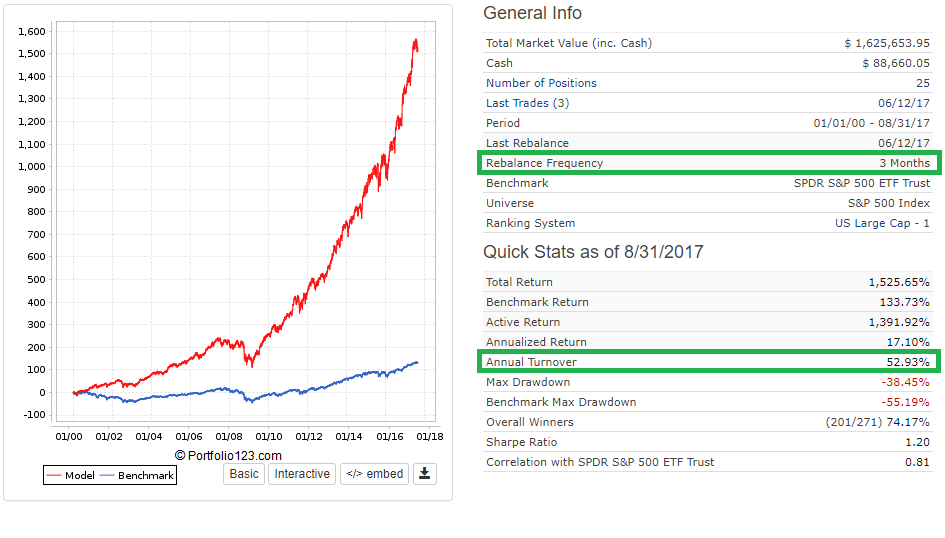

4. Low portfolio Turnover

Low portfolio turnover is below 75%… I often see designers stating “low turnover” at >200%. If you manage money, you aren’t a speed boat that can turn on a dime. You have to think of yourself as a cruise ship.

5. Lack of transparency

Many models are unfortunately black boxes. I can understand the need to protect intellectual property but if one cannot even understand where the returns come from and how they are generated, it is problematic.

So far, I have these three strategies meeting investment advisors / institutional requirements. They are fact sheets but I have detailed presentations available as well for those interested:

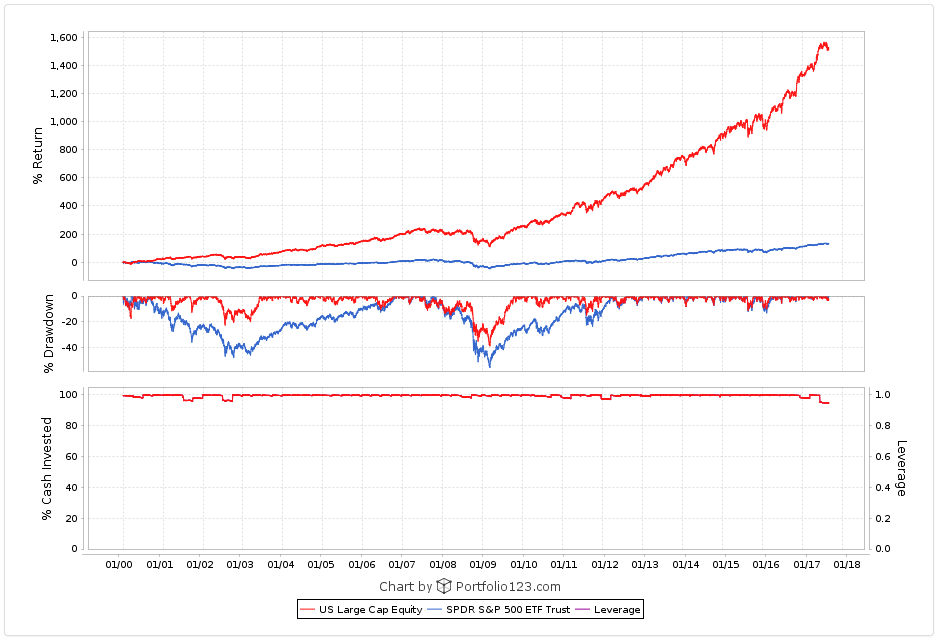

US Large Cap Equity

Inovestor_Factor_Based_US_Large_Cap_Equity_Fact_Sheet_201708.pdf

International Equity

Inovestor_Factor_Based_International_Equity_Fact_Sheet_201708.pdf

Canadian Equity

Inovestor_StockPointer_Canadian_Equity_Fact_Sheet_201708.pdf

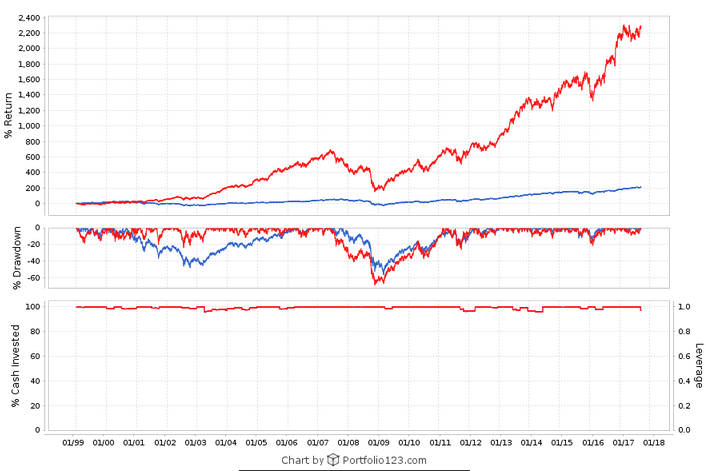

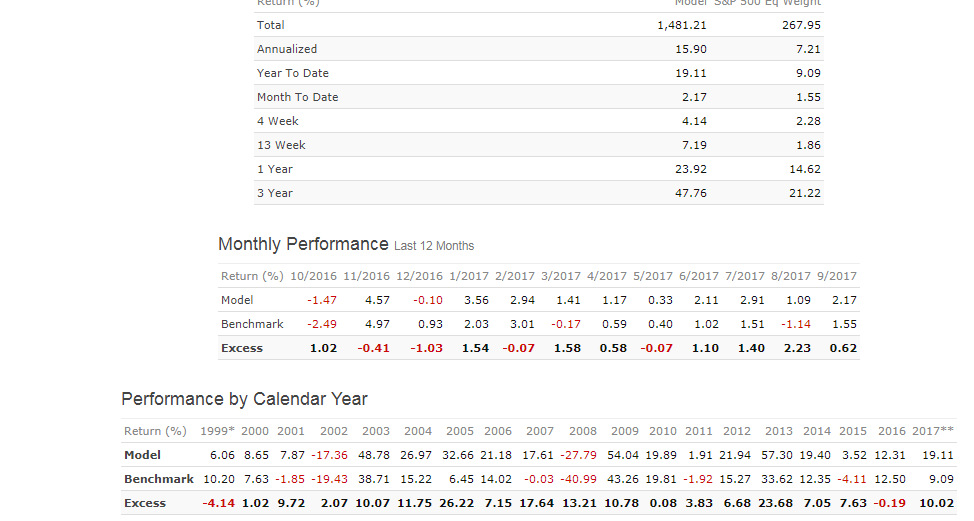

This one has an out of sample track record of almost 10 years! I didn’t create it but I am responsible for it. An interesting fact about this Canadian Equity Strategy is that it was released out of sample during the 2008 bear market without ever having been backtested! Thanks to P123, I was able to finally prototype the model in the first half of this year. An ETF tracking this quantitative strategy should be launched late November 2017 and listed on the Toronto Stock Exchange, I am excited about this ![]() ! I am wondering if other members created model portfolio strategies specifically aimed at investment advisors / institutionals and what results have you achieved?

! I am wondering if other members created model portfolio strategies specifically aimed at investment advisors / institutionals and what results have you achieved?