Really interesting and good explanation of why annual return is not all you should look at, especially for retirement. I really enjoyed this video and he does a great job with the charts.

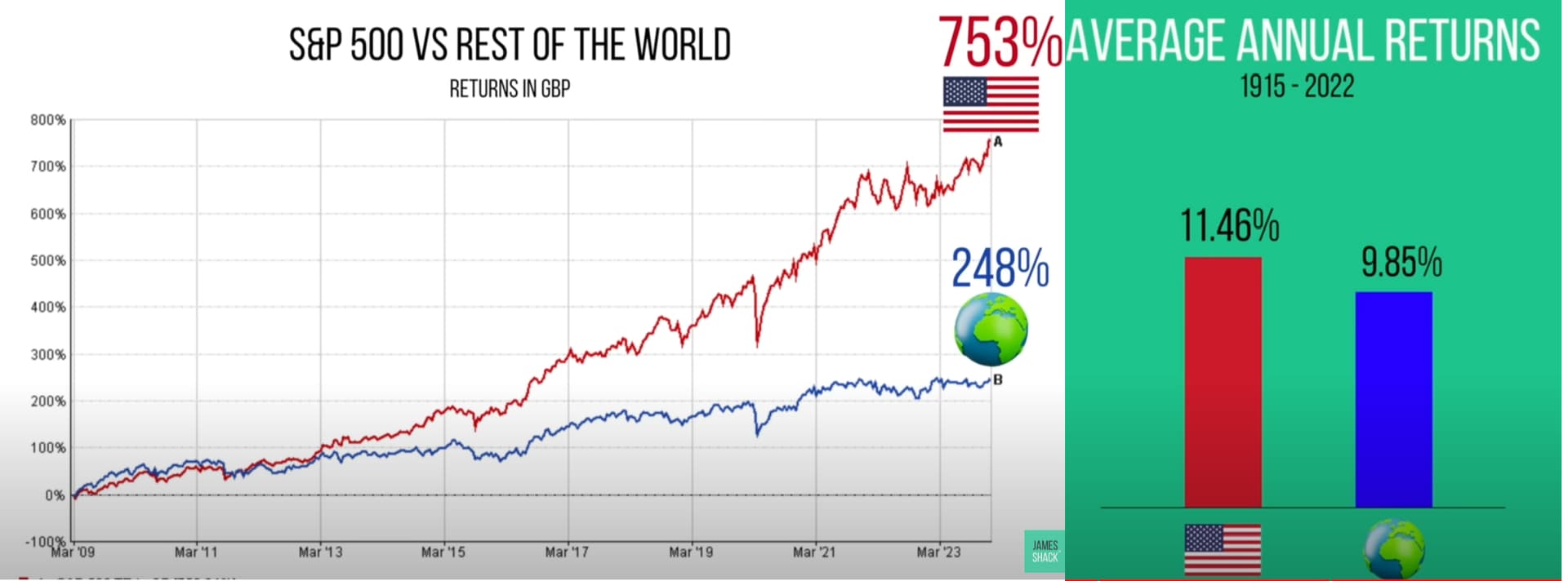

What does it mean for P123? That perhaps adding European data was a smart decision! And that we need to focus on other things instead of just great backtested returns. And produce tools that put more emphasis on stability, rather than just average returns (we started doing this a bit with our new rank performance, and AI factor). Lastly we're starting a Risk Model project to help reduce volatility.

Hope you enjoy.

")

Some screenshots...

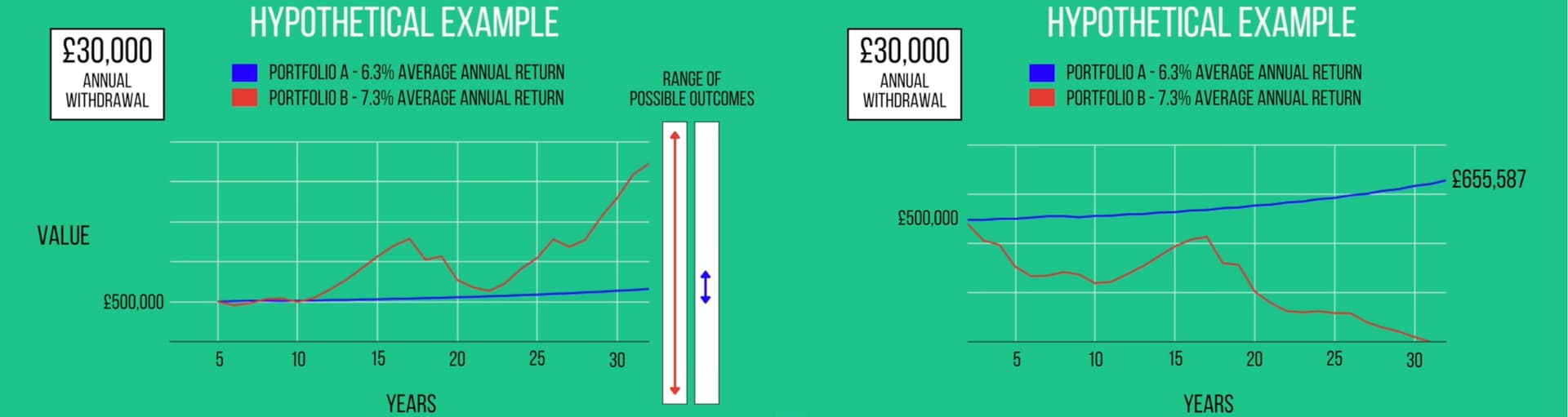

What would you choose?

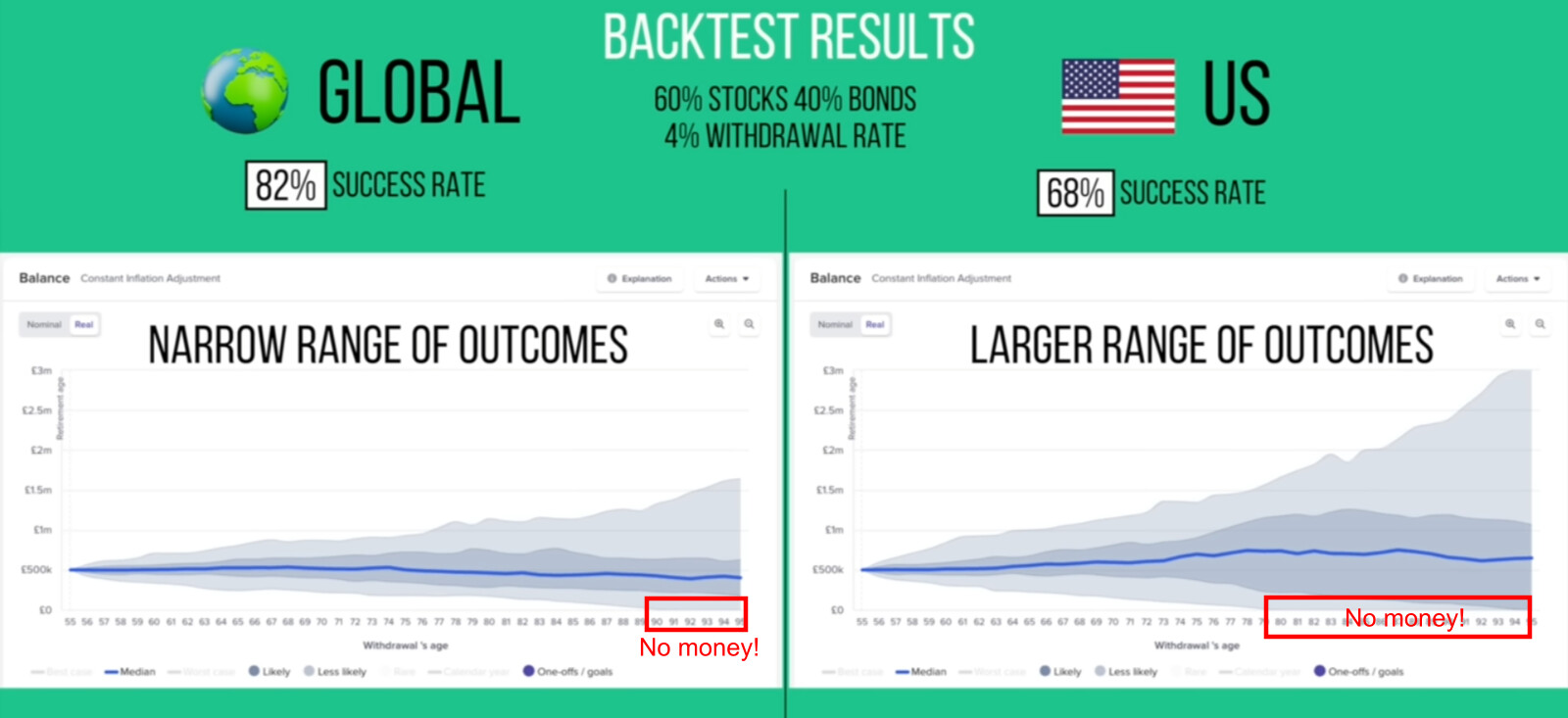

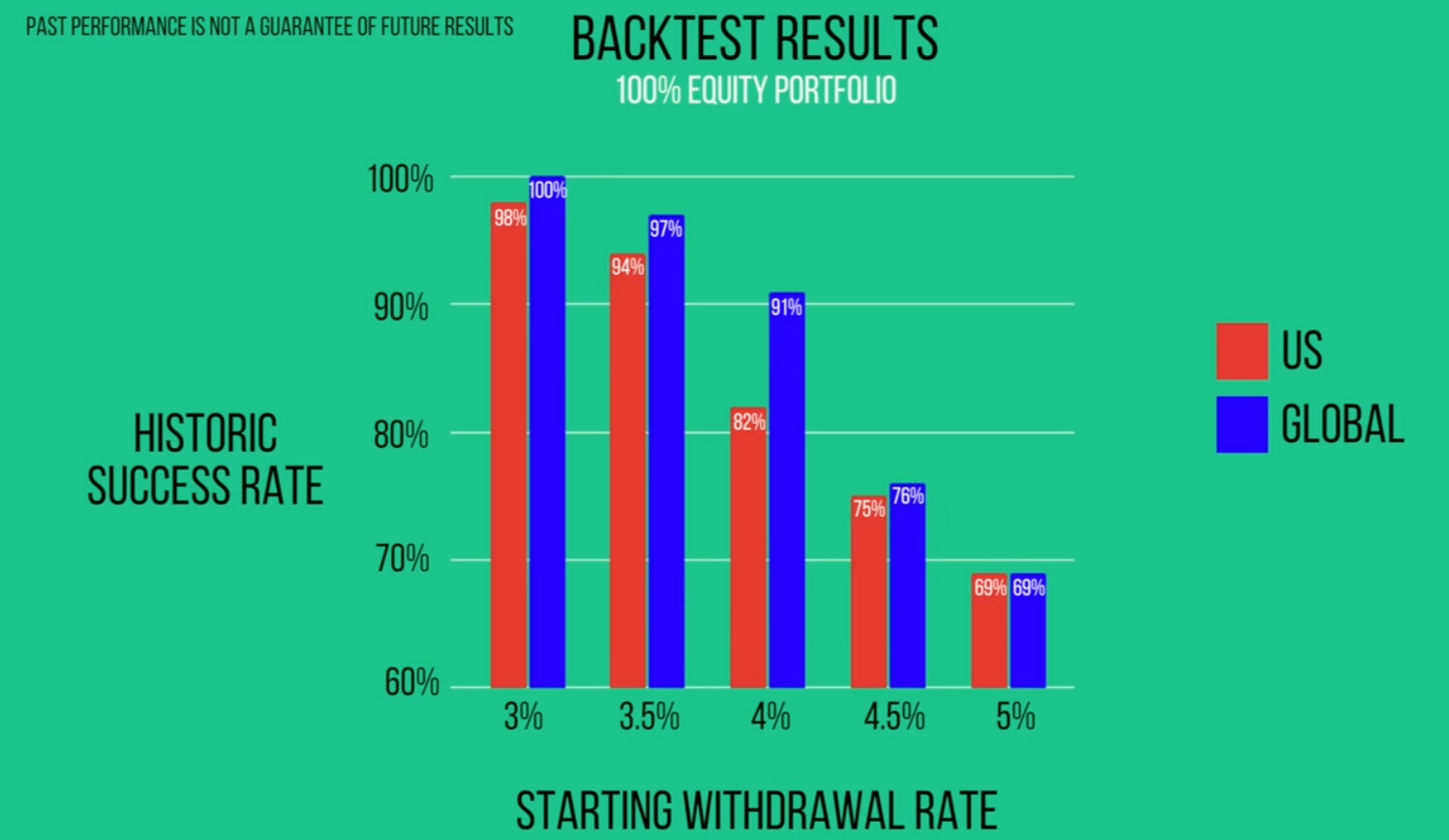

The problem is that when you combine it with an annual withdrawals the SP500 has a much higher change of failure at the 4% withdrawal rate. In other words you'll end up with no money (82% success rate vs 91%)

The problem is volatility of course. If you are lucky in the beginning of retirement, and hit some very good returns with the SP500, you will end up with a lot more money at the end (which you can't take with you). Conversely if you have a string of bad years at the beginning you could run out of money.

Neither is good if your main goal is to enjoy retirement (spend more money every year) with good changes of success.