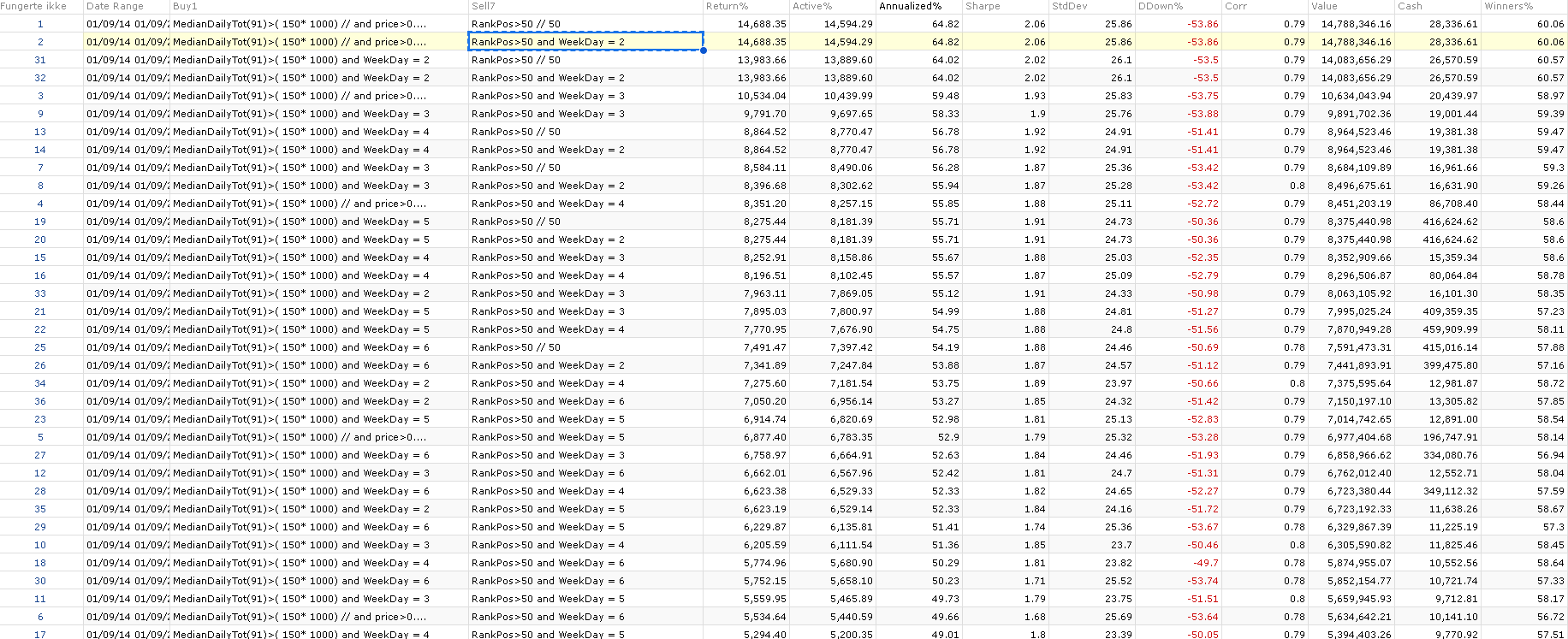

TL;DR: it seems I am doing is better with my style and my ports compared to just rebalancing on Monday each week. By that i mean, rebalancing each day (including Friday) rather than continuing to buy or sell during the week on Monday’s data gives me better returns. I think that is mathematically provable with my ports. And it makes sense that it might work that way as one might rationally consider that more recent data could help at times.

My point is my Friday sim does poorly because it uses Monday’s data for the rebalance (5 day old data) and not Friday’s data. The Monday sim has the advantage of using data that would have been uploaded into P123 the night before.

My Friday sim doing poorly (and my Friday sim does indeed perform poorly) due to that fact that it is using 5-day-old data and has nothing to say about the day-of-the-week-effect. My Friday sim does portly while my port does well.

I only buy and sell on Friday for my Friday live port, yes.

But I also have a Monday port (rebalanced only on Mondays) and Tuesday port (rebalanced on Tuesdays only ) a Wednesday port (rebalanced on Wednesdays only) a Thursdays port (rebalanced only on Thursdays only), I have already discussed my Friday port rebalances.

My Friday live port is nothing like my sim (with regard to holdings or returns). The sim is not an accurate backtest of my port for the reasons In my first post and above in this post.

For me Friday is the best port of all them (while the sim does poorly). One reason that when the AI/ML is full rolled out I would like to be able to rebalance on Fridays easily.

One way to deal with liquidity problems like that would be to run 5 ports that are 1/5th the size of the a larger port that takes several days to rebalance because of liquidity concerns. The five ports would spaced out over the week (a port for each day of the trading week).

Personally, I would finish the rebalance each day by the close. Hopeing the next day would be better (assuming the rebalance the next day even includes that stock after a large price movement that made it difficult tp fill the entire order). But there would be other rational ways to dea with that (none quite as good in my opinion).

Not only is each buy-order 1/5 the size allowing you to move in or out of a position gradually, but you are no longer chasing a stock that had a bad announcement, a change in analysis opinions or had a price change large enough to have a significant effect on the value factors. A large price change would probably affect every value factor wouldn’t it?

BTW, a designer (P123) could run the same port 5 days a week and ethically increase the number of subscribers allowed (without liquidity concerns) by a factor, perhaps, of 3, 4 or even 5.

TL;DR: I think this is an accurate analogy that should simplify this discussion. When making a decision as to whether to enter an intersect it dose not hurt, at least, to have live information on the traffic light (red or green) or the traffic patterns (what other cars are doing). I am not sure how old the information can be to work for me at a traffic light but I suggest there is a limit. A limit for all information really including stock information.

For gaming microsecond latencies are an extremely serious problem addressed by programmers. If the latency reaches a second (for headphones or with another player in a remotet location) the game is useless. If there is some game/theory and high-frequency trading none of this should be anything to not consider seriously. Each port will have its own latency beyond which it is useless.

This is a real problem Apple has accessed with gaming on its computers. Decreasing the latency with AirPods and acknowledging that Beats headphones are seldom adequate for gaming. For casual-gaming a latency of 100 -150 milliseconds is adequate but hardcore games demand better. It was also a consideration in updrading to the Bluetooth 5.0 standard.

Anyway, it is my believe that 5 days is not so good for some stock ports but this is not a new problem. High-frequency traders even put servers next to the exchange using fiber-optics to mitigate the limits of the speed of light (and electric currents).

None of this should be new or controversial to anyone

Jim