I ran several different tests to see what would be best and the effect of using RankPos> vs. rank<. And for some reason, in every test, it was possible to get the same alpha but with a lower turnover. Almost 100% lower turnover in most tests. Why?

I understand that it is smart to use rankpos when there is a lot of variability in the number of stocks in the universe. Rank vs RankPos: Which is better? - #5 by WalterW .

But is there any other reason why I’m seeing this effect?

Hi Whycliffs, I don’t know, but some things to try:

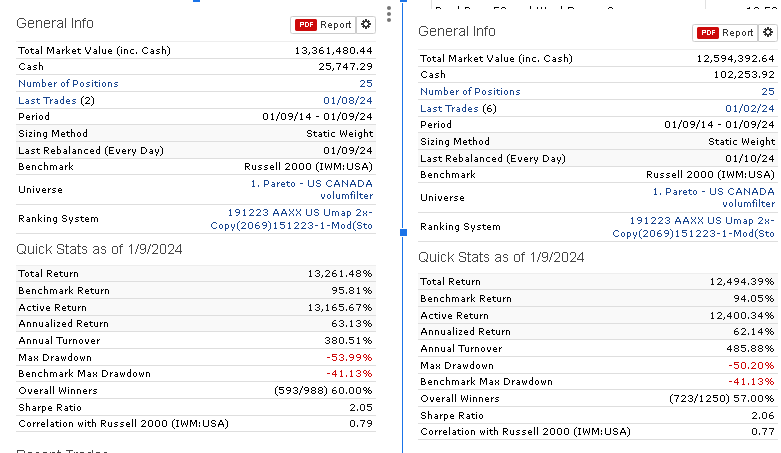

Maybe look at the last trades. Seems like the one on the left traded on 1/08/24 and made 2 trades, while the one on the right traded on 1/02/24 and made 6 trades (trading on different days). Might look at those trades for ideas why it’s picking different stuff with different activity levels.

Also, can’t tell about slippage, but you might set slipppage to 0 and compare them both to see what comparable returns would be absent slippage. Slippage could be the difference in return given different turnover levels.

I think any hurdle rules in your screens could cause differences with rank vs. rank position, so if you have any maybe remove those and see if that might be impacting result. I guess in same vein, check to see if both models are always selecting 25 stocks every single rebalance. (It sounds like that is the expected result, and that all 25 for both models should be expected to be the same? If that’s not the case, perhaps look at when they diverge and why? After that point, butterfly effect can take over).

Let’s say that your universe changes size over time. Rank and RankPos will act very differently. Rank will always give you the same percentage of stocks in your universe while RankPos will always give you the same number of stocks. A sell rule based on Rank and a sell rule based on RankPos will give you very different results.