Marchus posted this in another thread. To the extent one might want to hold bonds I agree:

James (ustonapc) had made me aware that one can get some leverage of inflation protected bonds through the ETF UPAR. Link: UPAR

In addition, one might get some advantage from: “longer duration to take advantage of higher yields and ability to “roll down” the yield curve” with this ETF.

This will come with leverage of other asset classes which may be good or bad for each P123 members’ individual investing style.

There has been some interest in correlation of securities and purchasing diverse asset classes recently. This ETF could be combined with other ETFs to provide a desired mix of asset classes with some leverage–especially if you invest using an IRA account that does not allow margin.

James has an extremely high level of awareness of professional investing methods and his ideas are extremely welcome in this forum.

I have used a modest weighting of RPAR as part of a diverse portfolio and I switched all of my RPAR to UPAR when you made me aware of UPAR’s existence.

Have you compared rpar to what you can do using portfoliovisualizer? Leveraged treasuries have the potential to take quite a hit if interest rates continue to increase so have you considered including/excluding them based on momentum or another indicator? Why do you trust using this etf long term without out of sample returns?

I like using phdg as an alternative diversifier. I hold it when it’s warranted but it would be a reasonable choice for a long term hold.

I am not sure that James is actually investing in RPAR or UPAR so I am speaking entirely for myself. James may agree or disagree on any specific idea of mine.

As for as out-of-sample results, James made me aware of RPAR when it became available because of its similarity to Ray Dalio’s All-Weather strategies. James was aware that I follow some of Ray Dalio’s ideas. In fact, I believe that many of the people at RPAR are former employee’s of Ray Dalio’s Bridgewater Associates.

RPAR has some out of sample results but underperforms–probably one of the reasons that they now have UPAR as a leveraged alternative. They advertise it as possibly giving better returns than SPY with the same volatility. Obviously I am skeptical that it will perform exactly as advertised. Who knows? Certainly not me.

But truly this is just a part of my portfolio to get leveraged TIPS. One can mix any ETFs they want (some also leveraged perhaps) to get the mix they want.

Like you have said before, I think, TLT may not be the best bond fund to hold. TIPS, or leveraged TIPS may be better. They do better in inflationary environments, obviously. The are also considered less interest rate sensitive, although this is probably only because interest rates usually rise in inflationary environments.

As far as Portfolio Visualizer, I do use it. It is always possible to find a backtest that looks good. I do not have enough out-of-sample results to show you anything meaningful there.

BTW, if you are interested in leveraged intermediate-term bond funds that can be found as part of NTSX which is a Wisdom Tree ETF.

I am not married to any one idea. Just to the idea of using multiple ETFs to get the overall mix of assets I desire. UPAR is just an idea for one way to get exposure to leveraged TIPS for anyone who may be interested. The desired mix of assets after combining multiple ETFs would be different for everyone, I imagine.

Why not just hold 50%TIP + 50%SPY?

This combo performed better than RPAR since its inception.

RPAR is actively managed. As stated in the SA article posted by Scott RPAR’s managers had made some temporary modifications to the fund’s asset class weights, which had both increased risks and decreased returns. There is no guarantee that the manager will not mess up again.

Second what about being a modest portion of multiple ETFs did you not get?

Also read Scott’s and Marchus’ ideas about TLT in the present interest rate environment. While it remains to be seen how TIPS may do, for TLT the following applies: Past performance may not predict future returns.

Hense, I do not immediately switch into the best backtest I can overfit.

Also, please reread Yuval’s posts about cherry-picking and overfitting. As well as some of Marc Gerstein’s ideas on the subject.

For a classic 60/40 bond mix with leverage one can also look at NTSX. The advantage here would be that NTSX uses intermediate-term bonds that may be less interest rate sensitive. [color=firebrick]And because of the leverage one can diversify with other assets (e.g., GLD) without reducing the portion of the portfolio in stocks. [/color] But again, past results may not predict future returns and I hold no NTSX.

Everyone will have their own opinion about bond funds and which bond fund to use (if any at all). Notice I have made no recommendations here nor have I even said what portion of my portfolio is made up of bond funds. That would be for each member to decide.

BTW, at the end of the day my mix can have other bond funds in it (through my adaptive allocation portion of my portfolio). [color=firebrick]I am not against other bond funds. In fact, I hold other bond funds at times.[/color]

It is not a backtesting competition as you well know, James.

This is a comparison of the different ETFs (UPAR is excluded due to the lack of history) that has been mentioned in this thread. As Jim points out, past results may not predict future returns. Before investing, the standard deviation (risk) of the different ETFS should also be a consideration.

Thank you. Any P123 member may want to own any, all, or none of these (with or without timing) depending on their strategy and perception of the interest rate environment (as well as the economy as a whole).

It is just an idea that would not even rise to the level of a suggestion.

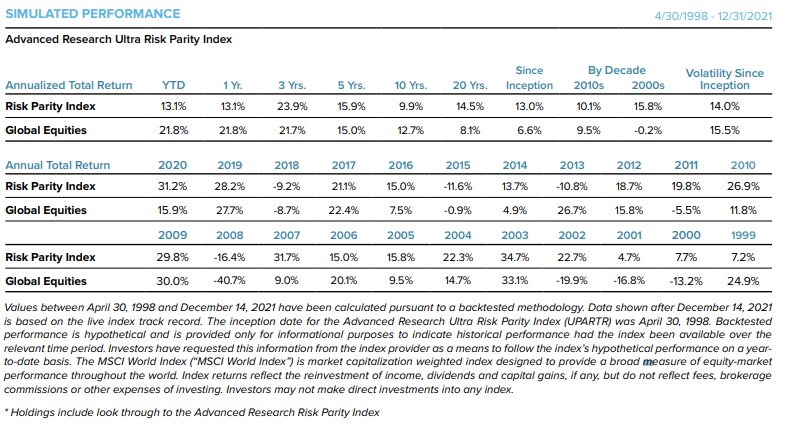

They do have an “index.” And indeed it is probably better called a backtest than an index.

I did not find the index very decipherable when I first looked at it and kind of did a back-of-the-envelope calculation of 15% CAGR (which you confirm).

Thank you for the more detailed analysis of the 'index" or backtest. That is good information.

I am more intrigued by the theory. It is LIKE modern portfolio theory (MPT) but not over-reliant on recent historical data. It takes advantage of the lack of correlation of the assets but is not using the “tangency line” calculated from historical data as simple MPT might do. Therefore, the correlations are probably more persistent through different macro environments.

Ray Dalio (who runs the largest hedge fund in the world) has tested this strategy in a huge number of macro situations. For example, after World War II when there was inflation and bond yields were kept artificially low. Some have said we are in a similar situation now.

Theoretically 2 (of the 4) holding classes should be correlation while there is an inverse correlation of the other 2 in most situations. With leverage this can produce stable constant returns.

I mention the link here because they do discuss how the strategy is not so good with zero interest bonds. Perhaps bonds are not at zero interest now but each person has their own idea about bonds and interest rates. The link discusses some of this with less spin than many links. They are talking to a huge number of large institutions (maybe more institutions than any other fund in the universe) thru this link and too much BS would not be appreciated.

But the most important thing to me is the I have not always stuck with this asset mix nor do I necessarily recommend it to anyone. People may (probably do) have different ideas about bonds and commodities than I do. With a little high school algebra one can mix this with other assets to get whatever asset mix they desire and take advance of the leverage–including the leveraged TIPS but also commodities and stocks if they want. I have added small-cap ports to the mix in the past.