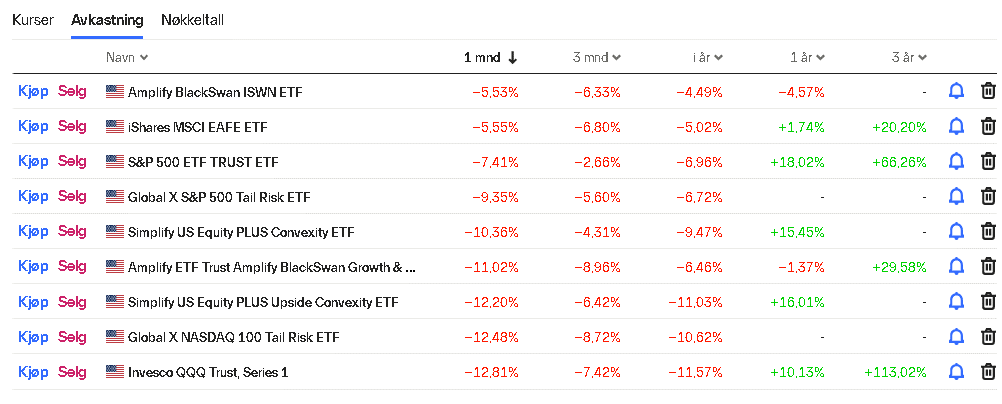

I examined the Tailrisk or hedge etf. I’m astonished at how poorly the actual have performed in this correction. It may appear that none of them work properly until there is a correction in marked at 30-50 percent, at which point you pay a very high price for something that rarely works.

That is very interesting… a few years ago I did a lot of digging into the Tail Risk Hedging space and could never come up with a strategy that paid for itself, although I figured someone smarter than me might could do it.

I wonder if this particular drawdown is causing problems because for these funds because it is driven by inflation concerns rather than deflation concerns and we haven’t seen the typical move higher in Treasuries. Of course I am sure they would argue that a 10% drawdown isn’t really a left tail event.

Marchus,

Thank you for posting this. I was unfamiliar with many of these funds. And I guess I agree 100% as far as the discussion has gone so far.

But perhaps the discussion can be extended in 2 areas. First, is it always the case that these funds are supposed to be used in isolation?

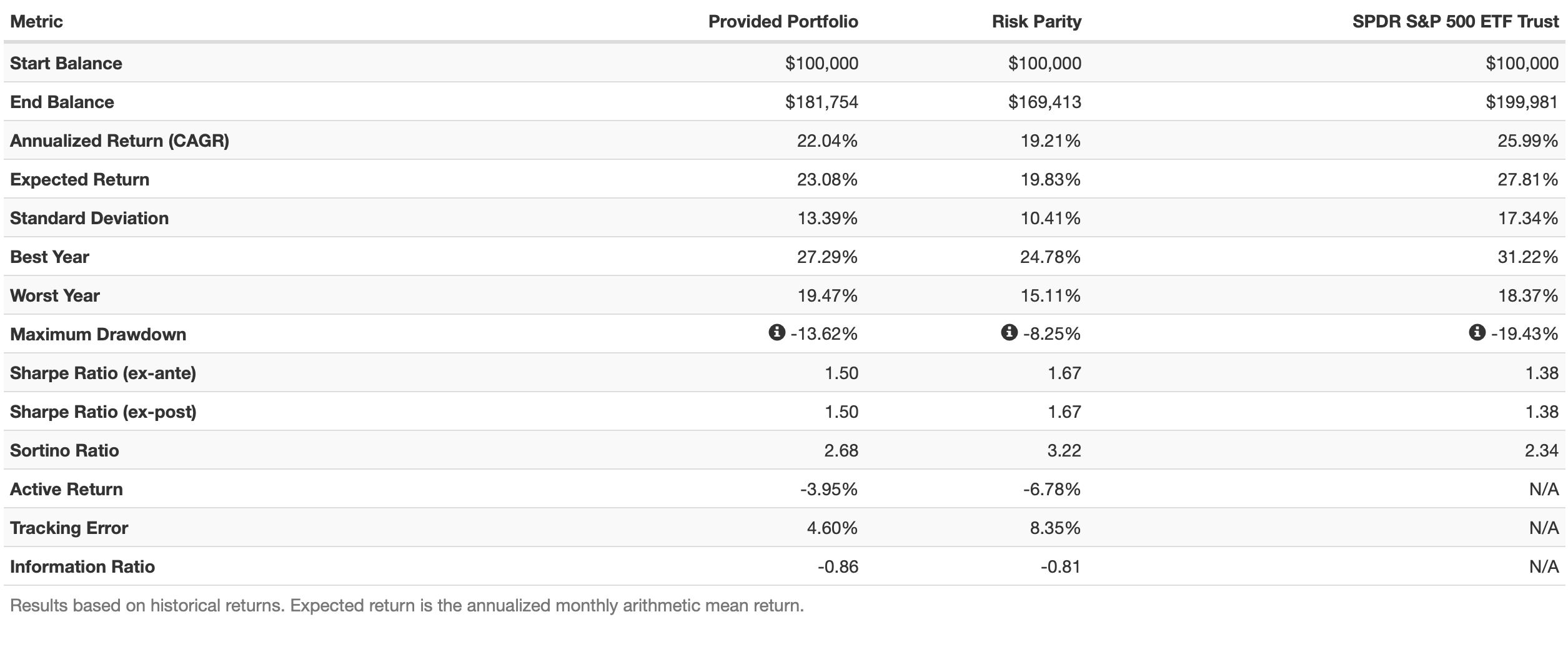

As an example of why I ask, here are the risk metrics for VTI/SWAN in a 60/40 ratio (“Provide Portfolio”). Also VTI and SWAN with risk parity.

Either mix (60/40 or risk parity) does increase the Sharpe ratio and reduces the drawdown compared to SPY which may accomplish some people’s goals. Unfortunately SWAN has not been around long.

But second, that is just the beginning of the discussion isn’t it? Markowitz was basically always discussing the use of leverage or holding some cash equivalents (at the risk free rate).

My only point is that by combining ETFS and/or finding ways to use leverage (sometimes using ETFs that already have leverage) this could still be useful for some members.

Also whatever I might imply with any short backtest of mine, the recent market is just weird (e.g., distorted by the FED interventions) and cannot be expected to continue. SPY (the benchmark) will not have a Sharpe ratio of 1.38 forever going forward, for example. It is not clear to me what impact this may have in the future if we revisit this discussion.

Much appreciated!

Jim

I’ve read a lot of literature including a couple books on Tail Risk Hedging. In my reading Ive looked at several case studies. Tail risk strategies which are based purely on options based far out of the money puts with deltas of 1 (out of 100) or less can pay handsomely during market crashes. But the rest of the time they are just dragging on your portfolio. You really need to be dedicating 5% or more of your portfolio to see a benefit in high volatility scenarios and that’s where they really drag on your portfolio. To make them work in your favor you have to employ to buy them during low volatility and take profits during high volatility which requires some market timing.

I made some money off tail risk hedges during covid crash, but I’m not sure I would buy them again. They blunted my losses at that point in time but the portfolio drag is irritating. I’d rather just take the good volatility with the bad.