So I have been consulting with a short-only fund for the past few years and I wanted to share a simple insight I learned along the way.

For shorting stocks there are basically 3 regimes.

- Calm and rational markets.

- Volatile and fearful markets.

- Volatile and greedy markets.

Shorting high risky stocks works well in calm and rational markets where discerning investors care about separating good stocks from bad. Shorting risky stocks works very well in crashing fearful markets. But you will get murdered if you short risky stocks on the rebound in greedy markets. It will wipe you out. Just think about what happens when a risky stock which has fallen from $100 to $10 and then the market bottoms and goes back up…if you short at $10 and it goes to $30…kiss your portfolio goodbye. In greedy markets you want to short low volatility (if you short at all).

Now this isn’t perfect but it is a very simple method to identify all three regimes with just the VIX.

- VIX less than 20 is rational markets (short risky assets)

- VIX is above 20 and it is also 10 points higher than it was 20 days ago (short risky assets)

- VIX is above 20 but is less than the VIX 20 days ago + 10 points (the elevated VIX is declining such as a market bottom and a new rally. Short low volatility if at all)

So as a proxy for risky stocks we will use SPHB.

As a proxy for low risk stocks we use USMV.

The short is set at 50% because the beta of the short (when it is SPHB) is so high and the low volatility ETF (USMV) is much lower. We want to balance out the beta risk.

In condition 1 and 2 we long USMV and short SPHB at 50%.

If condition 3 we long SPHB for the rebound and short USMV at 50%.

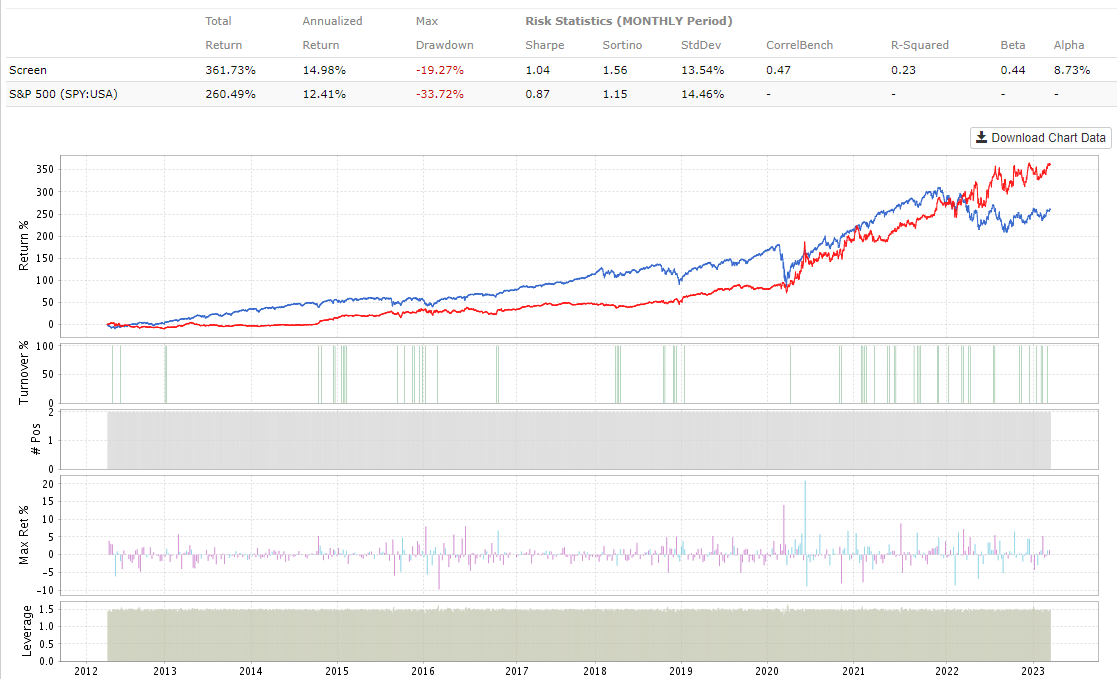

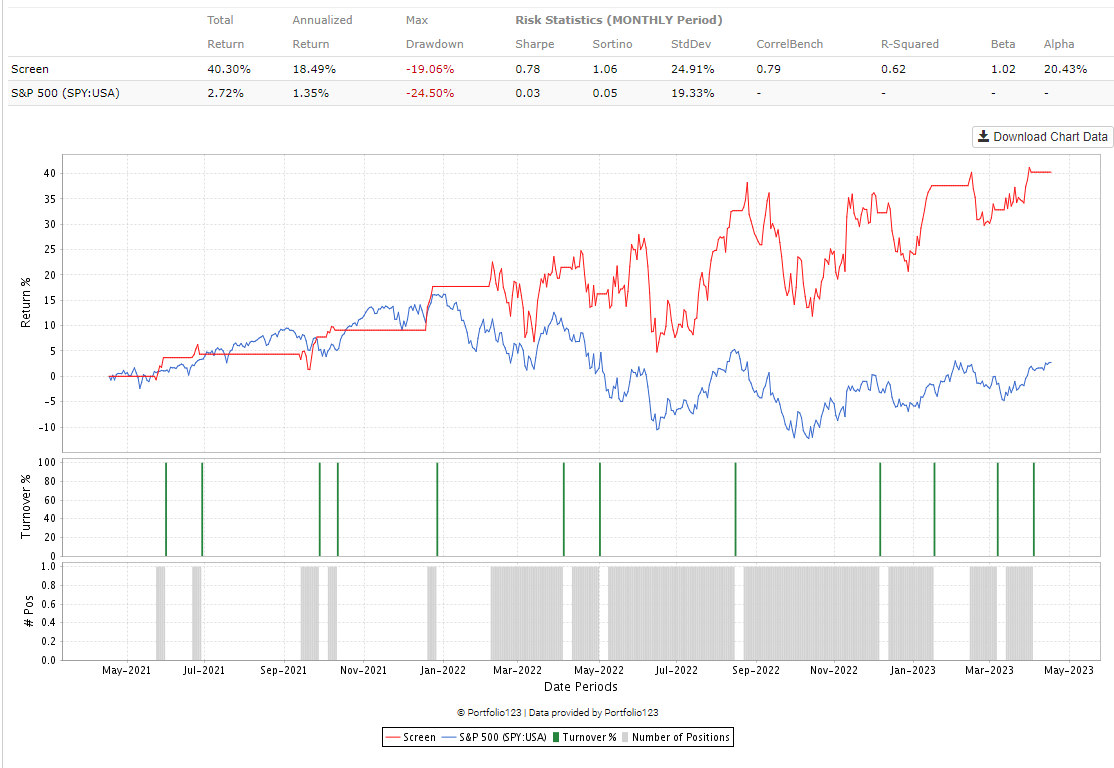

It is a simple screen I will make public. You can do so much more and better things with it. But for a rudimentary system with 2 ETFs…it’s not too bad.

https://www.portfolio123.com/app/screen/summary/281737?st=0&mt=9