Hi, I was wondering if anyone here has attempted a long / short hedging type strategy and can give feedback/thoughts/suggestions on the practicality of implementing such a system for a small investor going long/short in a universe of large, widely held, liquid companies. The idea being to build a strategy to tilt a bit toward market neutral and capture a spread between top/bottom deciles similar to what is seen in academic papers.

Comments and discussions I’ve read elsewhere seem to strongly discourage that approach from a real-world, practical standpoint.

I’ve only shorted a handful of times in my life, and in those cases I don’t recall difficulty or high expenses with the process, but my experience is extremely limited and I’m sure there are pitfalls.

There are some securities with very high borrow rates (I got paid quite a bit when some hard-to-borrow shares were borrowed from me within the past year or two) but I’m wondering if those cases can be safely avoided by focusing only on widely held, liquid securities? Maybe this assumption is incorrect?

Any thoughts or comments on market neutral approaches are appreciated. I know so little about this that almost any perspective is more valuable than my own thanks in advance,

Select a brokerage carefully. Not all are created equal when it comes to shorting stocks. Avoid brokerages such as IB that use third-parties for implementation of short positions.

Quant factors tend to flip on their heads for periods of time. This can be quite painful because making up for a loss is difficult when long/short. Note that FTLS only goes short up to 50%, long 80-100%, and is discretionary i.e. managers actively decide the holdings so historical performance is somewhat meaningless. FTLS isn’t a horse I’d be betting on (just a gut feel).

I would recommend an equity hedged strategy instead using index futures or index, size and sector ETFs instead. Going long “good” factor and short “weak” factor stocks effectively doubles the risk in selected times when factor performance goes against you. And that is actually the time when you want to be hedged and not being hit double.

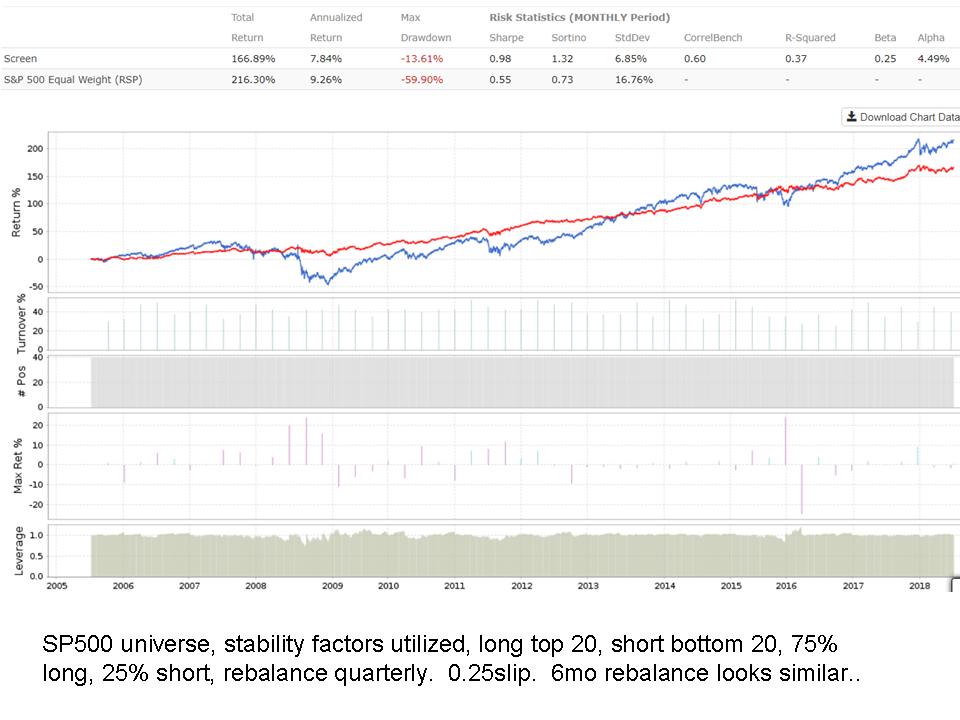

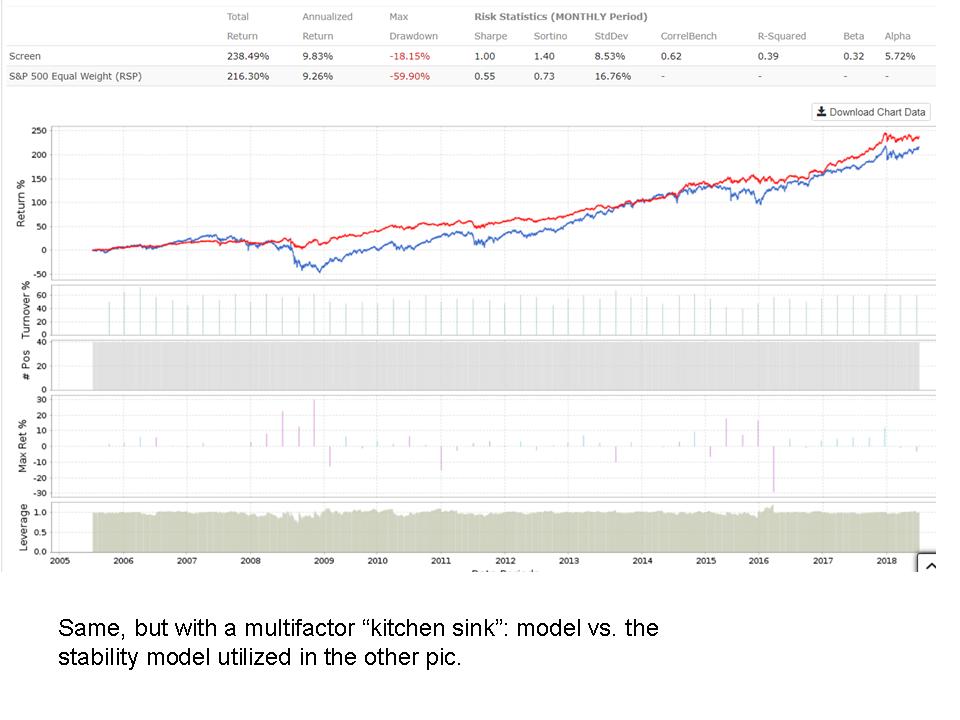

Hi thanks for the replies. I’m just playing around with the idea, but here’s the first simple long/short model I was working with when I first made the post. It’s 75% long 25% short, SP500 universe, ranked based upon fundamental business stability measures (1st pic below). It takes the top 20 ranks and goes long, and the bottom 20 ranks and goes short. 0.25 slippage is assumed. In the second pic I change ranking system to a kitchen sink multi-factor model for comparison.

The results are intriguing to me - I like the characteristics of the equity curves - but when I compare to long/short etf out there, they don’t seem to perform similarly. Some like FTLS or DYLS seem to be about as volatile as SP500.

I guess why I’m thinking about this: I can envision a scenario where I would expect a) bonds to not perform so well along in a rising rates environment, and b) compression of equity earnings multiples due to those same higher rates. So what would I do if both bonds and stocks fall at same time? It seems like some type of long/short hedged equity strategy might be able to serve as a stabilizer with possible positive return in a time period when nothing else might be working. I’m totally just thinking out loud on this, but can see the appeal to these type of strategies if they can be implemented in such an environment.

@StockMarketStudent: Thanks you for the comment. Have you encountered issues with IB when shorting (SP500 companies), or are you cautioning primarily about borrowing fees due to 3rd party? I do use IB as a broker. Would maybe Fidelity or Schwab likely be better for this? (Sorry for my dumb questions - I’m just ignorant on this - I don’t know what I don’t know. I had my accounts with Scottrade for the longest time and I don’t recall charges when I shorted a few times with them (big companies)- so not sure what I should expect.)

@whotookmynickname: “using index futures or index, size and sector ETFs instead.” thanks. I’ll have to look into that. If I’m understanding correctly you’re suggesting hedging with more volatile indexes - like small cap, or more volatile sector etf.

“Have you encountered issues with IB when shorting (SP500 companies), or are you cautioning primarily about borrowing fees due to 3rd party? I do use IB as a broker.”

There are two costs involved. One is simply the interest rate for borrowing money on a margin account. The second is the cost of borrowing a stock. I have used TD Waterhouse in the past. In discussions with other P123 members several years ago, it appeared to be the case that IB was good for margin account interest rate, better than TD Waterhouse. But TD Waterhouse had no additional costs for shorting stocks. IB did have additional costs and they were substantial, at least 10%-20% depending on the security being shorted.

Your equity curves look great but are they achievable in practice? What turnover and slippage do you expect? Are the stocks LargeCaps or MicroCaps? How much over-optimization is involved with your systems?

Thanks for pointing this out. I’ll have to check on this. Thanks for mentioning because that would be different from what I’ve experienced previously. But when I shorted previously I always kept cash in the account sufficient to cover the short position also - so that might be contributor also.

Good questions. What you ask is what I’m trying to understand. If it was achievable I would expect to see something like this in the market - although maybe it doesn’t scale well and big expense ratios on long/short etfs kindof defeat the purpose. Maybe it’s just not doable. I’d think there’s be etf demand for something like this if it’s available somewhere though.

The model is built on SP500, quarterly turnover, using 0.25pp slippage. Carry cost was the p123 default of 1.5. 75% long, 25% short - so leverage mostly stays around 1.0 ratio. I might need to put on some small shorts on sp500 stocks for a month to see how much it costs me. In my experience most SP500 stocks I’ve encountered tend to be easy to get into/out of with low slippage, but there are many on the short side of model that I’ve never encountered before.

I don’t know about overoptimization. Always possible. The models weren’t developed with this long/short use intended. I grabbed the fundamental stability model off the shelf because it seemed appropriate for smoothing out the bumps like I was wanting to do . The second multi-factor model was a kitchen sink model that tends to work better on large caps than my small cap models, so I grabbed it for this comparison also. But all of this is just a first cut - I was just surprised at what I was seeing initially - trying to understand what i’m missing.

My unsolicited advice is that you model out what kind of a drawdown would take your account to $0 due to margin call when you are short various amounts (which can happen even if your total leverage is <= 1.0). Then ask yourself how sure you are that you won’t ever encounter that kind of drawdown, and if the proposed benefits of the long/short model are worth that risk. Remember that risk never disappears, it transforms - so you are removing market risk, sure, but you are significantly increasing your exposure to the risk that whatever model you are using is wrong, and doing so in such a way that being wrong can kill you.

Should you still want to do this, my limited experience looking into it suggested that the stocks which were quantitatively the best short candidates were also the ones with the highest borrowing fees (not a surprising result).

I agree with Matt. Using a dedicated short component may actually increase your risk while mitigating market risk. But sometimes not even in a falling market “low quality/junk” short positions may work as everyone is cutting back exposure due to rising volatility, meaning borrow rates may increase (because holder may sell) and shorted stocks are bought back. Even worse, coming out of a correction, those junk stocks may snap back with a huge beta (2-4), destroying all your (potentially lower beta long stock 0.7-1) performance.

My strong advice: stick with some simple market and sector hedges, and generally, keep your portfolio slightly long-biased (especially adjusted for beta).