Related to my previous post, is there a way to easily find the total return for an equal weighted universe/screen of stocks without any rebalancing?

i.e. if you bought all stocks in the S&P500 on 01 Jan 1999 (or any date) equal weight, what would your CAGR be today without any rebalance. Of course would also take into the account stocks that went bankrupt/delisted/aquired along the way.

If you never rebalance, then it’s only “equal-weighted” on the day the portfolio opens. After that it’s weighted by performance since open. Rebalancing returns it to equal weighted.

If you set the number of stocks in a screen to 0, so that it includes all of the stocks, and then set slippage and carry cost to 0, then you can choose how often you rebalance to equal and see the AR for holding the whole universe.

This buys the S&P 500 at equal weight on June 1, 2009 (no reason to choose this date, just off the top of my head) and holds through today with no rebalancing. If you change the starting date, change the buy rule to be within 52 weeks of the starting date.

Great, that’s what I’m after. Unfortunately my membership is capped at 100 positions for sims.

Is there anyway to get a version of this sim to work on my profile (>100 positions)? I typically run much fewer positions than 100, this is only for some research I’m doing.

Agreed and thanks, but I’m curious what a true “buy and hold” performance would look like, with no-rebalancing. Over time several positions will fall back (bankruptcy, delisting, acquisitions etc), while others will become multi-baggers.

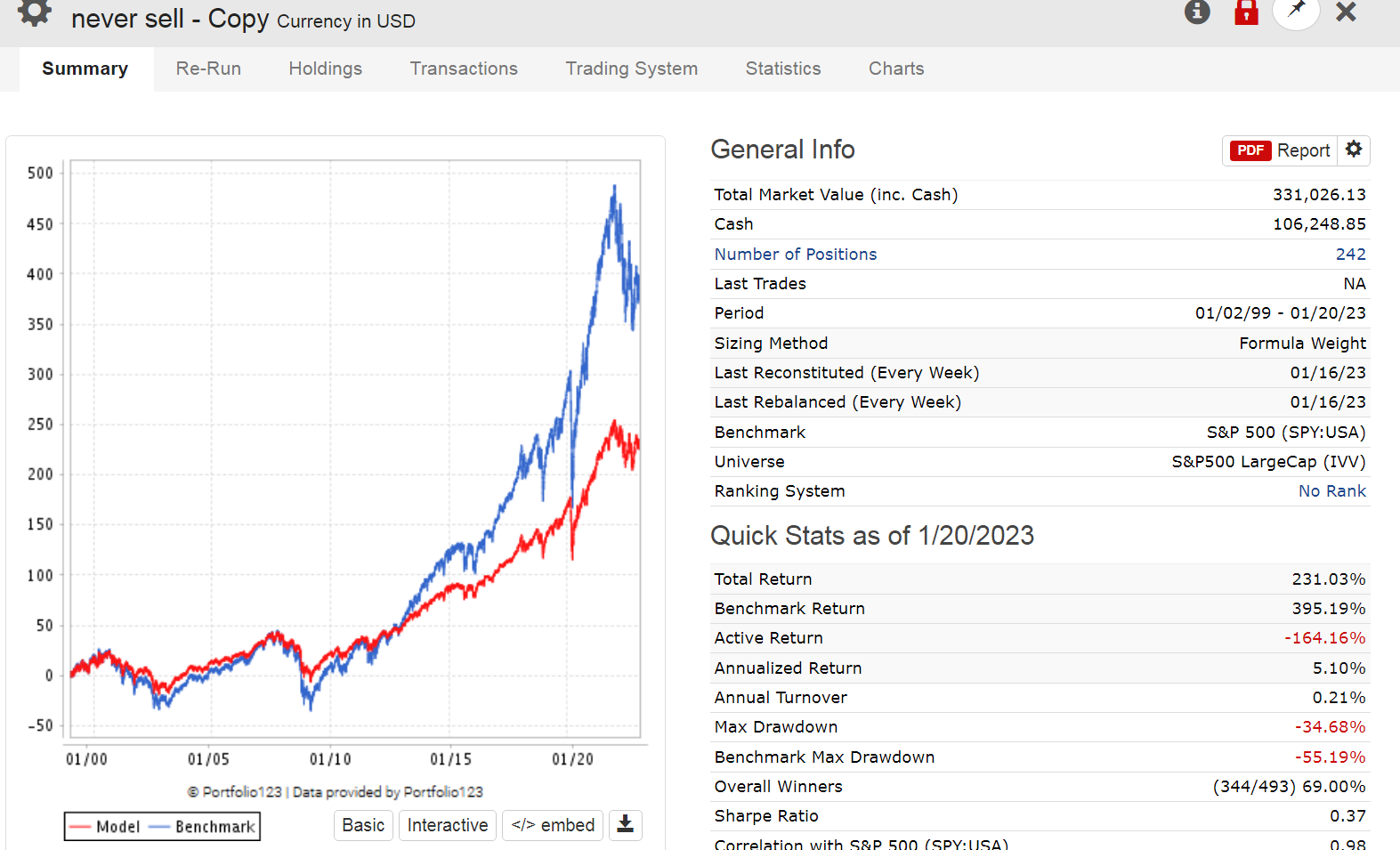

For a simulation (not screen) settings for S&P 500 are:

Sizing Method Formula Weight : 500 positions

Reconstitution = every week

Rebalancing = every week

Position Weight Formula = MktCap

Min Rebalance Transaction = 100%

Period = 1/2/1999 to 1/20/2023

Buy1 = AsOfDate < 19990108 (If you change the starting date, change the buy rule to be within 1 week of the starting date for 1 week rebalancing.)

Result:

Current holdings = 242

Because dividends are not re-invested Cash is about 1/3 of Market Value.

You could run this simulation with an additional buy rule, Between(FOrder(“MktCap”),1,100) and a position size of 1%. Then run it again with the buy rule Between(FOrder(“MktCap”),101,200) and so on. Then make a book out of those 5 simulations.