I’M trying to create some different universes, but want to have a minimum volume, and use this: MedianDailyTot(120) >( 70* 1000)

…and contained to markets where I can trade: ExchCountry(“nor”) or ExchCountry(“swe”) or ExchCountry(“FIN”) or ExchCountry(“DNK”) OR ExchCountry(“DEU”) or ExchCountry(“nld”) or ExchCountry(“bel”) OR ExchCountry(“fra”) or ExchCountry(“ita”) or ExchCountry(“ESP”)

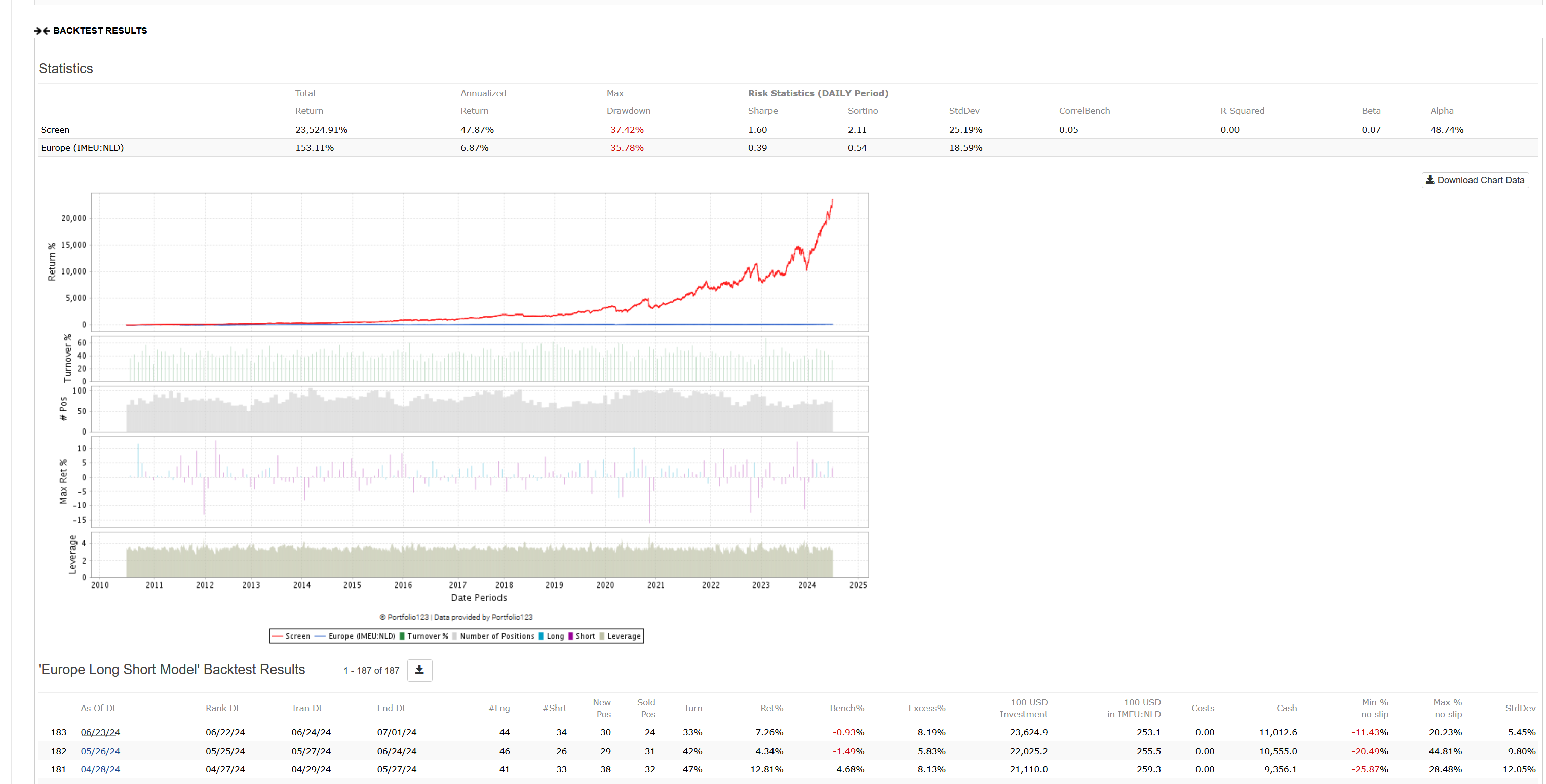

With the volume filter the number of stocks is reduced from 3500 to 1300. Is the volume so much lower in EU+ ore is there something in the volume rule that has to be adjusted to EUR markets?

European stocks in general have much lower volume than US stocks. 65% of US primaries pass your rule while only 39% of European primaries pass.

I do not know whether transaction costs are higher or lower when trading European stocks of comparable volume, or whether they’re about the same.

I have measured the spreads for US, Canadian, and European stocks. Spreads should, in general, be proportionate to the daily volatility divided by the square root of the daily dollar volume. In Europe, that proportionality is significantly higher than in the US or Canada. In other words, as you go up and down in terms of volume and volatility in Europe, you’ll end up paying more or less in transaction costs to a greater degree than in the US or Canada, all other things being equal. The exception may be the London Stock Exchange, where spreads are generally much higher and where volume and volatility doesn’t seem to make that much of a difference. British stocks are tough to trade because not only are you paying a portion of a higher spread, you’re also paying a transaction tax. But it’s very hard to make judgments here. The spread data that I get for LSE stocks could be way off for some reason.

Using my limited data, I would guess that the cost of buying a stock trading with a median daily dollar volume of $70,000 would be about 20% higher in the US than in Europe, about 50% higher in Britain (not including the tax), and about the same in Canada. That’s because spreads tend to be a little bit lower in Europe and Canada than in the US and quite a bit higher in Britain. As you go lower in volume, the spreads increase more quickly in Europe; as you go higher, the spreads decrease more quickly in Europe.

But all this is very conjectural, based on very limited data.

Yuval - where did you get this information about this relationship between spreads and daily volatility and daily dollar volume? Did you figure it out for yourself with data or is it based on a paper that can be accessed online?

I inferred it. The commonly accepted formula for transaction costs is the sum of a) a constant times the spread as a percentage of the stock price and b) another constant times the daily volatility times the square root of the amount invested divided by the square root of the daily dollar volume. I have observed that both a) and b) have a linear relationship to transaction costs, and verified that through extensive cataloguing of my own transaction costs. Because both those linear relationships go through the point (0,0), then a) and b) also have a linear relationship. And indeed, you can easily verify using a screen on P123 and an Excel spreadsheet that spreads as a percentage of price do indeed have a positive correlation with daily volatility and a negative correlation with daily dollar volume.

Me from Poland. Commissions are high, 0.25% per transaction is a super great deal.

However, the market can be extremely inefficient and volatile especially in small stocks from time to time (Covid, the War in Ukraine).

I-Star Market Impact Model (i-star) is probably the gold standard for estimating market impact. The key factor is avg. daily volume.

I thought about the implications of this when it comes to using P123. In doing so, I read some more of the older posts you wrote. I like the idea of linking stock ranks to expected returns as mentioned here : How to find cross-sectional Rank or RankPos - #5 by primus and after that subtracting transaction costs. As mentioned, this can then be used in formula weighting or buy/sell rules.

However, If I would use this ‘expected returns based on ranks’ type thinking and a formula for transaction costs based on volatility, transaction size and volume in for example a simulation with formula based weighting, then it probably will not backtest well.

This is because the assumption that P123 has about how to punish for transaction costs differs from the way I correct my rankings based on transaction costs.

Hence, I think the correct way to go about this is to first backtest using the definition for transaction costs that P123 itself uses. And then, when this approach gets validated and indeed improves returns (or other performance metrics) compared to not taking into account transaction costs, change the transaction costs formula to one based on volatility, transaction size and volume. Of course, this might not backtest well. But it should improve returns in practice (out-of-sample) anyhow.

For me, this raises the question whether it should be possible for users to adjust the variable slippage formula in their simulations.

I’m based in the US and have a model focused on "Europe." I’d like to trade it but haven’t been able to determine the overall transaction costs for each exchange or country. Does anyone have clarity on this?

It would be great if Portfolio123 could account for taxes, stamp fees, and other necessary charges. I trade through Interactive Brokers (IB), and any detailed information about fees and actual transaction costs would be highly appreciated.

Additionally, I’d love to hear how others trade European markets. I use IB's API, but I’m unsure how the P123 ticker syntax maps to the required IB syntax for trading across different countries in Europe.

I used to use IB but stopped. I now use Fidelity for my personal accounts but they charge 1% for currency conversion; for my hedge fund I use StoneX, but that option isn't available for individual investors.

Besides financial transaction taxes you'll also pay taxes on dividends, and unlike Canadian dividend taxes those are not recoupable.

For polish stocks I have a brokerage account in Santander Bank (Poland) with account in PLN.

In general, IB is by far most popular option to trade all European equites in Europe. The second most popular will be DeGiro.

Does any US investor have experience trading in "Europe" and know what the actual average costs tend to be?

It seems like this might be too complex to determine upfront. Perhaps it is necessary to paper trade the portfolio and analyze what IB charges for executing these trades.

About a year ago, when I was trading tons of European stocks with IB, I made the following chart. These are round-trip costs (double per-transaction costs) based on IB's commissions and what I thought were the taxes (though I now know I was wrong about some of those). Anyway, this will give you some idea. But really the link to IB's commissions schedule that I gave earlier is the best source.

There may be stamp duty and financial transaction taxes in Taiwan, India, the Philippines, Pakistan, Hong Kong, and Singapore, but if so they're very low. The highest is probably Taiwan's, which is either 0.15% or 0.3%. Along with the APAC countries P123 would very likely offer developing markets, including South American, Central American, Mexican, and African exchanges. Very few of those countries charge financial transaction taxes.