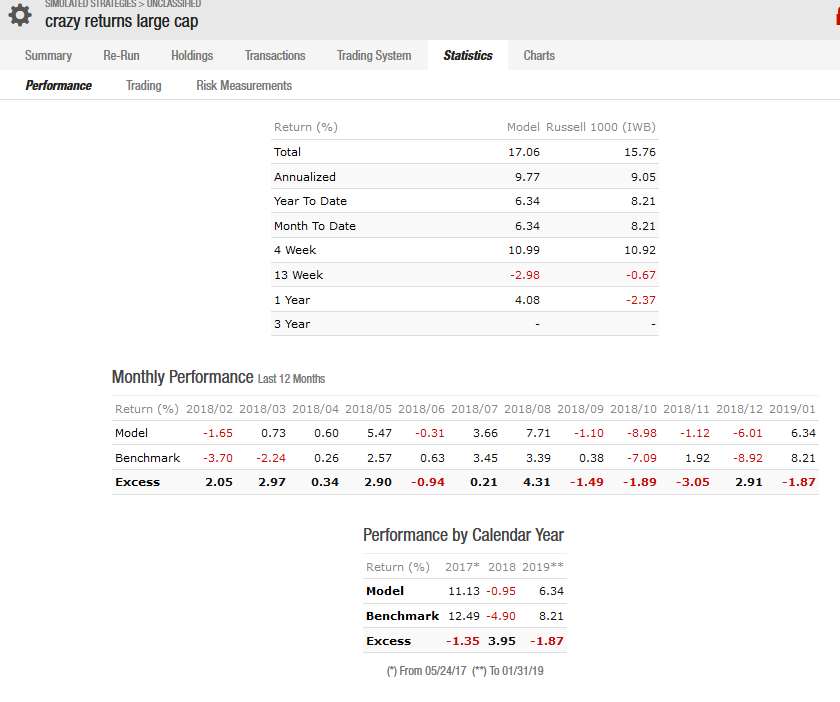

We have diverted from the post’s message, namely that it is not necessary to have many trades to make a decent return by combining the tools of P123 with outside economic data. I have expanded the 4-Trade model to trade more often (38 times since 2000), and it now it shows an 18% annualized return, up from 13.3% for the 4-Trade model.

It uses, apart from three recession indicator series, a custom formula to calculate the max drawdown for USMV and benchmark SPY over 200 days.

P123-Team, if you are listening, please provide a new function for max DD, proposed syntax maxDD(bars [,offset,series]). This function could be used in ranking systems as well, and it does improve simulated returns from what I can tell.

Here are the rules for the model to make it trade more often:

Buy1: Eval( $portsum>=5 ,TICKER(“USMV”),TICKER(“IEF”)), where $portsum is a market timer.

Sell Rules 1 to 4:

Sell1: Eval(close(0,GetSeries(“iM-LLI”))<-2 ,TICKER(“USMV”),TICKER(“ief”)) & nodays > 25

Sell2: Eval(close(0,GetSeries(“iM-SLI”))<4 ,TICKER(“USMV”),TICKER(“IEF”)) & nodays > 25

Sell3: Eval(close(0,GetSeries(“WLI”))<10 & $portsum<2 ,TICKER(“USMV”),TICKER(“IEF”)) & nodays > 25

Sell4: TICKER(“USMV”) & 0.5*$stockDD200 < $benchDD200 & nodays>25

To address Marc’s critique that all the previous models posted here start in 2000, there is also a backtest attached, starting in Jan-2015 which has only 12 Trades. It shows an AR= 16.1%, comfortably out-performing the bench SPY. Sell1 and 2 do nothing in the 2015 model. Sell3 uses the ECRI WLI growth, and is included here because of the many false positives it produces, otherwise Sell4 would only be effective, with limited success.

One can download WLIg for free: https://www.businesscycle.com/

I added 2.6 to the growth rate because this gives the WLIg the best recession capturing characteristics (which are not particularly good, but we don’t care about this because we do not want to signal recessions with it here). The iM-LLI and iM-SLI series will soon be available for free downloading at iMarketSignals.

So this will be my last post on this subject in this view-thread, please note that without the great P123 platform and its tools one could not backtest such a model. Thank you P123-Team.

Finally, I don’t want to use this view-thread to promote the use of recession indicators in models. But nevertheless it is interesting to use the new series upload function for this. BTW I wanted to make my series public, but currently there does not seem to be a way to do it.