Since I am convinced that I can’t determine the market direction, I am trying to develop Sims/Ports that, in effect, do that for me. I have tried to develop Sims/Ports that use various market timing approaches to try and limit my max drawdown without reducing my annual gains very much. This is sure a lot easier than me trying to determine which way the market is going. I have been using 3 variations of market timing (that I have discussed in previous posts) in most of my ports. They are:

-

Buy Rule; BenchClose(0) > sma(15,0,#Bench) or sma(15,0,#Bench) > sma(50,0,#bench)

Sell Rule; Rank < 101, and I set “Allow Sold Stocks to be Re-bought at current Rebalance” to Yes.

In some Ports I use the Sell Rule; (15,0,#bench) and sma(15,0,#bench) < sma(50,0,#bench), and I set “Allow Sold Stocks to be Re-bought at current Rebalance” to No. -

Buy Rules; BenchClose(0) / BenchClose(5) > 1 or BenchClose(0) / BenchClose(10) > .98:

Sell Rules; BenchClose(0) / BenchClose(5) < >97

I use a variation of Number of Bars and % in some Ports. This approach caused the most rotation out of and back into the market. -

Buy Rule; Pr4W%ChgInd > -2 & Pr4WRel%ChgInd > 0

Sell Rule; Pr4W%ChgInd < -2 or Pr4WRel%ChgInd < 0

I use a variation or % values in some Ports. These Ports never went fully out of the market (although their Sims did occasionally). They just rotated from one industry to another.

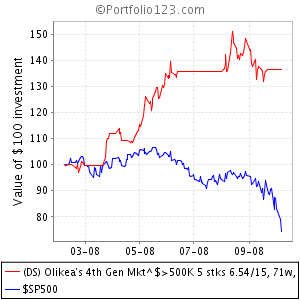

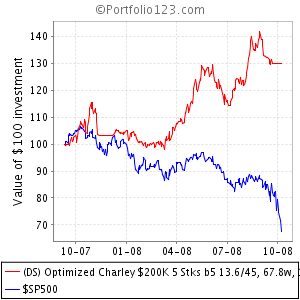

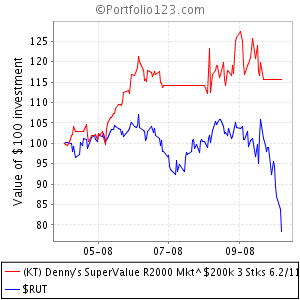

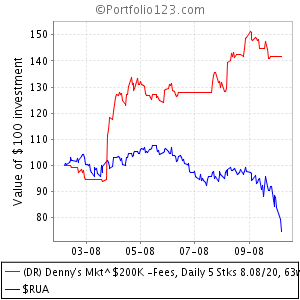

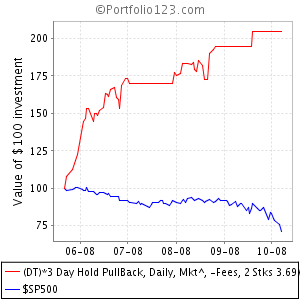

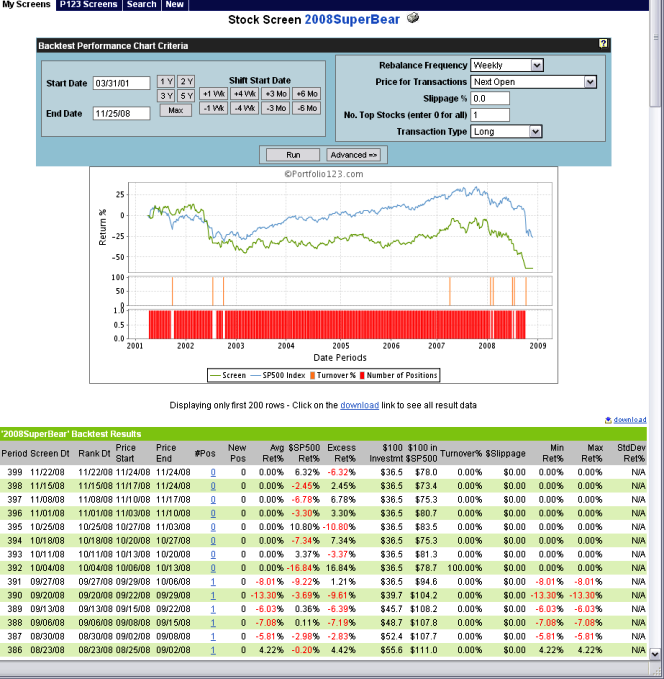

Since July ’07 the Ports that use the above rules have gradually moved out of, and back into the market. I have been as high as 80% in cash in August and January, and nearly fully invested in October and December. I am currently about 90% re-invested as of my buys last week and this morning. A few of the Ports were whipsawed in the October-November timeframe. Overall, the sum of my market timing Ports had a max drawdown of 16.4% on January 22nd, while the Russell 2000 had a max drawdown of 24.8% on March 10th. So I have beaten the benchmark of the type of stocks I buy by about 8%. I consider myself a relative aggressive trader and I have a fairly high tolerance for drawdown. 16.4% is significantly less that I have experienced in the past during >10% market corrections. So I am happy with that.

The Sims of these Ports imply that I will only lose a few % of the annual gain relative to Sims without the market timing rules. I will have to wait until we have had a run-up over a significant period of time to see if I haven’t actually hurt the annual gain very much.

Although I don’t try to determine if we have seen the bottom yet, it looks like my Ports are telling me that we have!

Denny ![]()

{kind=link}