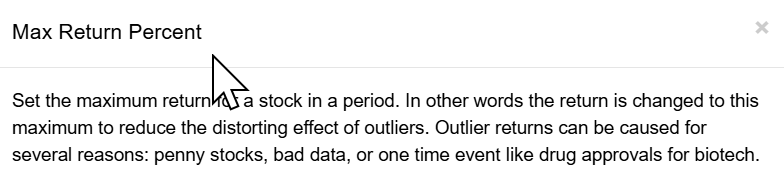

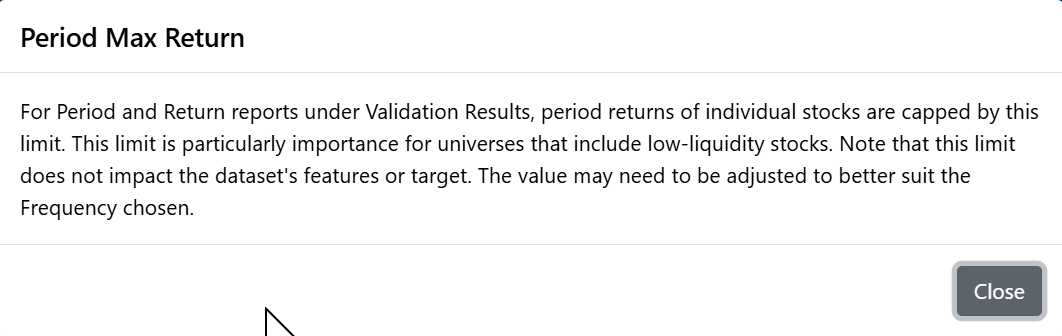

When doing a rank performance test and AI factor training, we can set a max return. A period, is that the rebalancing/sampling period (one week)?

That is correct. Period Max Return caps the return of a stock per Frequency. It does so like this: UBound(Future%Chg_D(perf_bars), max_ret).

1 Like