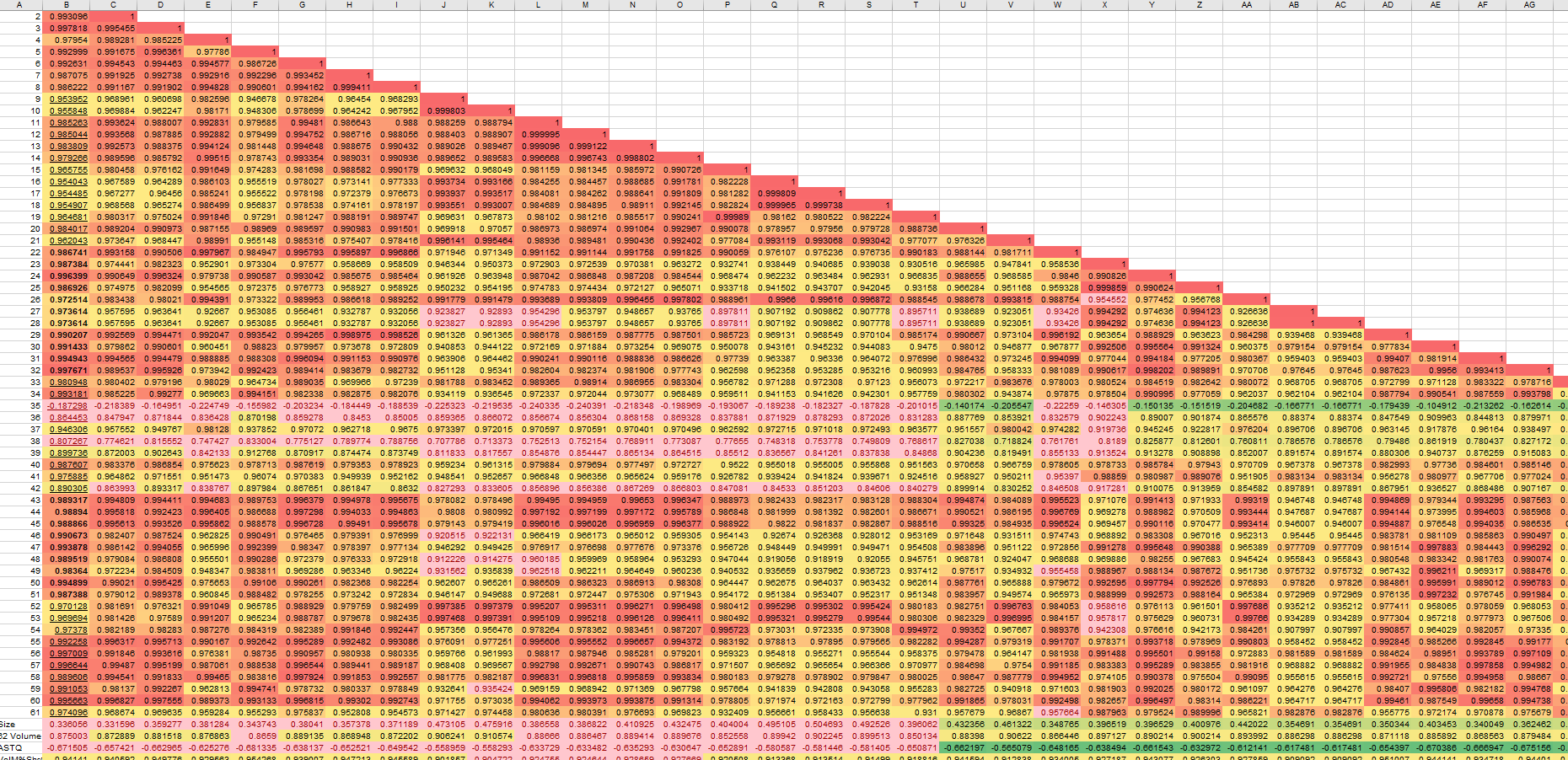

If I have 50 nodes and want to pick out the nodes that historically are least correlated, does anyone know how I can proceed to find the individual nodes that historically are least correlated with each other?

Is it possible to measure, for example by creating a correlation matrix?

Here are the 50 nodes I want to test:

| NetFCFQ/MktCap | Universe | Higher |

|---|---|---|

| FCFQ/mktcap | Universe | Higher |

| (NetFCFQ/ShsOutMR)/Close(0) | Universe | Higher |

| FCFPSQ/Price | Universe | Higher |

| (NetFCFQ / AstTotQ) + (NetFCFTTM/mktcap) | industry | Higher |

| NetFCFQ / AstTotQ | Universe | Higher |

| NetFCFQ/AstTotQ | Universe | Higher |

| FCFQ/EV | Universe | Higher |

| (OperCashFlQ-CapExQ)/EV | Universe | Higher |

| (mktcap + DbtTotQ) / Eval(EBITDAq>0,EBITDAq,NA) | Sector | Lower |

| (OperCashFlQ+ IntExpQ-CapExQ)/EV | Universe | Higher |

| OperCashFlQ/EV | Universe | Higher |

| IsNA( (EBIT(0,Qtr)-EBIT(4,Qtr))/ABS(EBIT(4,Qtr)) - (AstTotQ-AstTot(4,Qtr))/ABS(AstTot(4,Qtr)), 0) | Universe | Higher |

| (OCFPSTTM-(CapEx(0,TTM)/ShsOutMR))/ Price | Universe | Higher |

| OpIncPSQ/EVPS | Universe | Higher |

| NetFCFPSQ/Price | industry | Higher |

| NetFCFTTM / (Price * Vol3mAvg) | Universe | Higher |

| OpIncBDeprQ/EV | Universe | Higher |

| EBITDA(0,QTR)/EV | Universe | Higher |

| FCFYield | Universe | Higher |

| OpIncGr%PYQ | Sector | Higher |

| (NetFCFPSTTM + DivPSTTM) / Price | Universe | Higher |

| FCFTTM/mktcap | Universe | Higher |

| GrossProfitQ/AstTotQ | Universe | Higher |

| (FCFPSTTM + DivPSTTM) / Price | Universe | Higher |

| GR%PYQ(FCF) | Universe | Higher |

| FCFGr%PYQ | Universe | Higher |

| EV2EBITDAQ | Universe | Lower |

| ROE%Q | Universe | Higher |

| GR%PYQ(NetFCF) | Universe | Higher |

| NetFCFGr%PYQ | Universe | Higher |

| (opincq-opincpyq)/max(2,abs(opincpyq)) | Sector | Higher |

| IncBTaxQ/EV | Universe | Higher |

| PEInclRDQ | Universe | Lower |

| OperCashFlQ/AstTotQ | Universe | Higher |

| (OpMgn%Q - OpMgn%PYQ) / abs(OpMgn%PYQ) | Universe | Higher |

| OpMgn%Gr%PYQ | Universe | Higher |

| CurFYEPSMean/abs(CurFYEPS13WkAgo) | Universe | Higher |

| EBITDAGr%PYQ | Universe | Higher |

| NetFCFTTM / AstTotTTM | Universe | Higher |

| eval(NextFYEPS8WkAgo>0,(NextFYEPSMedian-NextFYEPS8WkAgo)/NextFYEPS8WkAgo,NA) | Universe | Higher |

| GrossProfit%AssetsQ | Universe | Higher |

| NextFYEPSMean/abs(NextFYEPS13WkAgo) | Universe | Higher |

| AstTurnQ | industry | Higher |

| NetFCFPSTTM/price | Universe | Higher |

| NetFCFPSTTM / Price | Universe | Higher |

| (OperCashFlTTM - CapExTTM + 0.8*IntExpTTM) / EV | Universe | Higher |

| (opercashflttm-capexttm+0.87*intexpttm)/$ev | Universe | Higher |

| NetFCFTTM / MktCap | Universe | Higher |

| NetFCFTTM/mktcap | Universe | Higher |