I have been using the European dataset and let me tell you there is definitely some excess returns here. I was skeptical at first but am very impressed once I dug into it a little. Yuval said so and I should have listened.

Here is just one example of a microcap model with a focus on shareholder yield. Turnover is 65% so you hold for a year and a half (or 365 trading days in the stats section).

Feel free to copy this model, build off of it and develop your own ideas. Low fcf and high 26 week momentum also work great with microcaps in Europe.

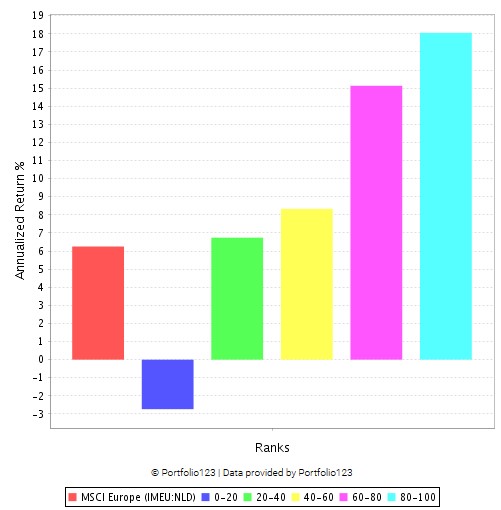

Factor backtest of shareholder yield since 2004 in microcaps with some liquidity filters. And a screenshot of the model if you can’t use the link because you don’t have European data…yet.

I don’t think 0% slippage is at all realistic here, and would advise users not to run sims with 0% slippage. Returns are still impressive if you add slippage, especially with such low turnover! If you run it with different starting dates, most of the outperformance is concentrated in 2009 and mid-2019 through today, which makes sense since it’s a heavily value-weighted strategy . . .

Will do. I added 0.5% slippage in for starters. Will adjust when I get some more concrete numbers. Variable seems unrealistically high in the lower liquidity stocks. When I was using VWAP algo and where it tried not to take liquidity, I was getting just a hair above the closing price on average. This was on microcaps to smallcaps. I never had 5-10% slippage. That’s way too high for an estimate.

If anyone else wants to submit their models, feel free. I have more on the way but will be posting my more basic systems. The goal is to generate ideas to help others build their own. Not to necessarily provide ready-baked models so 100 people all trade the same thing. Then you will be getting 5 - 10% slippage by chasing the identical trade.

It’s not specifically related to Europe, but I noticed you just use a broad “Europe (Incl. Foreign Primary)” universe, and then put minimum liquidity and price conditions only in your buy rules. I’m curious if you always use this approach for your strategies?

I’ve always put the liquidity/price constraints in the universe rules for my strategies, but I had made a note to explore moving them to buy rules just as you had done. With the constraints in the universe I tend to see names that bounce around one of the thresholds, causing my strategy to buy, sell, and maybe re-buy a stock as it comes in and out of the universe, and I was hoping to minimize those edge cases.

Your approach would avoid that, with the side effect of including a wider set of stocks in the information universe, for better or for worse. So I’m curious if your approach is intentional and how it’s played out for you?

Honestly, I don’t have any one set way of doing things. Here is one consideration where I may go one way or another.

Suppose I want a model for Utilities. If I keep the universe too broad, it makes it difficult to use ranking rules. I may get zero Utility stocks with a rank>90. And if I lower the rank too much, it isn’t a timely signal. In this instance I may choose to make the universe very specific.

Each case requires me thinking what my objective is. And experimenting a little. I will often try it both ways. And think about what the differences are between the two.

When making models public, I try not to make too many custom universes as then I have to make that public too. So I wouldn’t read too much into that.