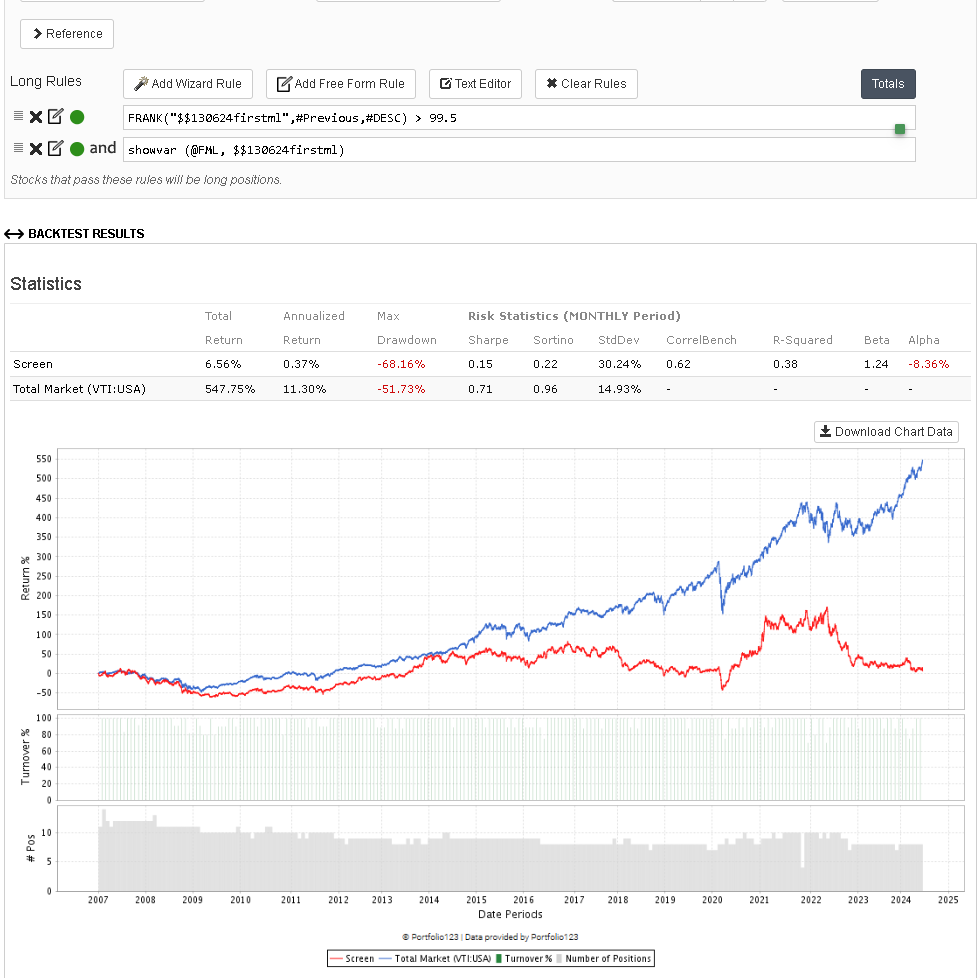

I have now tried to code my own ML code to test it on the dataset from p123, and then run the predictions on the stocks in the screen backtest (FRANK("$$130624firstml",#Previous,#DESC) > 99.5)

The results were completely dismal:

I can't understand why it's so terrible.

I am sharing everything here in case anyone has any input on whether I am making a mistake:

-

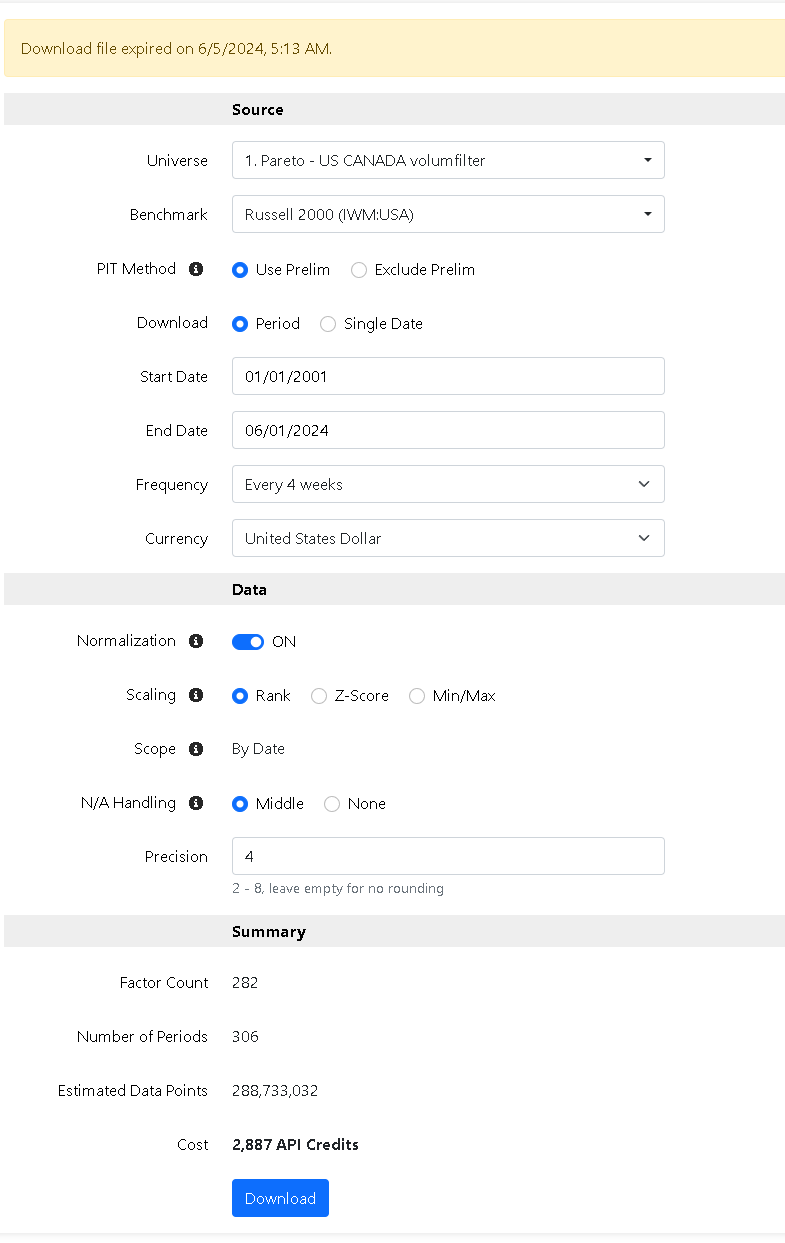

Here is the dataset: 020624RAA.csv - Google Drive

-

Here is the predicted score: predictions.csv - Google Drive

-

Here is what the code dose:

- Load and Preprocess Data:

- Load CSV data using Dask, which allows handling large datasets efficiently.

- Set the 'Date' column as the index and check for the presence of the 'Ticker' column.

- Drop rows with missing values to ensure data integrity.

- Identify categorical columns and use

LabelEncoderfor those with fewer unique values. - Apply one-hot encoding to remaining categorical columns to convert them to numeric.

- Ensure all data columns are numeric, dropping any that are not after preprocessing.

- Split Data:

- Use a sliding window approach to split the data into training, validation, and test sets.

- Each window includes a period for training/validation and a subsequent period for testing.

- Maintain the 'Ticker' information for each set to track which stocks are being predicted.

- Split the target column (e.g., '1 Day Returns') from the features for model training.

- Train Models:

- Define three models:

RandomForestRegressor,ExtraTreesRegressor, andXGBRegressor. - Train each model on the training data, ensuring they learn patterns from historical stock prices.

- Save the trained models using

joblibfor later use, reducing the need for retraining. - Evaluate Models:

- Evaluate each trained model on the validation set using Root Mean Squared Error (RMSE).

- Compare the RMSE scores to determine which model performs best on unseen data.

- Select the model with the lowest RMSE as the best-performing model for making predictions.

- Recommend Stocks:

- Use the best-performing model to predict stock prices on the test set.

- Generate stock recommendations based on the predicted future prices.

- If the model provides feature importance, include this information in the recommendations to explain which features are most influential.

- Report Results:

- Save the model's predictions to a CSV file, including the date, ticker, and predicted value.

- Ensure the CSV report is properly formatted and saved to the specified file path.

- Main Execution:

- Ask the user whether to use existing trained models or train new ones.

- Load existing models if available, otherwise, train new models.

- Execute the entire workflow, from loading data to generating stock recommendations and saving the results, based on user input.

- Here is the Python code:

import pandas as pd

import numpy as np

from sklearn.ensemble import RandomForestRegressor, ExtraTreesRegressor

from xgboost import XGBRegressor

from sklearn.preprocessing import LabelEncoder

from sklearn.model_selection import GridSearchCV, TimeSeriesSplit

from sklearn.metrics import mean_squared_error, mean_absolute_error, r2_score, mean_squared_error

import joblib

import os

import csv

import logging

from tabulate import tabulate

logging.basicConfig(level=logging.INFO, format='%(asctime)s - %(levelname)s - %(message)s')

def load_and_preprocess_data(file_path):

logging.info("Laster inn data...")

data = dd.read_csv(file_path, parse_dates=['Date']).set_index('Date')

logging.info(f"Antall rader før forbehandling: {len(data)}")

logging.info(f"Antall kolonner før forbehandling: {len(data.columns)}")

logging.info(f"Kolonner før forbehandling: {data.columns}")

if 'Ticker' not in data.columns:

raise KeyError("Kolonnen 'Ticker' finnes ikke i den opprinnelige datasettet.")

tickers = data['Ticker'] # Bevar 'Ticker' kolonnen

data = data.dropna() # Rense dataene for manglende verdier

logging.info(f"Antall rader etter å ha droppet manglende verdier: {len(data)}")

logging.info(f"Antall kolonner etter å ha droppet manglende verdier: {len(data.columns)}")

logging.info(f"Kolonner etter å ha droppet manglende verdier: {data.columns}")

# Identifisere kategoriske kolonner

categorical_columns = data.select_dtypes(include=['object']).columns

logging.info(f"Identifiserte kategoriske kolonner: {categorical_columns}")

logging.info(f"Antall unike verdier i kategoriske kolonner: {[data[col].nunique().compute() for col in categorical_columns]}")

# Bruk LabelEncoder for å konvertere kategoriske kolonner med få unike verdier

for col in categorical_columns:

if data[col].nunique().compute() < 100:

le = LabelEncoder()

data[col] = data[col].map_partitions(lambda s: pd.Series(le.fit_transform(s)))

logging.info(f"Kolonner etter LabelEncoding: {data.columns}")

# Bruk pd.get_dummies for de gjenværende kategoriske kolonnene

data = data.map_partitions(pd.get_dummies, columns=[col for col in categorical_columns if data[col].dtype == 'object'])

logging.info(f"Kolonner etter pd.get_dummies: {data.columns}")

data = data.compute() # Konverter Dask DataFrame til Pandas DataFrame

data = data.apply(pd.to_numeric, errors='coerce') # Konverterer til numeriske verdier

logging.info(f"Kolonner etter konvertering til numeriske verdier: {data.columns}")

data = data.dropna(axis=1, how='any') # Fjerner kolonner som inneholder ikke-numeriske verdier

logging.info(f"Antall rader etter å ha droppet ikke-numeriske verdier: {len(data)}")

logging.info(f"Antall kolonner etter å ha droppet ikke-numeriske verdier: {len(data.columns)}")

logging.info(f"Kolonner etter å ha droppet ikke-numeriske verdier: {data.columns}")

data['Ticker'] = tickers # Legg tilbake 'Ticker' kolonnen

data = data.sort_index()

# Sjekk om Ticker-kolonnen er til stede

if 'Ticker' not in data.columns:

raise KeyError("Kolonnen 'Ticker' finnes ikke i datasettet etter forbehandling.")

logging.info(f"Startdato i datasettet etter forbehandling: {data.index.min()}")

logging.info(f"Sluttdato i datasettet etter forbehandling: {data.index.max()}")

return data

def split_data(data, target_column, train_size=0.7, val_size=0.2, window_size=5):

logging.info("Splitter data...")

logging.info(f"Startdato i datasettet før splitting: {data.index.min()}")

logging.info(f"Sluttdato i datasettet før splitting: {data.index.max()}")

train_data = []

val_data = []

test_data = []

tickers_test = []

start_date = data.index.min()

end_date = data.index.max()

window_end_date = start_date + pd.DateOffset(years=window_size)

while window_end_date <= end_date:

train_val_data = data.loc[start_date:window_end_date]

test_data_window = data.loc[window_end_date + pd.DateOffset(days=1):window_end_date + pd.DateOffset(years=window_size)]

train_val_data = train_val_data.iloc[:int(len(train_val_data) * (train_size + val_size))]

if train_val_data.empty or test_data_window.empty:

raise ValueError("Trenings-, validerings- eller testsettet er tomt. Sjekk dataens lengde og splitting.")

train_data_window = train_val_data.iloc[:int(len(train_val_data) * train_size / (train_size + val_size))]

val_data_window = train_val_data.iloc[int(len(train_val_data) * train_size / (train_size + val_size)):]

train_data.append(train_data_window)

val_data.append(val_data_window)

test_data.append(test_data_window)

tickers_test.append(test_data_window['Ticker'])

start_date = window_end_date + pd.DateOffset(days=1)

window_end_date += pd.DateOffset(years=window_size)

# Ensure the last window includes all remaining data

if window_end_date > end_date:

test_data_window = data.loc[window_end_date + pd.DateOffset(days=1):end_date]

if not test_data_window.empty:

test_data.append(test_data_window)

tickers_test.append(test_data_window['Ticker'])

X_train = [data.drop([target_column, 'Ticker'], axis=1) for data in train_data]

y_train = [data[target_column] for data in train_data]

X_val = [data.drop([target_column, 'Ticker'], axis=1) for data in val_data]

y_val = [data[target_column] for data in val_data]

X_test = [data.drop([target_column, 'Ticker'], axis=1) for data in test_data]

y_test = [data[target_column] for data in test_data]

return X_train, y_train, X_val, y_val, X_test, y_test, tickers_test

def train_and_save_model(model, X_train, y_train, model_path):

logging.info(f"Trener og lagrer modellen: {model_path}")

model.fit(pd.concat(X_train), pd.concat(y_train))

joblib.dump(model, model_path)

def evaluate_models(models, X_val, y_val):

best_model = None

best_score = float('inf')

best_model_name = ""

for model in models:

model_name = type(model).__name__

logging.info(f"Evaluating model: {model_name}")

predictions = model.predict(pd.concat(X_val))

rmse = mean_squared_error(pd.concat(y_val), predictions, squared=False)

logging.info(f"{model_name} RMSE: {rmse}")

if rmse < best_score:

best_score = rmse

best_model = model

best_model_name = model_name

logging.info(f"Best model: {best_model_name} with RMSE: {best_score}")

return best_model

def recommend_stocks(model, X_test, tickers_test, feature_names, num_recommendations=20):

logging.info("Starting stock recommendation...")

latest_data = X_test[-1]

if latest_data.empty:

logging.error("Latest data is empty. Cannot proceed with stock recommendation.")

return pd.DataFrame()

predictions = model.predict(latest_data)

data = pd.DataFrame({'Ticker': tickers_test[-1], 'Predictions': predictions})

# Check if model has feature_importances_

if hasattr(model, 'feature_importances_'):

feature_importances = pd.DataFrame(

[model.feature_importances_ for _ in range(len(data))], columns=feature_names

)

data = pd.concat([data.reset_index(drop=True), feature_importances.reset_index(drop=True)], axis=1)

else:

logging.warning("Model does not have feature_importances_ attribute.")

recommended_stocks = data.sort_values(by='Predictions', ascending=False).head(num_recommendations)

logging.info("Stock recommendation completed.")

return recommended_stocks

def display_recommendations(recommended_stocks):

logging.info("Displaying recommendations...")

if recommended_stocks.empty:

logging.error("No recommendations to display.")

return

# Sorter featurene etter viktighet for den første tickeren

first_ticker_features = recommended_stocks.iloc[0, 2:].sort_values(ascending=False)

# Skriv ut tabellen for den første tickeren

logging.info(tabulate(

[['Ticker', recommended_stocks.iloc[0, 0]], ['Predictions', '{:.3f}'.format(recommended_stocks.iloc[0, 1])], ['Top 50 Features', ''], *first_ticker_features.head(50).items()],

headers=['Feature', 'Importance'], tablefmt="fancy_grid"

))

# Skriv ut tickerne for de resterende anbefalte aksjene

logging.info("\nResterende anbefalte aksjer:")

for i in range(1, len(recommended_stocks)):

logging.info(f"{i}. {recommended_stocks.iloc[i, 0]} ({'{:.3f}'.format(recommended_stocks.iloc[i, 1])})")

logging.info("Recommendations displayed.")

def print_model_report(model, X_test, y_test, tickers_test, output_file_path):

try:

output_dir = os.path.dirname(output_file_path)

if not os.path.exists(output_dir):

os.makedirs(output_dir)

output_file = os.path.join(output_dir, os.path.basename(output_file_path))

combined_tickers = []

combined_dates = []

combined_predictions = []

for X, tickers in zip(X_test, tickers_test):

predictions = model.predict(X)

combined_predictions.extend(predictions)

combined_tickers.extend(tickers)

combined_dates.extend(X.index)

with open(output_file, 'w', newline='') as csvfile:

writer = csv.writer(csvfile)

# Skriv overskrifter til CSV

writer.writerow(['Date', 'Ticker', 'Value'])

for date, ticker, prediction in zip(combined_dates, combined_tickers, combined_predictions):

date_str = date.strftime('%Y-%m-%d')

writer.writerow([date_str, ticker, '{:.3f}'.format(prediction)])

logging.info(f"Prediksjoner skrevet til {output_file}")

except Exception as e:

logging.error(f"En feil oppstod under skriving av CSV-filen: {e}")

def main():

file_path = r'C:\\Users\\mywag\\Documents\\YT\\020624RAA.csv'

model_paths = ['trained_rf_model.pkl', 'trained_et_model.pkl', 'trained_xgb_model.pkl']

data = load_and_preprocess_data(file_path)

logging.info(f"Kolonner i datasettet: {data.columns}")

target_column = '1 Day Returns'

if target_column not in data.columns:

raise KeyError(f"Målkolonnen '{target_column}' finnes ikke i datasettet.")

# Del dataene før modellvalg

X_train, y_train, X_val, y_val, X_test, y_test, tickers_test = split_data(data, target_column, train_size=0.7, val_size=0.2, window_size=5)

feature_names = X_test[0].columns

models = [

RandomForestRegressor(n_estimators=100, max_depth=10, min_samples_split=2, min_samples_leaf=1, n_jobs=-1),

ExtraTreesRegressor(n_estimators=100, max_depth=10, min_samples_split=2, min_samples_leaf=1, n_jobs=-1),

XGBRegressor(n_estimators=100, max_depth=10, min_child_weight=1, gamma=0, subsample=0.8, colsample_bytree=0.8, objective='reg:squarederror', n_jobs=-1, scale_pos_weight=1, seed=27, reg_alpha=0.00006)

]

use_existing_models = input("Vil du bruke tidligere trente modeller? (y/n): ").lower() == 'y'

trained_models = []

if use_existing_models:

for model_path in model_paths:

if os.path.exists(model_path):

trained_models.append(joblib.load(model_path))

else:

logging.info(f"Filen {model_path} finnes ikke. Trener en ny modell.")

model = models[len(trained_models)]

train_and_save_model(model, X_train, y_train, model_path)

trained_models.append(model)

else:

for i, model in enumerate(models, start=1):

model_path = model_paths[i-1]

train_and_save_model(model, X_train, y_train, model_path)

trained_models.append(model)

# Evaluate models and select the best one

best_model = evaluate_models(trained_models, X_val, y_val)

# Anbefale aksjer basert på den beste modellen

logging.info("Anbefalte aksjer:")

recommended_stocks = recommend_stocks(best_model, X_test, tickers_test, feature_names)

display_recommendations(recommended_stocks)

# Generere og skrive ut rapport

output_file_path = os.path.join(os.path.dirname(file_path), 'predictions.csv')

print_model_report(best_model, X_test, y_test, tickers_test, output_file_path)

if __name__ == "__main__":

main()