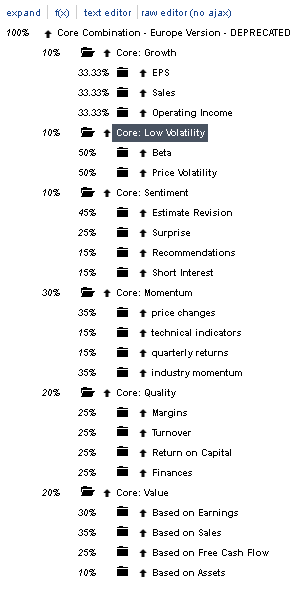

Some use composites (Core), while Focus just weights the individual node differently. In the core systems, you weight the factor folders differently between Europe and the US.

I tried to look for why and how this is done in the forum, but found little about:

How have you gone about choosing to use Composite or not?

How have you gone about assessing the weight of the individual node or composite?

So, it would have been very interesting to know how p123 have thought and proceeded when assagning a weight to a node or composite?

I know there is a lot of disagreement about how to optimize and whether a system should be optimized, but it would have been great to know which method p123 have used.

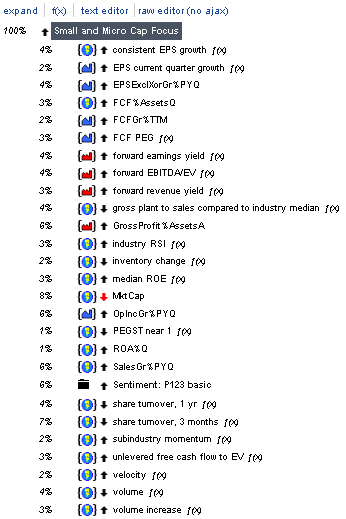

I came up with the Small and Micro Cap Focus ranking system as an alternative to Core Combination and based it on the ranking system I use every day. I just assigned it percentages that came kind of close to the ones I use, and percentages that make sense. I thought of putting the nodes into folders but I was having trouble deciding which folder to put certain factors in, and personally I don’t use folders. So I just put them all in alphabetical order. My assignment was to come up with a model that would perform well and that subscribers could use profitably. I didn’t optimize it, but I do optimize my own systems, and this is loosely based on those. I optimize by doing lots of simulations with varying weights on different universes and comparing the results.

When I first started using ranking systems in 2015 I found that my returns were usually better if I didn’t use folders than if I did. I don’t know why, or whether that’s generally true or not. But anyway, I started out not using folders, and it would be hard for me to switch back at this point because my mode of testing would have to radically change. The weights I gave in the response that you quoted were just weights I got from adding up the node weights, not folder weights.

I ran some tests to investigate. And that seems to be true. There is still a bit of higher turnover in the one that only consists of only nodes and that dosent have folders. So it could be a single stocks that makes the difference, but yes, when I went from folders to only nodes, it got a few percent better.

Here with only nodes. Here, the number of nodes in each factor folder was divided by the percentage weight the factor folder had in the original system.

The only reason I’ve come up with for improved performance of ranking systems with non-nested nodes is that there’s less manipulation of the actual rank of each individual factor, and therefore there are more possibilities for rank combination. For example, if you put accruals in your quality folder and earnings yield in your value folder, you’ll have a very slightly better chance of buying a company that’s manipulating its earnings than if you have them loose.

If I understand correctly you are using around 100+ factors.

The question was, if the factors in the “Small and Mirco Cap Focus” are a portion of the factors you are using in your strategies?

Second question was, are you adjusting the weights of all your factors on a regular basis?

As some factors perform better/worse during time, maybe it could be a solution to prioritize some factors over others (for example using lines regression)

First question: yes, those are some of the factors I use for my own portfolio.

Second question: I do adjust the weights of my factors, but very irregularly, and as a result of further testing rather than depending on recent factor performance.

Has anyone actually has a strategy to trade in multiple countries in Europe? My concern are taxes or more of the various tax treaties and I’m not sure is it really worth the trouble when USA is already a great market and with single and easy tax system. Also, a lot of information is not available in English such as local news about stocks.