I am accustomed to hearing the argument that to reduce idiosyncratic risk, one should hold more than 15-20 stocks(The Diversification Myth: Why 30 Stocks Aren’t Enough for Your Portfolio), but then I came across this. Does anyone have thoughts on this, and how many stocks do you hold?

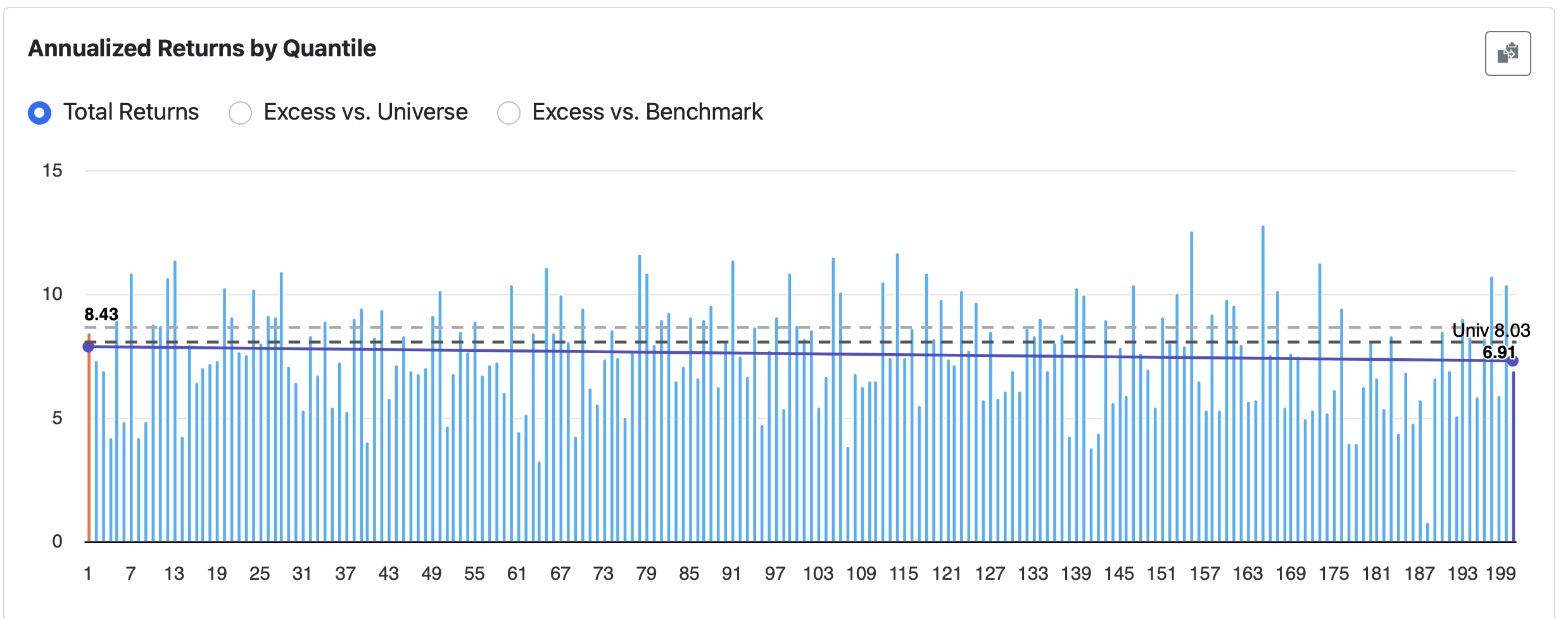

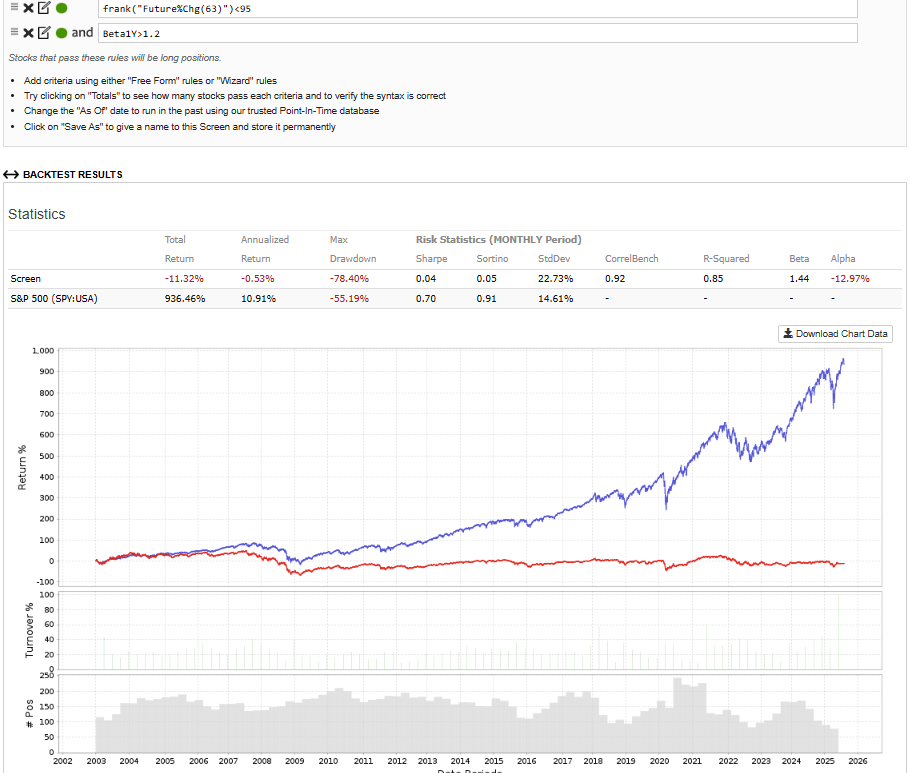

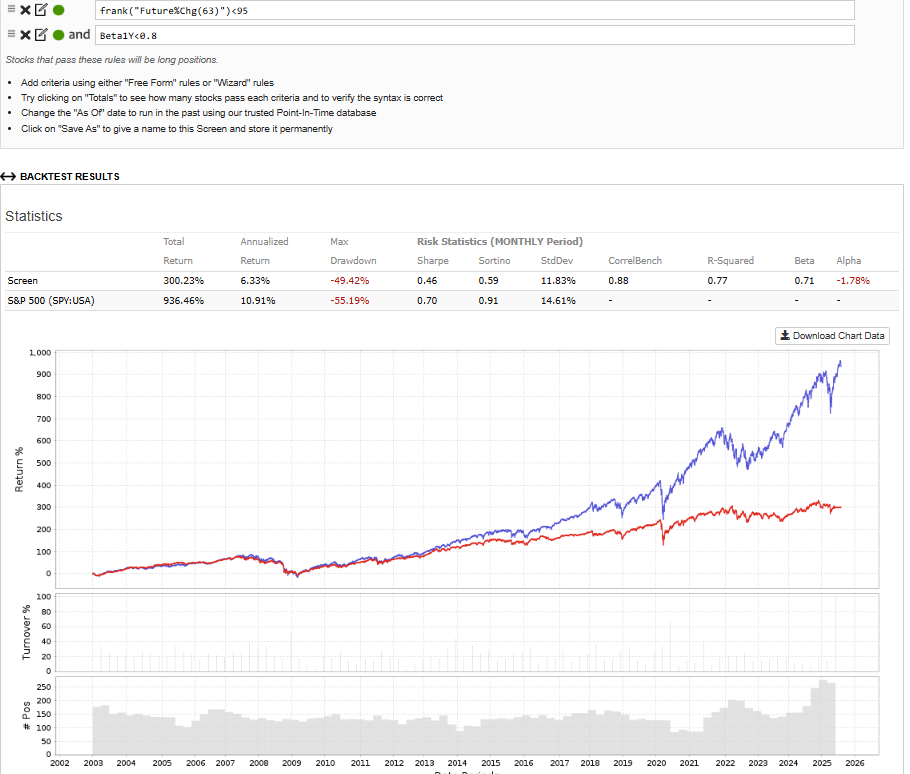

Regardless, it demonstrates how irrelevant it is to run tests or simulations in backtests with too few stocks. There is too much noise and randomness in the market.

Stocks")

The Studies Referenced in the Video:

-

JP Morgan - "The Agony and the Ecstasy" (2021 & 2024 editions)

-

Hendrik Bessembinder - "Do Stocks Outperform Treasury Bills?" (2018)

-

"Why Indexing Works" (2017)

-

"Mutual Fund Performance at Long Horizons" (2023)

-

"Underperformance of Concentrated Stock Positions" (2023)

-

"How many stocks should you own?" (2022)

-

"Fund Concentration, a magnifier of manager skill" (2022)

What the Studies Tell Us, Summarized in 10 Points:

-

Nearly half of all stocks end in disaster. 44% of stocks in the Russell 3000 index (a broad U.S. index) from 1980 to 2020 experienced a decline of 70% or more from which they never recovered. The risk of a permanent, massive loss in a single stock is therefore alarmingly high. (JP Morgan)

-

Most stocks lose to a risk-free savings account. Over half (57.4%) of all U.S. stocks since 1927 have had a lifetime return that is lower than a risk-free Treasury bill (T-bill). Thus, you statistically have a better chance of earning more by keeping your money in a risk-free asset than in a randomly selected individual stock. (Bessembinder)

-

The entire stock market's gain is driven by a small number of "mega-winners." While most stocks underperform, a small fraction delivers exceptional returns. These few winners pull up the average for the entire market. This explains why it is so difficult to beat an index fund—the probability of picking a loser is statistically much higher than finding one of these rare winners. (JP Morgan & Bessembinder)

-

Today's winners are often tomorrow's losers. This is one of the most critical points. Stocks that have performed best over the past 5 years have a statistical tendency to underperform the market over the next 10 years. Buying a stock because it "has done well" is a dangerous strategy. (Underperformance of Concentrated Stock Positions)

-

The old rule of "20-30 stocks" is outdated. To truly protect yourself against the worst long-term outcomes, you need far more stocks. Research shows that the worst outcomes (e.g., the 10th percentile) improve dramatically until the portfolio contains around 250 stocks . (How many stocks should you own?)

-

Concentration punishes the bad more than it helps the good. Increased concentration in a portfolio (fewer stocks) amplifies the outcome. It has a positive effect for those skilled at picking stocks, but an even larger negative effect for those who are not. Since most are not skilled stock pickers, concentration is a strategy that most often leads to poorer results. (Fund Concentration)

-

Even professional managers struggle to beat the market. Due to the skewness of the stock market, less than half (45.2%) of active funds managed to beat an S&P 500 index fund—and this was before their own management fees were deducted. The odds are stacked against active management from the start. (Mutual Fund Performance)

-

Catastrophic losses are unpredictable and can happen to "good" companies. Most companies that experienced massive losses had "buy" recommendations from analysts, were profitable, and had reasonable debt levels before their collapse. It is nearly impossible to predict which stock will be the next loser. (JP Morgan)

-

The mathematical reason why index funds work. When returns are positively skewed (few big winners, many losers), picking a random subset of stocks (stock picking) will almost always increase the probability of underperforming the entire index. Owning the whole market through an index fund is the only way to guarantee you capture the returns of the few winners. (Why Indexing Works)

-

A diversified portfolio is better than a coin flip against the market. Even a portfolio of 100 randomly selected stocks has historically had less than a 50% chance of beating the market index over a 10-year period. By picking stocks, you statistically have a greater chance of losing to the market than winning. (Bessembinder)