Reading “Quantitative Strategies for Achieving Alpha” with the hope of improving my short and long ranking systems. Its a little bit of a poor man’s version of what What Works on Wall St.

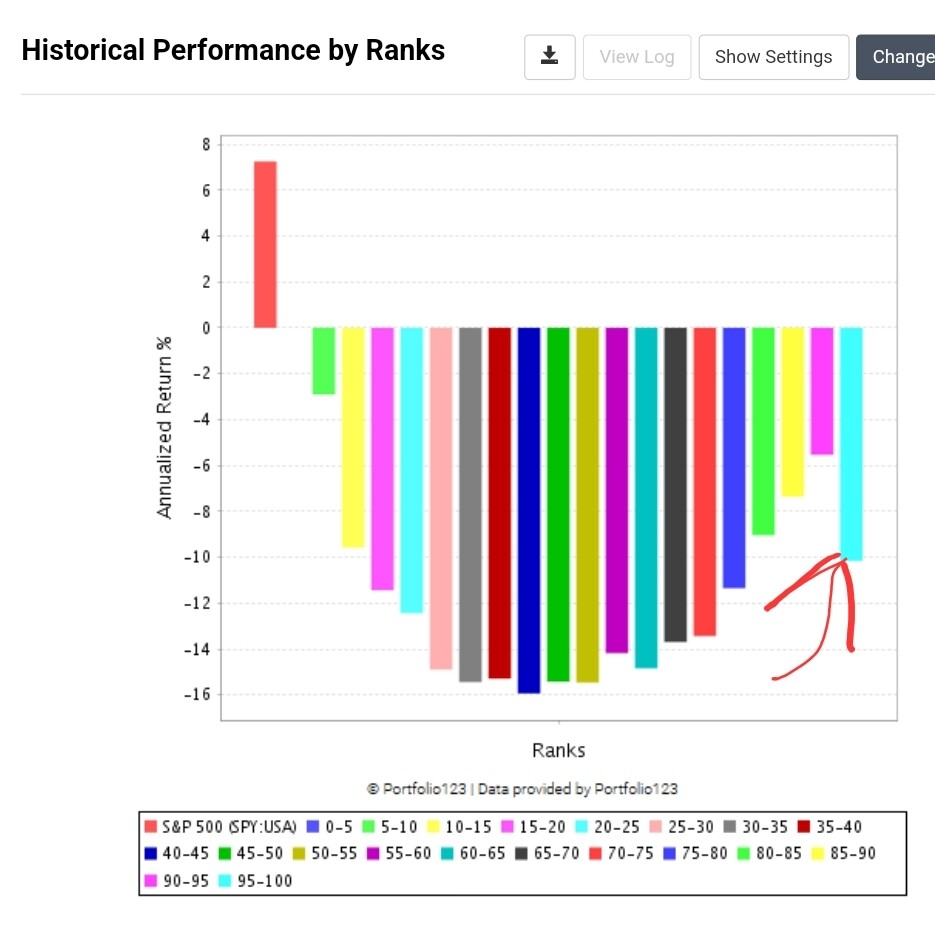

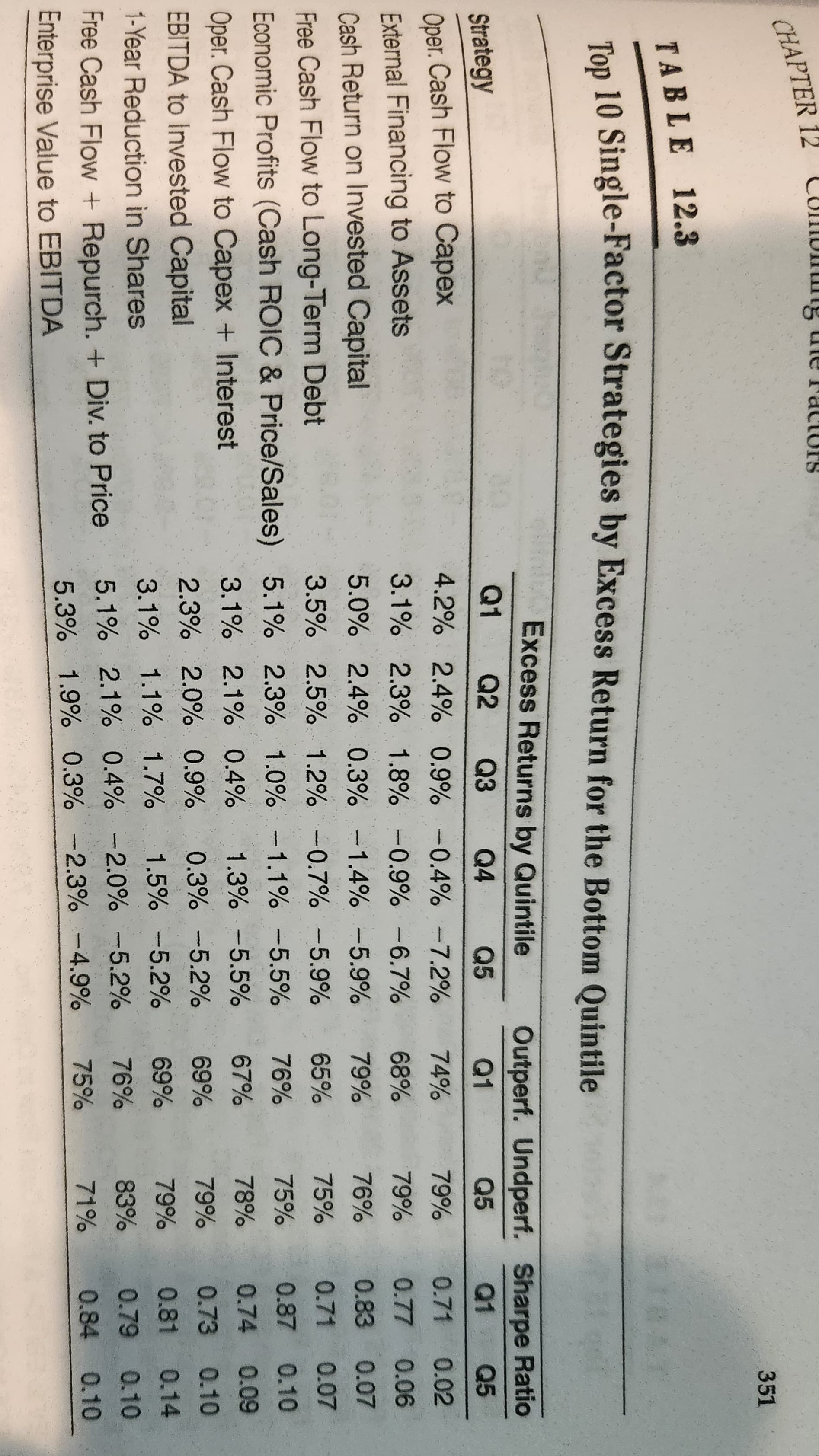

The testing recommends OperCashFl to CapEx as the best factor to select stocks for shorting.

However, when I run the ranking performance (short) the top bucket performance drops off. I believe its related to stocks with high CapEx having a less negative score. I’m really looking for stocks with awful OpCashFl (very negative) and huge CapEx. Any recommendations on how to improve the ranking formula? Should I just require that we only rank stocks with negative OpCashFl and put the CapEx in the numerator?

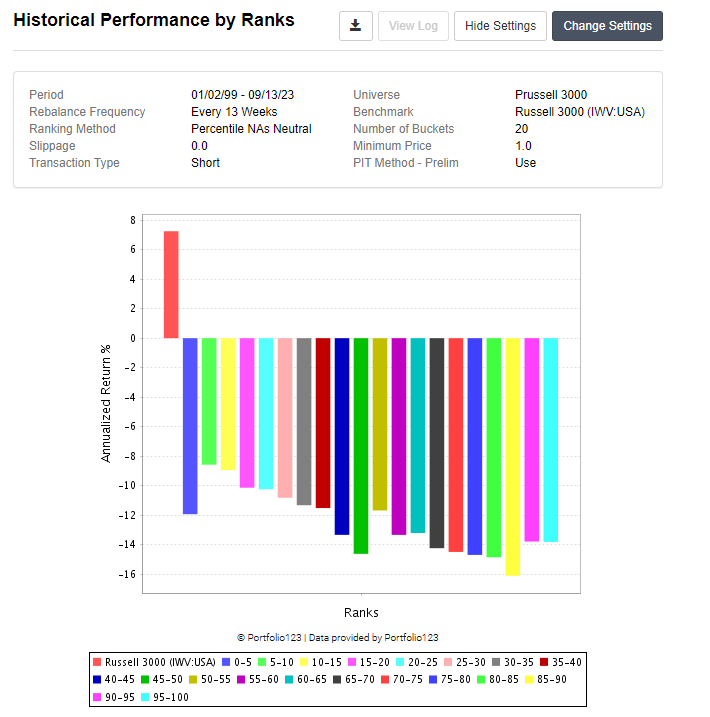

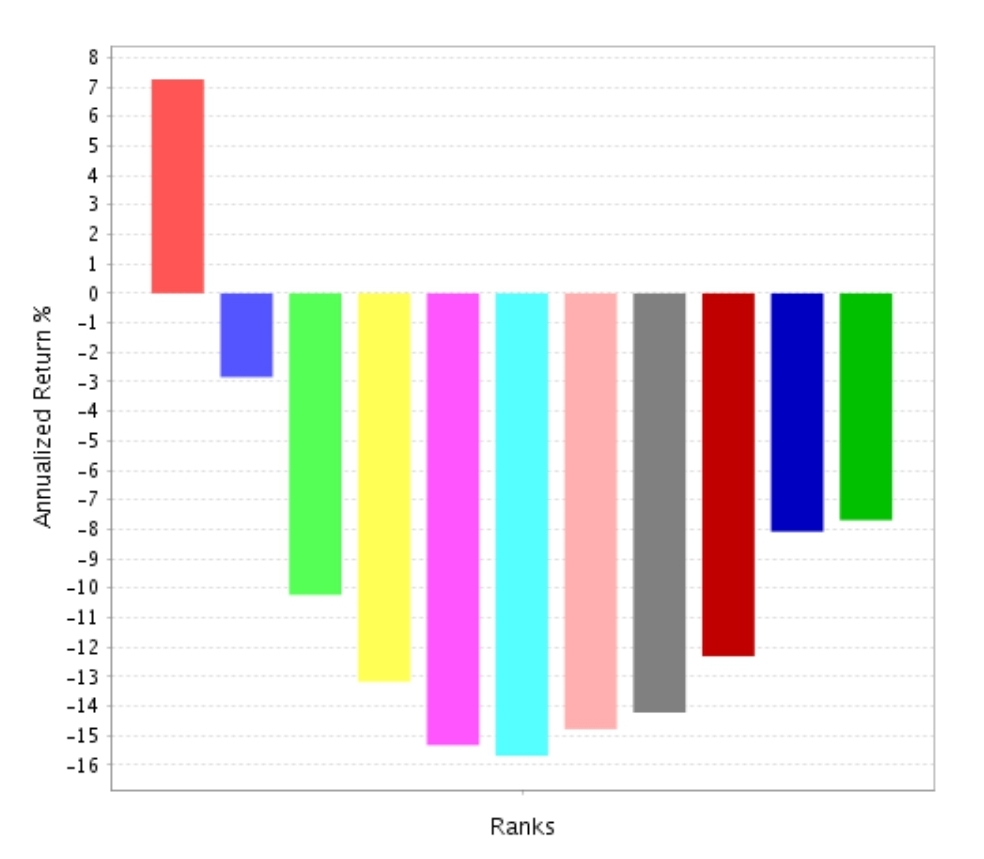

I have found that factor pretty useful myself, especially for long-term strategies. I use OperCashFlTTM / CapExTTM, universe, higher for long, lower for short. The 20-bucket charts can be misleading and are quite unstable (try different starting dates and you’ll see what I mean). I’d suggest trying five to ten buckets.