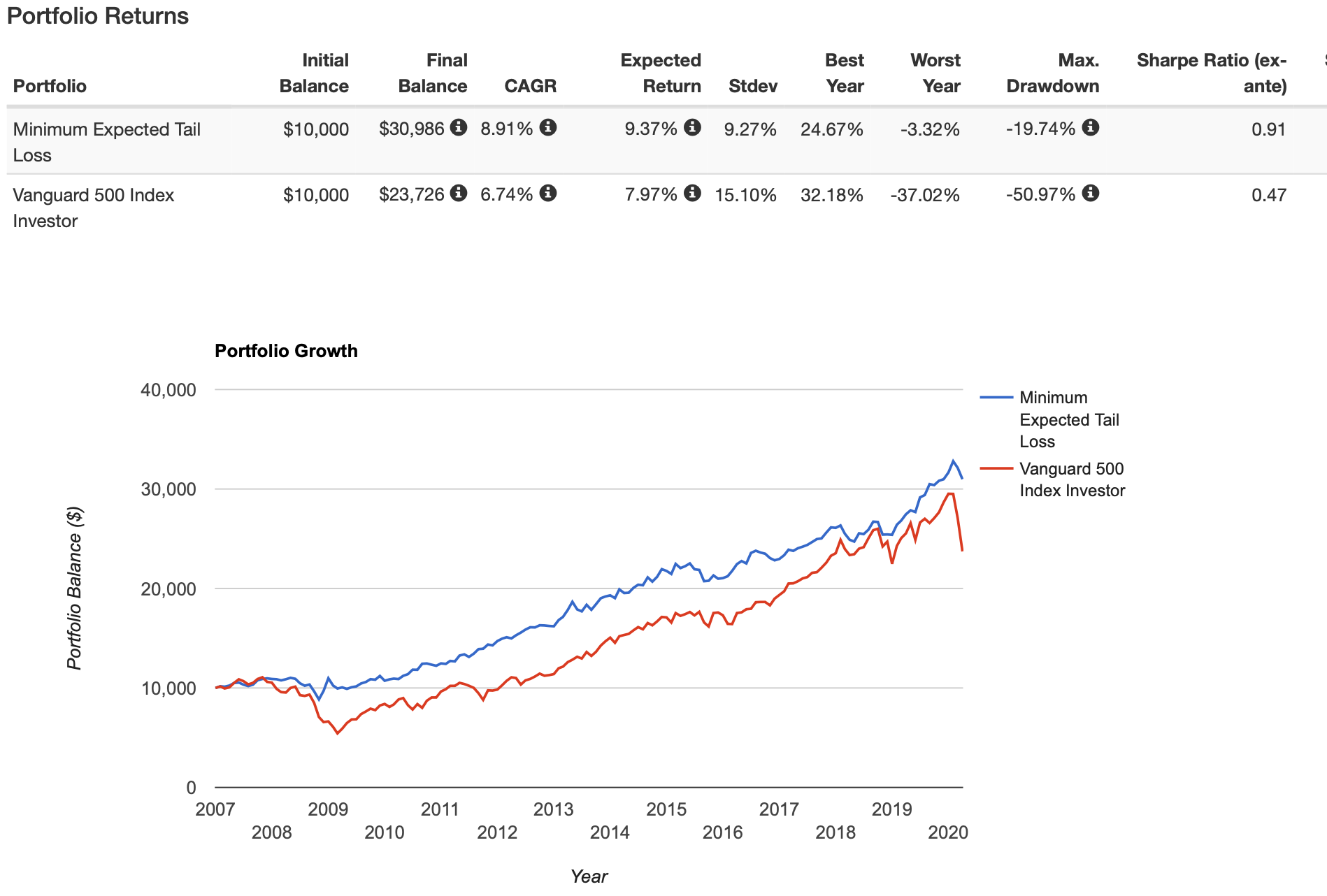

Porfolio Visualizer allows one to optimized a set of ETFs using expected shortfall (conditional value-at-risk). Other optimization methods are available.

Specifically the “Rolling Portfolio Optimization” on this site allows one look back over a specified period then it uses the results to weight the ETFs over a specified period in the future. So, this is a type of walk-forward testing.

I took a set of ETFs and set the program to look back 2 years and determine the weight of the assets that “Minimized Conditional Value-at-Risk” for that 2 year period. Those weights are were then used for the next month (in the future). This is then repeated each month by the program. So the program “Walks Forward” one month at a time.

So this is PIT.

These are my results. You can see that I beat the SP500 benchmark with much less risk and less of a drawdown.

I am happy to share which ETFs I used but you may want to look at this with your own ETFs.

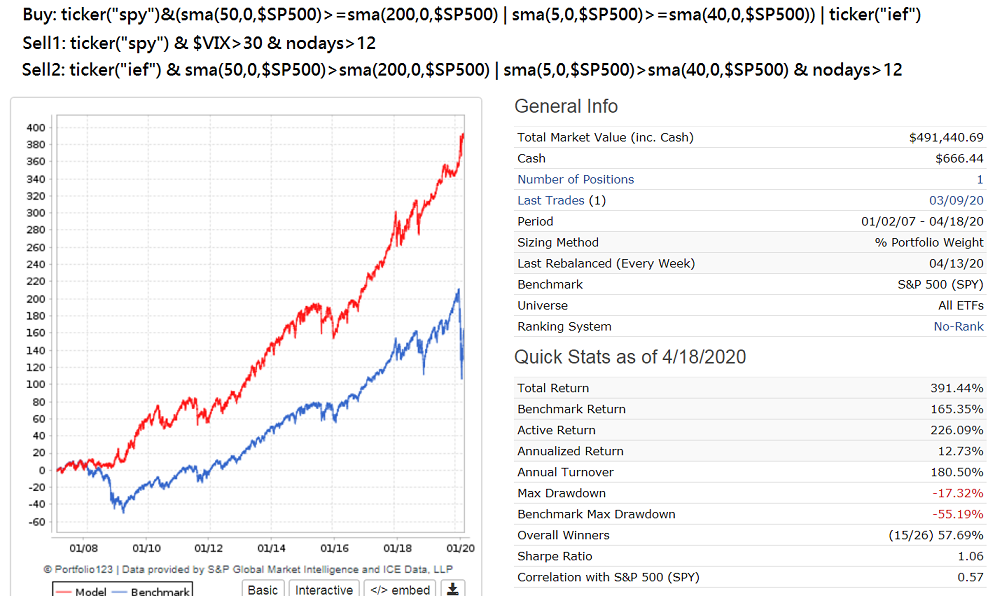

I used exactly the rules as you have them there but I cant quite can there. I cannot avoid the latest drawdown. Are there any other rules that you are using for this?