Hi everyone and Happy New Year!

I have been reading about order “price improvement” over the last few days. This would be improvement over the BID/ASK spread for market orders. Folio Investing has been good for small orders as there are no commissions per trade for window orders. But for larger orders—where commissions represent a smaller percentage of the trade—is Folio Investing the best?

First, I have been comparing Window Orders to Market Orders and there is no (statistical) difference. Market orders have less slippage in my sample. But the numbers are close and probably the same. A window order is about like a market order with no commission, I think.

Brokers are required to make “Best Execution” by law. That does not always mean best price improvement. A broker can always say they have “Best Execution” based on speed reliability etc. And can they all really be the best? Maybe not.

First. Folio is paid to refer to a particular market maker. See image of SEC Rule 606 disclosure below. UK made this illegal and sees it as a conflict of interest. Several sources on the internet say this is a reason some brokers have little price improvement. Not all brokers get paid to make referrals.

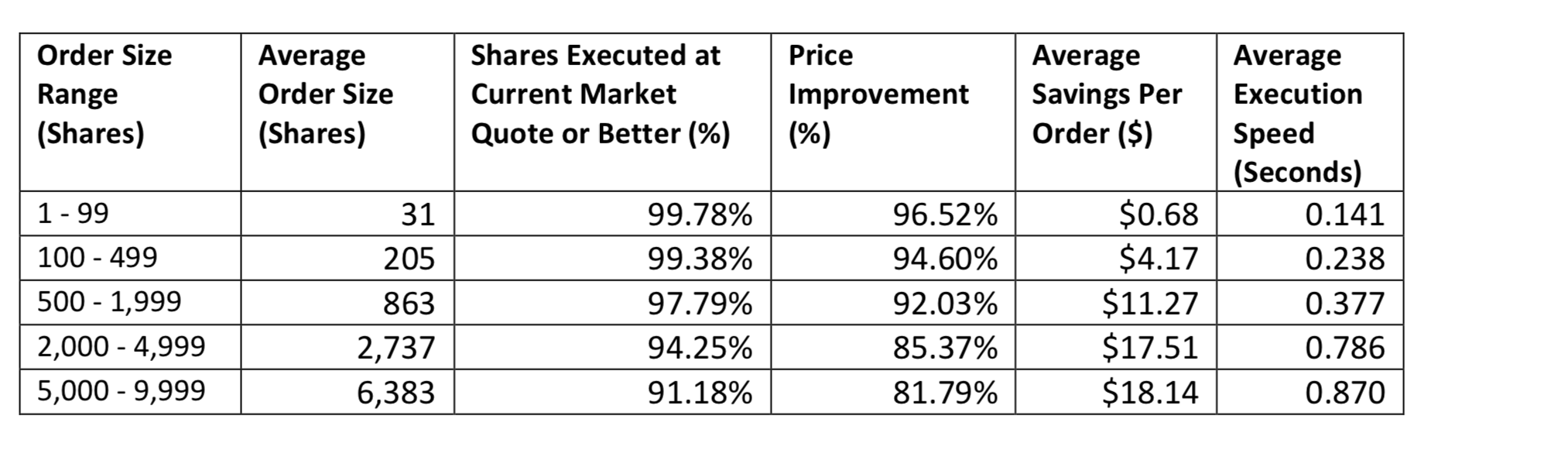

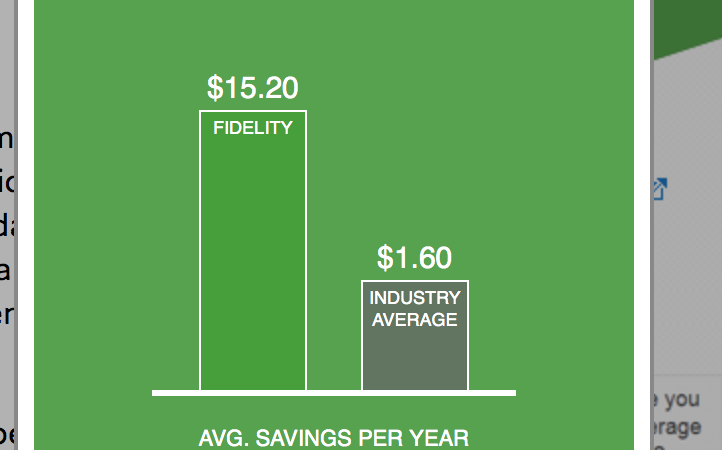

Fidelity has been rated as having the best price improvement by many sources. I am told that they actually tell you how much price improvement there is for your trades and keep a running total of your savings during the year. The next 2 images are from Fidelity about their price improvement. The green image is for 1000 shares compared to the “Industry Average.”.

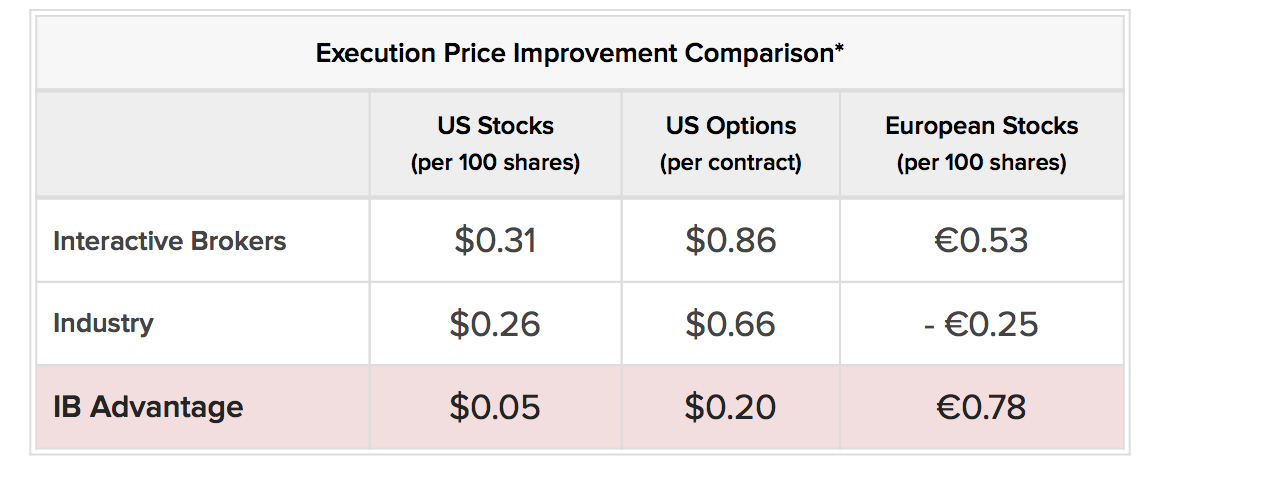

The last image is what Interactive Brokers has to say about its price improvement. This is largely to show that maybe there is an “Industry Average.” For some time periods IB and Fidelity post similar “Industry Averages.”

BTW, Folio Investing has little to say about price improvement. They just say: “….all orders are executed at prices equal to or better than the displayed applicable national best bid/offer price.” Which actually says nothing about whether there is ever any price improvement or how much price improvement there may be (if any). I wonder how they get rewarded for making my trades: if it is not in commissions is it for the referral of my trades? Why is there money left over for a “Rebate?” If a “Rebate” made no commissions possible then I will not complain. But in medicine a similar deal would fall under the Federal Anti-Kickback Statutes.

Time to move to Fidelity or Interactive Brokers? “Price Improvement” has the potential for being a greater factor than the commissions depending on how much difference there is in Fidelity vs Folio Investing for price improvement.

I like IB and I think I will ultimately take SUpirate1081’s advice. Which, I think, is use VWAP “Best Effort” avoid taking liquidity. I probably will not do this right away as I do not want to keep much cash in my SEP-IRA account and I don’t want to see if orders get filled re-submit orders etc. Also the commission on lower priced stocks is not low. But I very my appreciate SUpirate1081’s input and recognize the wisdom. I will try this when I have a margin account, more cash or more time.

Any ideas welcome.

Thanks.

-Jim